Markets Today: Resilience and hope drives bond yields higher

The flow of economic data surprises has continued overnight and this time it was a uniformly stronger than expected performance of the services sector across major Developed Market economies.

Strong services PMIs point to DM economic resilience

Services inflation remains elevated, implying Central Banks still have more work to do

Gilts lead global rates move higher, on relatively stronger services PMI

Equity markets spooked by the tighter for longer CB narrative. NASDAQ leads decline

USD stronger across the board with GBP the exception

AUD back below 0.69, NZD softer but key support at 0.62 not breached

Coming Up: RBNZ MPS, AU WPI, German IFO, FOMC minutes early tomorrow

Events Round-Up

NZ: PPI output (q/q%), Q4: 0.9 vs. 1.6 prev. GE: Manufacturing PMI, Feb: 46.5 vs. 48.0 exp. GE: Services PMI, Feb: 51.3 vs. 51.0 exp. EA: Manufacturing PMI, Feb: 48.5 vs. 49.3 exp. EA: Services PMI, Feb: 53.0 vs. 51.0 exp. UK: Manufacturing PMI, Feb: 49.2 vs. 47.5 exp. UK: Services PMI, Feb: 53.3 vs. 49.2 exp. GE: ZEW Survey of expectations, Feb: 28.1 vs. 23.0 exp. CA: CPI (y/y%), Jan: 5.9 vs. 6.1 exp. US: Manufacturing PMI, Feb: 47.8 vs. 47.4 exp. US: Services PMI, Feb: 50.5 vs. 47.3 exp. US: Existing home sales (m/m%), Jan: -0.7 vs. 2.0 exp.

Work it, Make it, Do it, Makes us Harder, Better, Faster, Stronger – Daft Punk

PMI releases over the past 24 hours, from Japan to Germany, the UK and the US, show activity in the services sector surprising to the upside in February. The good economic news is bad news as the

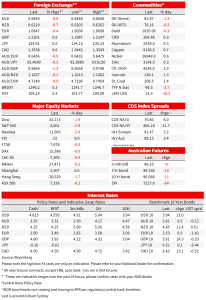

resilience of Developed Market (DM) economies means Central Banks (CB) still have more work to do. UK Gilts have led a rise in core global bond yields with 10y UST yields now at 3.95%. Equity markets are spooked by the tighter for longer CB narrative. NASDAQ leads decline, down over 2% while the USD is stronger across the board with GBP the exception. AUD is now back below 69c and NZD is also softer but with key support at 0.62 not breached.

The flow of economic data surprises has continued overnight and this time it was a uniformly stronger than expected performance of the services sector across major DM economies. Yesterday, during our time zone, Japan’s PMI were mixed with the manufacturing survey falling to 47.4 from 48.9 previously, but the services sector rose to an eight-month-high of 53.6 from the previous month’s 52.3. Of note too, the service firms’ input costs rose at the fastest pace in eight months, while the inflation for prices they charged to customers only advanced to a two-month-high, indicating thinner profits.

PMI releases overnight depicted a similar picture to the one seen in Japan, PMI services readings were notably stronger than expected across the Euro Area, UK and the US, rebounding further into expansionary . Manufacturing gauges were weaker across Europe and slightly stronger in the US, but still all in contractionary territory. With the services sector being a much larger and important part of the economy, composite gauges expanded. And like Japan’s details, services inflation remains sticky with the Euro area release suggesting “hints at persistent elevated price trends in the service sector, linked in part to higher wage growth” and the US release noting that the improved supply situation had taken price pressures out of manufacturing supply chains but “the upward driving force on inflation has now shifted to wages amid the tight labour market”.

The PMI releases are not only painting a picture of economic resilience across DM economies, but the with inflationary pressures still elevated, the data also suggest that DM central banks still have work to do in order to bring inflation to heel.

The move up in global rates was led by UK Gilts, given the relatively bigger upward surprise from the PMIs. UK flash composite PMI rose to 53 in February, from 48.5 in January – well above consensus expectations for a marginal increase to 49. Gains mostly reflected a sharp increase in the services PMI to 53.3, from 48.7 (49.2exp.). The two-year gilt yield gained 17bps basis points to 3.86%, flattening the curve with the 10y rate climbing 14bps to 3.60%. Talk of the BoE pausing its hiking cycle in March now look premature with the OIS market now pricing a 78% chance of a 25bps hike in May (after a 25bps hike in March).

