Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

After an initial hint of contagion, European and US equities looked past Asian concerns over China’s regulatory crackdown, closing the day with modest gains at or near record highs. Meanwhile the real story in the rates markets has been the record move decline in the 10y US real rate.

https://soundcloud.com/user-291029717/real-yields-reach-lows-vaccine-reach-slows?in=user-291029717/sets/the-morning-call

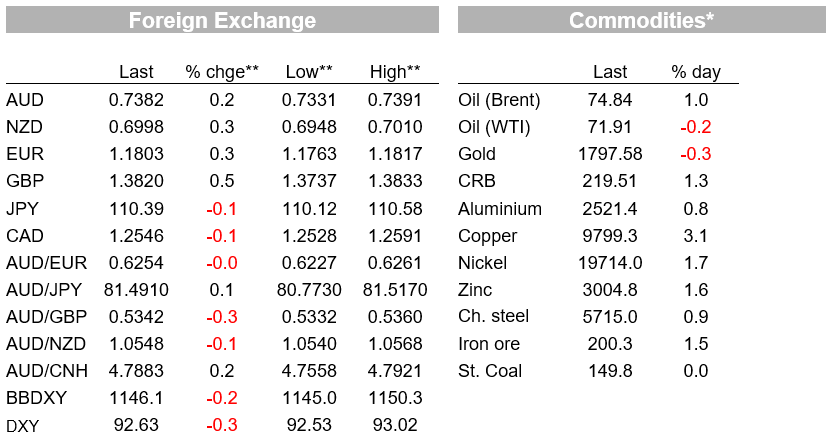

After an initial hint of contagion, European and US equities looked past Asian concerns over China’s regulatory crackdown, closing the day with modest gains at or near record highs. Meanwhile ahead of the FOMC meeting later this week the real story in the rates markets has been the record move decline in the 10y US real rate. The improvement in risk sentiment and decline in real US yields sees the USD weaker across the board, helping antipodean currencies recover. NZD is just above 70c while AUD edges closer to 74c.

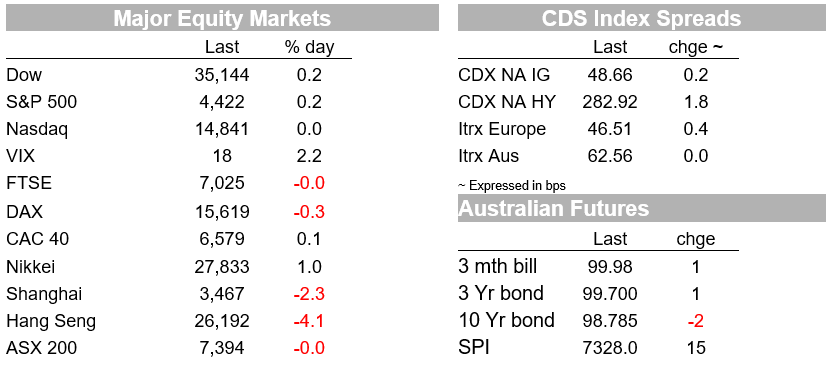

Asian equities ex Japan had a rough start to the new week with sharp declines in Chinese stocks setting the tone. China’s regulatory uncertainty is not going away, indeed it looks to be broadening with no clarity as to when and where it will end. The CSI 300 index fell 3.22%, the Hang Seng fell 4.33% and the Nasdaq Golden Dragon China Index fell 7%.

After the recent clampdown on the tech sector, on Monday Chinese Authorities shifted their attention to the education sector banning companies that teach school subjects from making profits, raising capital or going public . Bloomberg notes that in total $126bn in market capitalization has been erased from Chinese education stocks traded in the US, China and Hong Kong this year. The regulatory uncertainty is keeping investors nervous, property management shares traded in Hong Kong came under pressure after regulators said they were aiming to “notably improve order” in the market. Food delivery companies have also been put on notice, after authorities in Beijing issued a notice that online food platforms must, among other things, respect the rights of delivery staff and ensure workers earn at least the local minimum income.

Sentiment wasn’t helped by further headlines on tense US-China relations. High level US and China talks at a summit in China were contentious, with the result being two lists of grievances supplied by the Chinese side and a spokesman saying that the relationship was “in a stalemate and faces serious difficulties”. So, it seems that nothing has essentially changed since the last fiery meeting held in Alaska in March.

