Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

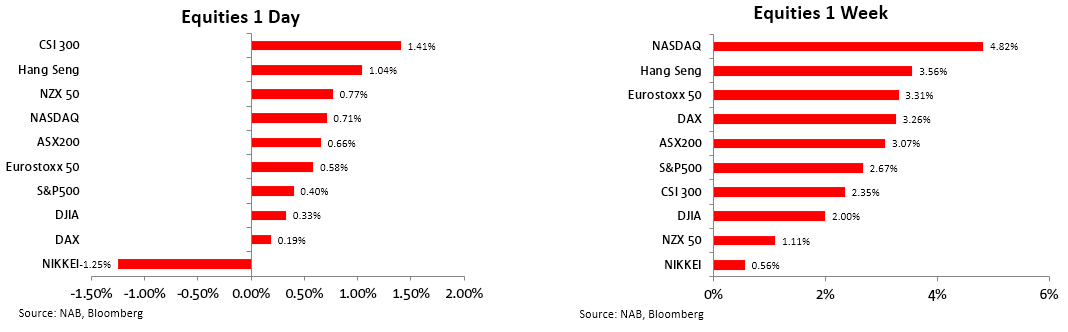

US equities managed to claw back into the green on Friday to extend the strong start to the year.

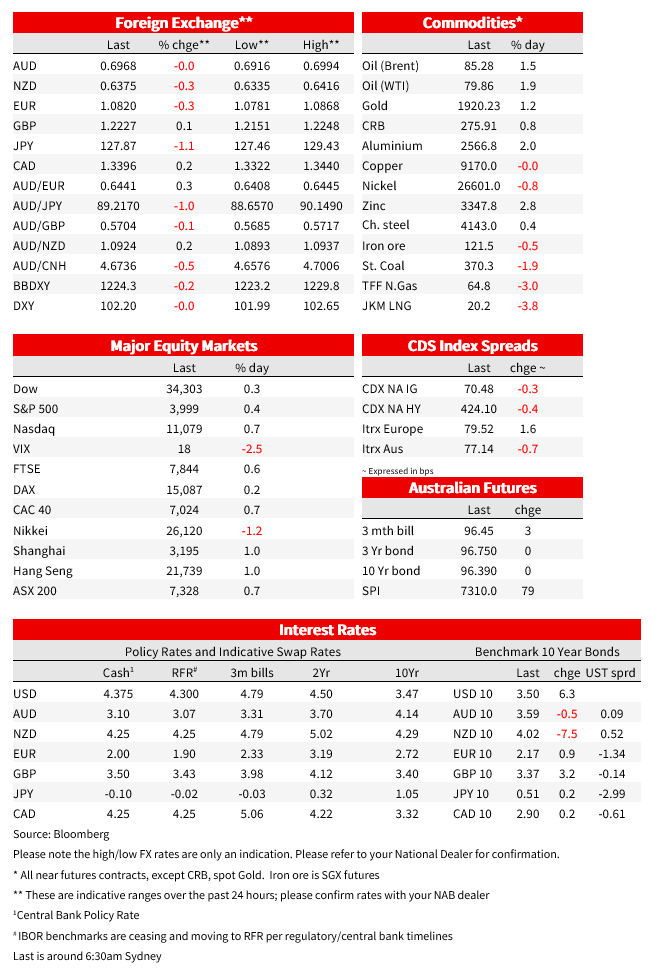

US equities managed to claw back into the green on Friday to extend the strong start to the year. The S&P 500 was 0.4% higher to be 2.7% higher over the week and +4.2% year to date. Bank earnings on Friday were mixed with earnings boosted by rising rates even as concerns mounted about the outlook. US earnings will be a key focus over the next couple of weeks as investors size up the earnings outlook. It’s a slower start to the week with US markets closed today for Martin Luther King Jr Day.

