Stock mostly firmer at start of new month, Europe faring better than US where S&P 500 ends +0.2%

New Orders the devil in the detail of a slightly higher than expected US manufacturing ISM…

…China slowdown starting to make its mark?

India surprises at COP26 with 2070 net-zero pledge

SNB joining the monetary policy party via the exchange rate?

RBA expected to acknowledge today the yield curve is henceforth out of its control

I was of a feeling it was out of control, I had the opinion it was out of control – U2

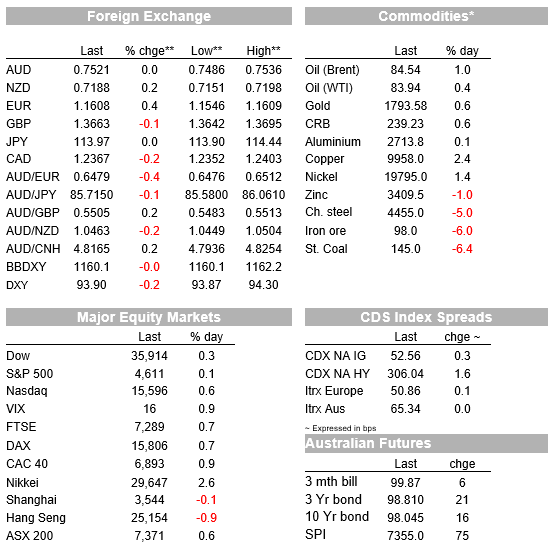

The new month has begun relatively quietly, unsurprisingly given the plethora of key central bank set pieces due this week, commencing at 14:30 AEDT this afternoon. Across the board gains in European stocks (led by Spain and Italy) have given way to a more nuanced US session with the S&P 500 ending up just 0.2% while other mainboard indices are closing with somewhat bigger gains. In FX modest – JPY led – USD gains in Asia Monday have turned to losses offshore, with weakness dated to the release of the US Manufacturing ISM report. 10-year bond yield are slightly higher almost everywhere in the world, including a 2.5bps rise in the implied yield on 10-year AU futures since yesterday’s local close.

The night’s main economic event, namely the US Manufacturing ISM, came in down 0.3 on September at 60.8 but which was 0.3 better than expected. Nothing much to see there, though the details reveal a sharp drop in theNew Orders component, to 59.8 from 66.7 (its lowest since June 2020). So still in expansionary territory, but suggesting that ongoing of supply chain issues and now the lagged impact of the recent fall-back in China PMIs – where the average of the NBS and Caixin manufacturing PMIs released Sunday/Monday is 49.9 – are both taking a toll. In the case of the former and as one commentator dryly suggests, why bother ordering something that isn’t going to arrive for months? (if you’re lucky). Elsewhere in the report, Prices Paid rose back to 85.7 from 81.2 and 79.4 prior – this after seemingly ‘peaking’ at 92.1 in June. Supplier deliveries also extended to 75.6 from 73.4. Order backlogs though easing a bit (63.6 from 64.8). Elsewhere employment to 52 from 50.2 – back to July levels.

In other economic news the final Markit US manufacturing PMI slipped to 58.4 from the preliminary 59.2 while in the UK the 57.7 preliminary read became 57.8. Canada’s (one and only) manufacturing PMI was 57.7 up from 57.0 in September.

In FX, the mild USD gains we witnessed during the APAC time zone yesterday have given way to modest US weakness overnight , losses we can date squarely to the timing of the US ISM release and evident disappointment at the fall-back in the New Orders sub-reading. At 93.9 though (-0.2%) DXY index remains in the middle of what we identify as a 93-95 broad range – tramlines we suspect it can remain comfortably inside for some time yet, barring a major surprise one way or the other out of Wednesday night/Thursday morning’s FOMC announcement and/or a big correction in risk sentiment for whatever reason.

