A private sector improvement to support growth

Insight

Friday’s main economic events, namely the ‘flash’ PMIs, tell us that there is little reason to fear stagnation, for the time being at least, given still elevated levels for all readings across Europe and the US.

https://soundcloud.com/user-291029717/powell-wants-time-to-heal?in=user-291029717/sets/the-morning-call

There was no singularly consistent theme running through global markets on Friday, though comments from Fed chair Powell engendered a fair amount of intra-day volatility, including a renewed (bull) flattening in the US yield curve. Friday’s main economic events, namely the ‘flash’ PMIs, tell us that while the inflation half of the ‘stagnation’ debate is a real and present danger, there is little reason to fear stagnation, for the time being at least, given still elevated levels for all readings across Europe and the US. That said, the energy crunch is clearly taking a toll on Eurozone services activity – less money to spend on them presumably as energy prices soar – but, surprisingly, not in the UK, and definitely not in the US notwithstanding recent sharp fall-backs in consumer confidence; where the message seems to be ‘watch what they (US consumers) do, not what the say’. See below for a full listing of Friday’s PMI and other releases.

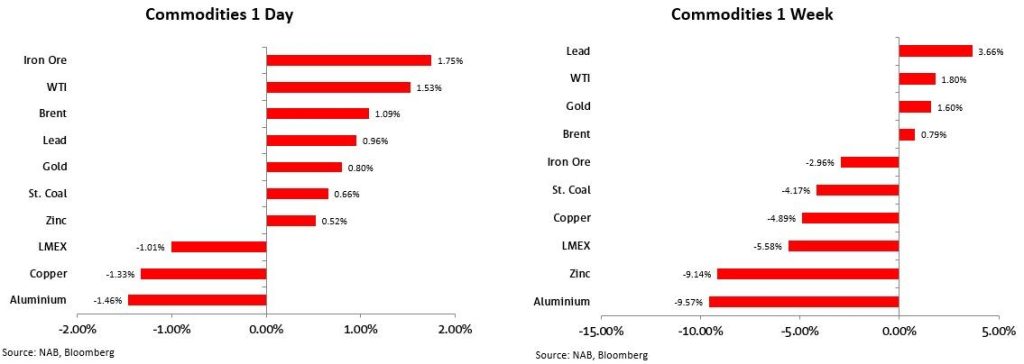

Australia Q3 CPI and ECB and Bank of Canada meetings are among the coming week’s significant known unknowns, in a week that, contrary to widespread expectations last week, isn’t stating off with news of an Evergrande default, after it reportedly made the overdue coupon payments on dollar bonds on Friday just ahead of the expiration of the 30-day grace period that commenced Sep 23. The latter didn’t arrest the weakness in base metals prices on Friday though and which will surely be a victim of sharply reduced housing construction in the months ahead, the LMEX index losing another 1% to be 6% down on the week, led by a 10% drop in aluminium.

“I do think it is time to taper,” Fed chair Jay Powell said Friday, adding “I don’t think it is time to raise rates,” stressing that the labour market needs time to heal with more than 5 million fewer people employed than before the pandemic. Powell nevertheless failed to offer any explicit protest at market pricing which currently has rates lift off fully priced for Q3 2022. Indeed, on inflation Powell said that “Supply-side constraints have gotten worse,” and that “The risks are clearly now to longer and more-persistent bottlenecks, and thus to higher inflation.” “We think we can be patient and allow the labor market to heal,” he said, before adding that, “no one should doubt that we will use our tools to guide inflation back down to 2%” if it looked like more persistent inflationary pressures were taking root.

Powell rightly says that Fed tools don’t do much for supply constraints, echoing recent comments from Bank of England Governor Andrew Bailey, that monetary policy can’t put more truck drivers on the UK’s roads. What central bank policy can, or might, succeed in doing though is reducing risk of second round effects (inflation expectations that then feed ongoing higher wage demands).The latter, though, are of course already very evident in the US and UK.