S&P futures were down as much as 0.6% during Asian trading but lifted from the European open and then pushed higher during the US session. Indeed, after an initial wobble, European equities recovered into the close with regional indices ending the day mixed, but close to unchanged . The Stoxx Europe 600 eased 0.08%, trimming losses of as much as 0.6%. Main US equity indices have managed to end the day in positive territory, posting yet another record high. The S&P 500 and Dow closed +0.24%, and the NASDAQ was +0.03%. After the bell, Tesla shares gained over 1.5% following better than expected second-quarter earnings, buoyed by strong demand for its electric vehicles and suggestion deliveries this year may exceed its longer-term projections for 50% growth.

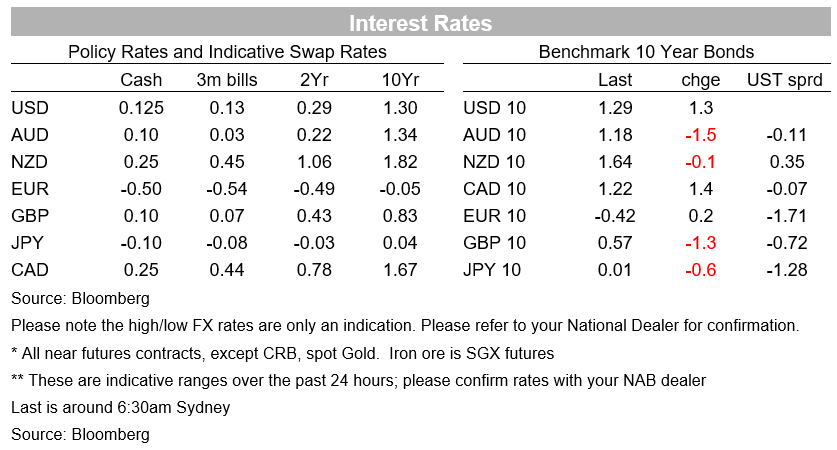

Moving onto the rates market, the UST curve is steeper on the day with the front end of the curve supported by a solid demand in the 2y UST auction while the back end of the curve has edged a little bit higher . 10y and 30y rates up 1.4bps and 2.6bps respectively to 1.2913% and 1.942%. The 10y Note traded to an overnight low of 1.2212% early in session as equities assessed the ramifications from Asia, but then moved up as the equity market recover.

That said, the real story has been the record decline in real yields. Real yield US and European 10-year rates both fell to record lows, with real US Treasuries taking a peek below minus 1.13% and European swaps hitting minus 1.65%. The move is being put down to illiquid summer trading conditions and ongoing concerns about the growth outlook, following signs that US growth has passed its peak and as the spread of the delta variant of COVID19 threatens the global economic recovery. Bond markets might have some macro concerns, but equity markets are hardly trading like there’s a major growth scare, and low yields simply add to the appeal of equities.

The data played into this narrative with new US home sales fell to their lowest level in over a year , indicative of much weaker demand after significant price rises, given that monthly supply is back to pre-pandemic levels (sales up to 6.3 months of supply versus a low of 3.5 months last year). Weakness in the series has been forewarned by much weaker mortgage applications over the past several months but, as noted by Pantheon Macroeconomics, the consensus was inexplicably picking a lift in sales.

Germany’s IFO business climate indicator fell for the first time in six months and off a three-year high, with the “expectations” indicator dropping by more than the lift in “current conditions”. The commentary suggested that supply bottlenecks and concerns over newly rising infection numbers were weighing on the German economy.

A combo of lower real yields and improved risk sentiment weighed on the USD overnight and helped risk sensitive currencies such as the AUD and NZD recover from a soft start during our APAC session yesterday. USD indices have ended the day down between 0.24% (DXY) and 0.34% (BBDXY) with the greenback underperforming all G10 pairs. GBP and SEK are at the top of the leader board, up ~0.55%. Cable now trades with a 1.38 handle (1.3818) and while it is still early days, encouragingly the UK has seen a sharp decline in the 7dma of infection rate to 35.5k, down sharply from 48.1k a week prior.

After we called a day in Sydney yesterday, the AUD traded to an intraday low of 0.7331 and the NZD fell to a low of 0.6948. But as risk sentiment improved during the overnight session, both antipodean pairs benefited from the lift in sentiment. The AUD made a run for 0.74 but just fell short (high of 0.7391) and currently trades at 0.7385, meanwhile the kiwi climbed to a high of 0.7010, and now looks to be consolidating juts above the figure.

Moving onto US politics, the bipartisan infrastructure bill hit another roadblock after Republicans rejected an offer to meet and address all outstanding issues from the White House and Democrats, calling into question the potential for the $579bn Bill to pass before Congress’s August recess. Passing the bill wold be a big boost for president Biden intentions to get his $3.5trn tax and spending package over the line.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.