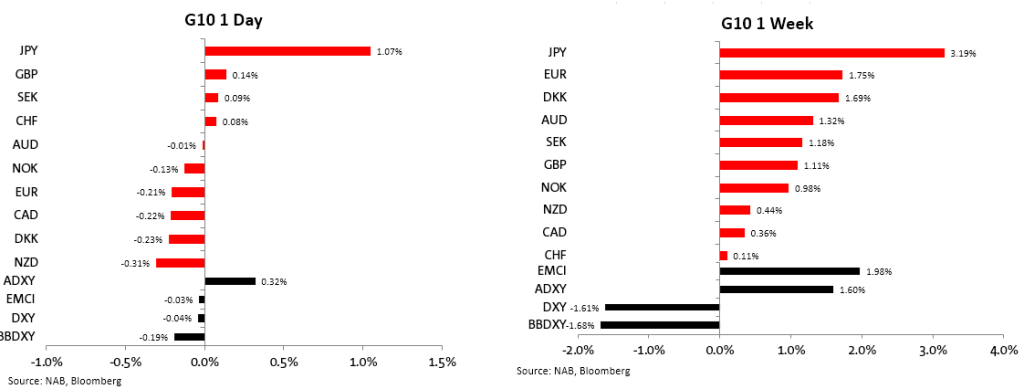

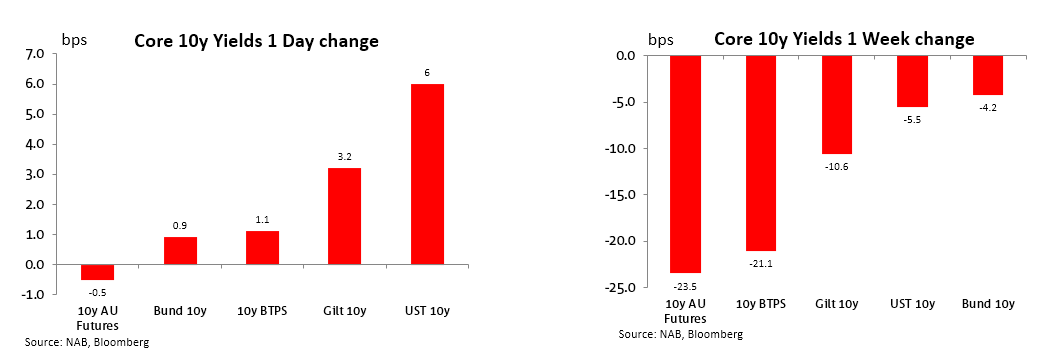

In rates, the bond rally took a breather on Friday, the US 10yr yield up 6bp to 3.50%, still down 6bp on the week and sharply lower than the 3.87% at the end of last year. The US dollar was little changed on Friday on the DXY, but the yen extended gains, up another 1.1% to a 7-month high against the USD. USD/JPY was 3.2% lower over the week to 127.76.

The top of the BoJ’s YCC tolerance band was tested on Friday with the 10yr yield rising as high as 0.54% before falling back to 0.505%. The BoJ bought ¥5 trillion of JGBs to defend the target on Friday, its largest ever daily amount of bond buying and following ¥4.6 trillion of purchases on Thursday. Pressure on the BoJ’s YCC framework has increased since the surprise 20 December decision to widen the allowable band for bond movements. A local media report on Thursday saying the central bank will assess the side effects of the policy has fuelled speculation around a change.

As for data flow, US Consumer Sentiment beat expectations, jumping to a 12-month higher of 64.6 from 59.7 in December (Consensus 60.7). Plunging gasoline prices are a likely driver, with the improvement led by a 9.2pt increase in current conditions. The share of people citing price rises as a drag on finances dropped 8pts. Short term inflation expectation fell to 4.0% from 4.4%, while the 5-10yr number ticked up a tenth to 3.0%. It has been around 3% since mid 2021. A majority of respondents said they anticipate their incomes to rise at least as fast as prices in the year ahead, the most since October 2021.

The tone of the other data flow on offer was decidedly less bad than feared. November Eurozone industrial production was +1.0%m/m against expectations for 0.5% and after last month’s -1.9%. German flash Q4 GDP was 1.9%y/y, implying quarterly growth about flat. UK Monthly GDP grew 0.1% m/m, outpacing expectations for a -0.2% fall on robust service sector activity and defying fears of a recession for now. Chinese trade data saw exports -9.9% y/y (consensus -11.1%) and imports down 7.5% y/y (consensus -10.0%) though the impact of Covid in the December clouds the numbers.