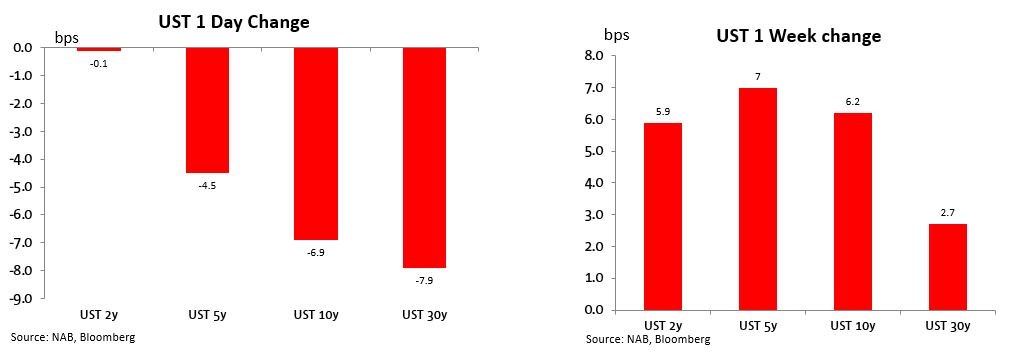

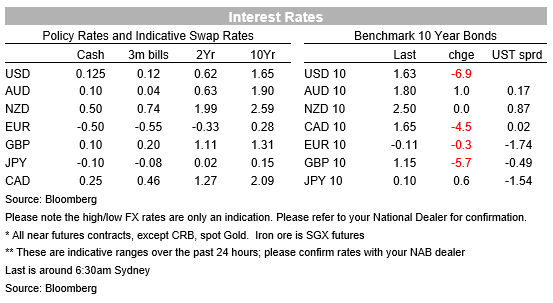

Powell’s comments lead us, and the market, to believe that tapering will not only be announced out of next week’s FOMC meeting but more likely than not will commence almost straight away, rather than wait until December. On a $15bn per month tapering each month, already indicated by the Fed as the most likely magnitude, the Fed would be done by June. The effect of Powell’s comments on bond market was to see little change in front end rates (and hence an expectation for Fed rates ‘lift’ off soon after tapering is complete) while 10-year yields fell by 7bps. This can’t mask a fairly uniform upwards shift in the US yield over the week, with 2s, 5s and 10s all up by between 6 and 7bps (albeit the 30 year was up a lesser 3bps).

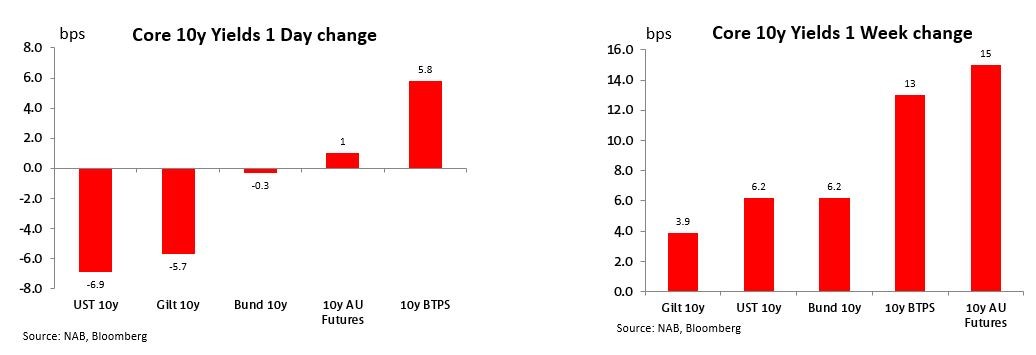

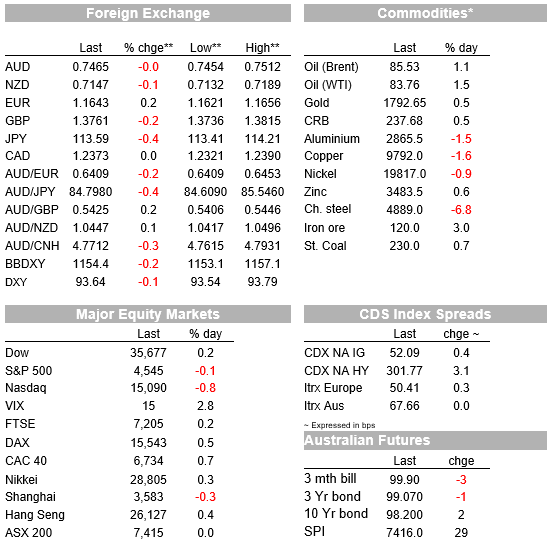

Globally it was a mixed picture Friday, while on the week yields are higher everywhere at 10 years with Australian 10s outpacing the rise in the US and elsewhere, up some 15bps. This is after the RBA came in on Friday to defend its 0.1% YCC target by purchasing the April 2024 bond for the first time since February.

