Online retail sales growth slowed in March

Insight

The market was not prepared for Powell’s hawkish remarks, sending short rates and the USD higher and equities lower.

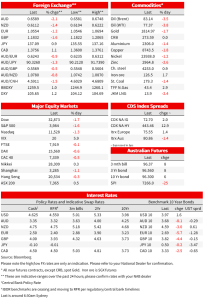

AU: Trade balance ($b), Jan: 11.7 vs. 12.2 exp.

AU: RBA cash rate target (%), Mar: 3.6 vs. 3.6 exp.

CH: Exports (USD YTD y/y%), Feb: -6.8 vs. -9.0 exp.

CH: Imports (USD YTD y/y%), Feb: -10.2 vs. -5.5 exp.

GE: Factory orders (m/m%), Jan: 1.0 vs. -0.7 exp.

Following a series of stronger than expected US data releases in recent weeks as well as comments from Fed speakers noting the increasing risk of further policy tightening ahead, speaking overnight Fed Chair Powell delivered a hawkish warning. Given what we already knew, his hawkish remarks shouldn’t have been a surprise, but evidently the market was not prepared. UST front end yields jumped, the USD more than reversed recent losses and equities fell across the board. The AUD and GBP are the notable underperformers, AUD not helped by the RBA’s softer tightening bias. GBP weighed down by BoE Mann’s concern on sterling.

Ahead of Fed Chair Powell’s semi-annual monetary policy testimony before the Senate Banking Committee, recent US data releases were already telling us that the US economy started 2023 on a much stronger footing than most had anticipated with inflationary pressures also proving more persistence.

This economic backdrop had already triggered a repricing in Fed rate hike expectations, but Fed Chair Powell’s acknowledgment of the current economic backdrop as well as warning that the Fed is prepared to do more still triggered a significant market reaction. This of course needs to be seen in the context that early February the Fed had step down the pace of hikes by lifting the Funds rate by “only” 25bps to 4.75%.

Powell said that “The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated,” and then he added that “If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

On the data, the Chair noted the moderation in inflation since the middle of last year. The 12 month change in total PCE prices has slowed from a 7% peak to 5.4% as energy prices and supply chain bottlenecks have eased. Core PCE is down to 4.7% and inflation in the core goods sector has fallen. Powell also noted that while housing services inflation remains too high, the flattening out in rents in recently signed leases points to a deceleration in this inflation component. But he warned there is little sign of disinflation in core services excluding housing, which accounts for more than half of core consumer expenditures.

The Fed is clearly data dependent and Powell’s’ remarks about the “totality of the data” means that upcoming data releases are going to be important, they will either vindicate the price action seen overnight and seal the deal for a 50bps hike on March 22 or they will likely trigger a reversal. On Friday we get non-farm payrolls and then next week we get the February CPI report

The Fed Funds futures market now sees an 80% chance of a 50bps hike in March, up from around 20% prior to Powell’s remarks. The front end of the UST curve has a led sharp flattening of the curve with the 2y rate up 13bps to 5.018%, a fresh high at a level not seen since 2007. 10y UST met some resistance (again) at 4% and is currently up 1bps relative to yesterday’s level 3.94%, the flattening of the curve sees the 2s10s scale of inversion breaking minus 100bps (now at 103 bps), a level not seen since the early 1980s .

The USD also enjoyed a decent jump, more than reversing recent losses. The DXY index is up 1.25% and currently trades at 105.624, after trading lower in the previous two days . Looking at G10, the big dollar is stronger across the board with JPY at the top of the leader board, down “just “0.85%”. USD/JPY is back above ¥137, threating the break above recent highs. The euro is down 1.2% and now trades at 1.0554, NOK and SEK are the big underperformers, both down close to 2.6% with the former not helped by a 3.53% drop in Brent oil.

The other two notable underperformers are the AUD and GBP. The AUD now trades at 0.6591, down 2.09% and extending its decline post yesterday’s RBA policy meeting . The RBA lifted the cash rate by 25bps to 3.60%, as widely expected but the Statement was less hawkish with the RBA removing February’s pre-commitment to more hikes over coming months. There was a hint of data dependency with reference to “when and how much further” tightening of monetary policy will be needed. The market saw this as a possible pause in April after the RBA’s ten consecutive rate hikes. Governor Lowe speaks this morning (see more below), so the market will be looking for a little bit more guidance from the chief.

GBP now trades at 1.1834, down 1.6% over the past 24 hours. The pound was not helped by BoE Mann’s remarks overnight, she sits at the hawkish end of the spectrum and while her views on the need for more aggressive BoE rate hikes are well known, overnight she strayed into currency markets, suggesting that the pound could fall further as the Fed and ECB hike rates further – she clearly would prefer the BoE to follow that trend but has been out-voted.

NZD sits somewhere in the middle of the G10 pack down by only 1.37% to 0.6116, the kiwi traded down to a fresh year to date low of 0.6104, but has recovered a little in the past hour.

As noted at the start, US equities were spooked by Powell’s remarks with the S&P 500 down 1.55% as I type and down below the 4000 mark (@3998 ) while the NASDAQ is -1.25%. Earlier in night the Eurostoxx 600 ended the day down by 0.77% while the UK FTSE 100 closed 0.13% lower.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in March

Insight

Rising artificial intelligence could see as much as half the work being done today automated within 20 years and organisations need to know how to get ready, an AI expert tells NAB’s Transaction Banking customer event series.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.