USD slippage has been led by SEK (+0.7%) and CHF (0.6%) where in the case of the latter the SNB now looks to be tolerant of a weaker EUR/CHF exchange rate , now trading below 1.06 for the first time since May 2020 in what look like it could be the SNB’s contribution to the global trend toward less-easy monetary policy settings. In the SNB’s case, this is through tighter monetary conditions via the exchange rate rather than overtures toward lifting its -0.75% policy rate and where a higher ECB policy rate is likely to remain a prerequisite.

In our time zone yesterday, it was JPY slippage driving a slightly firmer USD, following results of the weekend Japanese elections showing PM Kishida’s LDP winning a comfortable outright majority and which propelled the Nikkei to a 2.6% gain (stock market strength and currency weakness typically going hand-in-hand). Following his victory, Kishida told reporters a concrete action plan was needed for raising wages and he would work on passing an extra budget as soon as possible to help the Covid-battered economy. He also said his government would unveil its coronavirus plan by the middle of this month.

AUD/USDisflat to Friday’s New York close at 0.7520 and hard to envisage it doing too much in front of the 2:30pm RBA, but where we continue to note that volatility in the term structure of Australian interest rates, in absolute terms or relative to other countries, remains a very minor influence on the currency relative to other factors.

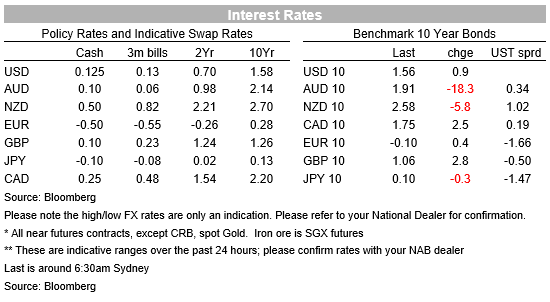

In bond markets , the 3-year AU futures, after adding some 10 ticks so falling by 0.1% in yield terms during Monday’s day session, have largely flat-lined overnight and in front to the RBA announcement, while 10s are also not much changed. 10-year Treasuries briefly revisited 1.60% overnight but since the aforementioned ISM report have fallen back, currently 1.58%, up 2.5bps on Friday’s NY close. 2-year yields are 1bp higher at 0.51% as the clock ticks down to Wednesday afternoon’s FOMC announcement, expected to fire the gun on tapering of its QE bond buying programme.

In commodities, the biggest moves are currently being seen in coal, where sharp falls in recent days are being attributed to evidence China is ramping up domestic production, an extension of the mantra earlier in October to ‘secure supplies at all costs’. Related or not, overnight, Indian Prime Minister Narendra Modi surprised delegates at the COP26 climate summit with a pledge: the world’s third-biggest emitter (and second largest conumers of coal) will reach net-zero by 2070.

Coming Up

RBA the main draw today and where last week’s de facto abandonment of the 0.1% April 2024 Yield Curve Control target is expected to be formalised. In doing so, presumably the broad contours of the RBA’s forecast revisions, to be revealed in the Statement today prior to publication in Friday’s SoMP would, if realised, allow for rates ‘lift-off’ potentially occurring somewhat earlier than April 2014. A point of market interest here is whether or not the RBA maintains some form of date-based guidance alongside a repetition of the state-based guidance for lift-off that already exists (i.e. that inflation must be deemed to be sustainably inside the 2-3% target, and with wages growth materially higher than currently). Another point of focus is on whether the QE policy ($4bn of purchases per week) will continue through at least February next year as currently articulated.

This morning (7:30 AEDT) RBNZ Governor Orr speaks on “Housing Matters, which will doubtless focus on the unsustainable level of house prices, a day ahead of the Financial Stability Report

Outside of the RBA there isn’t much else of market interest on today’s calendar. RBA Governor Guy Debelle is due to participate in an on line panel at 16:50 at the Impact X Sydney Summit, which is all about ‘designing actionable pathways to zero emissions’.

Offshore we only have final Eurozone manufacturing PMIs, where the pan-Eurozone version is seen unchanged on the 58.5 preliminary read.

Finally, the 2.30 announcement that will stop the nation will be interrupted again at 3,00p for the race that stops the nation, your scribe predicts – with zero confidence – to be won by the Johnny-come-lately last entrant into the field, Floating Artist.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.