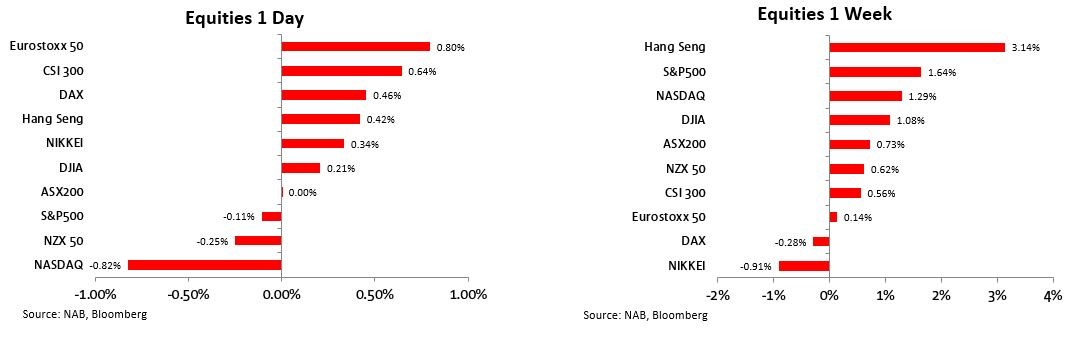

Equities ended Friday with most major indices having an ‘up’ week led by Hong Kong’s Hang Seng (+3.1%) with the Nikkei (-0.9%) and to a lesser extent the German DAX the only two to be down on the week. Incoming Q3 corporate earnings continue to provide support to the S&P500 which ended up over 1.6% albeit own slightly on Friday. The ASX 200 ended the week mid-pack, up 0.7%. More US earnings reports arrive in spades this week (See Coming Up, below).

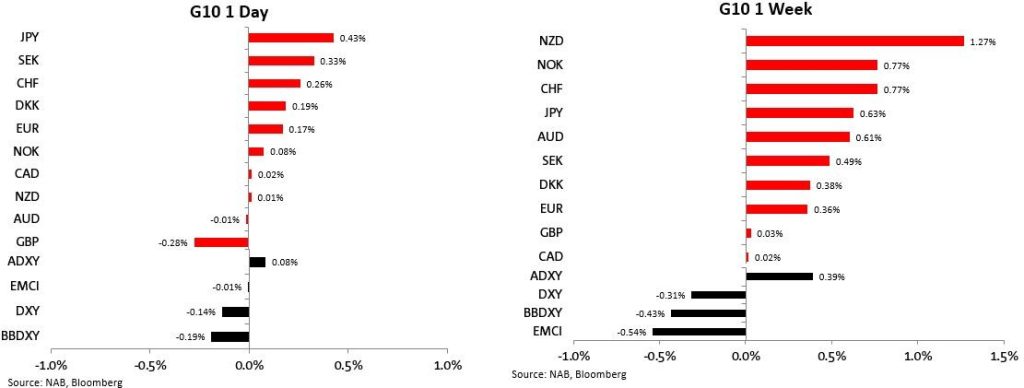

The US dollar was down last Friday and on the week but far from out, the DXY a mere 0.3% lower. At 93.6 (down 1% on its recent highs) the USD is to our mind still traveling essentially sideways inside a broader 93-95 range and, on NAB’s latest forecast, is expected to continue doing so for a while yet. AUD/USD was flat on Friday and 0.6% up in the week, still more than 1% back from its intra-week highs of 0.7459, at 0.7465. the week’s standout performer was NZD, up 1.3% and where after last week’s stonker of a Q3 CPI report, opinions are divided on whether the RBNZ’s next move (Nov 24) will be to lift rates by 25bps or 50bps.

Commodities put in a mixed performance on Friday , with energy-related prices – and too iron ore futures – posting gains but base metals continuing their fall with copper and aluminium both off more than 1%. This brings the fall in aluminium to 9.6% on the week closely followed by nickel (-9.1%) with the LMEX index of base metals off more than 5%. It does make you think that commodity markets, outside energy at least, have started to wake up to the what reduced China property construction in coming quarters (and years?) means for commodity demand. Everglade’s surprise completion of an overdue dollar bond market on Friday, so staving off for now a formal default, doesn’t really change this picture. Incidentally in this respect, Australia’s real time terms of trade index a strickled by Citi on Bloomberg, has now given back more than half of its exceptional mid-September to early October gains.

UK Sep Retail Sales -0.2% vs 0.6% expected

UK Oct Manufacturing PMI 57.7 from 57.1 an 56.0 expected

UK Oct Services PMI 58.0 from 55.4 and 54.5 expected

UK Oct Composite PMI 56.8 from 54.9 and 54.0 expected

France Oct Manufacturing 53.5 from 55.0 and 54.0 expected

France Oct Services PMI 56.6 from 56.2 and 55.5 expected

Germany Oct Manufacturing PMI 58.2 from 58.4 an 56.5 expected

Germany Oct Services PMI 52.4 from 56.2 and 55.2 expected

Eurozone Oct Manufacturing PMI 58.5 from 58.6 and 57.1 expected

Eurozone Oct Services PMI 54.7 from 56.4 and 55.4 expected

Eurozone Oct Composite PMI 54.3 from 56.2 and 55.2 expected

US Oct Manufacturing PMI 59.2 from 60.7 an 60.5 expected

US Oct Services PMI 58.2 from 54.9 and 55.2 expected

US Oct Composite PMI 57.3 from 55.0

Canada August Retail Sales 2.1% vs 2.0% expected, ex-autos 2.8% vs 2.6% expected

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.