In FX, the yen was the big mover over the week. The yen was 3.2% higher against a broadly weaker US dollar. The move came on Thursday and Friday as speculation ramped around another hawkish tweak from the BoJ this week. The USD/JPY was 1.1% lower on Friday at 127.87, not far off its intraday low of 127.46. That followed Thursday’s 2.4% fall. A combination of upward pressure on Japanese yields and a paring of US rate hike expectations has seen some reversal of earlier depreciation pressure for the yen as rate differentials with the US widened. USD/JPY is at its lowest since May 2022.

The USD was little changed on Friday on the DXY but is 1.6% lower over the week, losing ground against all G10 currencies. The AUD ended Friday little changed at 0.6977 and middle of the G10 pack against the US dollar on the day. The aussie touched an intraday high of 0.6994, just shy of 70c. The last time the AUD was above 70 was August 2022.

Equity markets rose on Friday, grinding back into the green over the session after being down as 0.9% shortly after the open. The S&P500 was 0.4% higher, to be 2.7% higher over the week. The Nasdaq was 0.7% higher to be 4.8% higher over the week, buoyed by pared expectations for fed tightening. In Europe, the Euro Stoxx 50 and FTSE 100 were each up 0.6%.

JP Morgan, Bank of America, Citigroup, and Wells Fargo reported on Friday. Mixed results and some evident concerns about the outlook saw stocks initially open lower before reversing. Consumer discretionary and financials led gains on the day Earnings season will be a key focus in the next couple of weeks with question marks over whether the earnings outlook has been revised sufficiently lower.

US yields were lower across the curve over the week, although the bond rally took a reprieve on Friday with post CPI falls in yields pared back. The 10yr was 6bp lower over the week to 3.50% after rising 6bp on Friday. The 2yr ended the week down just 2bp at 4.23% after gaining 9bp on Friday to be around its pre-CPI level. Expectations the Fed will eventually have to pull rates back more materially from restrictive settings have seen the belly lead moves with the 5yr down 9bp over the week after an 8bp rise on Friday. Testing of the BoJ’s 0.50% upper limit for the 10Y JGB was a support for higher yields, while some post CPI profit taking ahead of an expected $35bn in US investment grade corporate supply in the week ahead may also have contributed. Yield moves in Europe were smaller on Friday, with 10yr Bunds 1bp higher and Gilts up 3 bp.

Near-term market pricing for the Fed was little changed on Friday despite the moves in yields, with a peak fed funds rate of 4.92 and 47bp priced over the next two meetings. Atlanta Fed’s Bostic speaking in a CBS interview on Thursday evening in the US welcomed the December CPI result. “This report was really welcome news.” “It really suggests that inflation is moderating, and it gives me some comfort that we might be able to move more slowly now that we are in restrictive territory.”

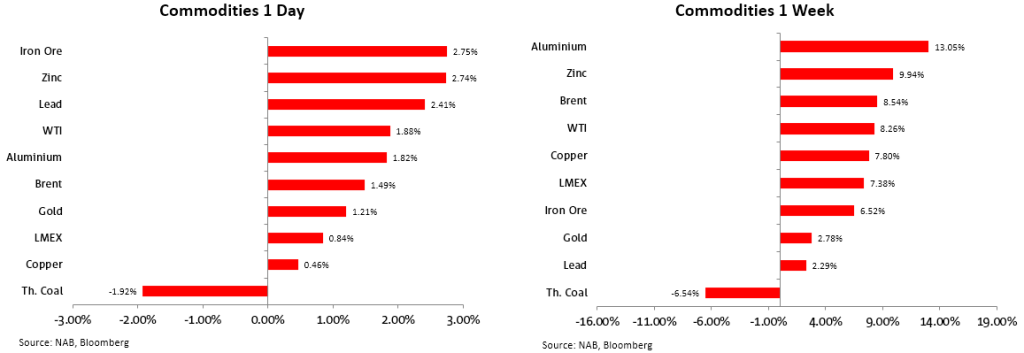

Commodities were generally higher over the week, boosted by optimism over China reopening. China said almost 60,000 people have died from Covid-related causes since early December, a glimpse at the extent of the reopening wave gripping the country as the WHO urged more data sharing. The Chinese CDC said it hasn’t detected any dangerous new mutations. Despite the near term hit, the prospect of a recovery through 2023 has buoyed commodity demand. Brent Oil was up 1.5% on Friday and 8.5% over the week to retrace most of last week’s decline.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.