The rise in German Bund yields was led by the back end of the curve with the 10y tenor up 7bps to 2.525% while the 2y yield rose by 5 to 2.932%. Meanwhile in the US, the move higher in yield has been led by the belly of the curve , the 5y Note is up 14bps to 4.167% while the 2y rate gained 10bps to 4.727%. As I type the 10y UST yield trades at 3.95%, close to its overnight high of 3.9584% and up 12bps relative to levels 24 hours ago. Of note too, For the first time, the market fully prices in three full 25bps hikes from the Fed over coming meetings with a peak in the terminal rate now seen at 5.36% by the July 26Th meeting.

The equity market has been spooked by the repricing of Central Bank rate hike expectations (more hikes) following the PMI data releases. The tech heavy NASDAQ is leading the declines, currently down 2.15% while the S&P 500 is -1.84%. In Europe the STX Europ 600 ended the day down by a modest 0.19% while main regional indices recorded declines closer to 0.5%. The UK FTSE 100 fell by 0.46%.

Moving onto to currencies, the USD is stronger across the board not only benefiting from the move higher in UST yields but also by the increase in risk aversion with the VIX index climbing ~2point to 22.8. The BBDXY and DXY index are up around 0.35% and within G10, sterling is the outlier as the only G10 pair outperforming the greenback. The much stronger than expected UK Services PMI not only is suggesting an improved chance the UK may avoid a recession this year, but also doesn’t help the BoE’s task to cool a tight labour market and bring inflation back to target.

The AUD now trades at 0.6854, after climbing to an intraday high of 0.6921 yesterday during our trading hours.Yesterday the RBA minutes sounded hawkish revealing a50bps hike was discussed at the Bank’s meeting early in February. My colleague Tapas Strickland also noted that Minutes revealed “Members also noted that the cash rate was lower than policy rates in many other comparable economies. While wages growth remained lower here than elsewhere, Australia’s positive exposure to higher commodity prices and the extra savings buffers accumulated by households were estimated to be larger than in other countries.” A high WPI could change the view on wages being different to the rest of the world. WPI is out today at 11:30 am Sydney time (see more below).

Ahead of the RBNZ meeting today (more below), the kiwi is one of the weakest performers, down about 0.4% overnight to 0.6211, with key support at 0.62 holding.

In other economic news, US existing home sales were weaker than expected, falling for a twelfth consecutive month, taking the peak to trough slump to 37%. Canadian CPI inflation data showed inflation easing to 5.9% y/y, 0.2pps weaker than expected. The average of the three core measures nudged down by 0.1% to 5.6% y/y. The data supported the Bank of Canada’s “pause” guidance on rate hikes at its last meeting.

Meanwhile in Geopolitics, Russian President Vladimir Putin said Moscow would suspend its participation in the last remaining major nuclear-arms-control treatybetween the US and Russia, and said he would continue Russia’s military campaign in Ukraine.

Bloomberg also reports China’s president Xi Jinping is preparing to visit Moscow for a summit with Russia’s president in the coming months. Amid scepticism from western leaders, Beijing says it wants to play a more active role aimed at ending the Russia-Ukraine conflict. President Xi could visit Russia in April or in early May.

Coming Up

New Zealand gets trade data ahead of the RBNZ meeting outcome at midday Sydney time. For Australia the Wage Price index (WPI) is the data release to watch (11:30 am Sydney time) with Construction work done for Q4-22 are released this morning.

Later in the day, Germany gets it final CPI reading for January along with the IFO survey for February (business Climate at 90.7 exp vs 90 prev.). Tonight, the US gets mortgage applications followed by the FOMC minutes early tomorrow morning.

Our economists expect WPI to print at 1.0% q/q and 3.5% y/y (the RBA SoMP has a forecast of 3.5% y/y). The RBA has already noted that price-wage persistence and the risks of a shift in wage and price setting behaviour could see the economy “knocked off that narrow path” to a soft landing. An upward surprise to today’s WPI could push the RBA to move deeper into restrictive territory to be able to forecast a more material softening in the labour market.

Our BNZ colleagues note the recent vicious weather has thrown awful curve-balls for today’s RBNZ MPS. However, we think inflationary messages will keep the RBNZ/MPC hiking its OCR, to 4.75% (from 4.25%). The case for 75bps has become a harder sell, given the emotional backdrop.

US FOMC Minutes out early tomorrow morning have been put back into the spotlight given Mester and Bullard’s revelations that they wanted a 50bp hike at the last meeting. Were there any others? And if so does that increase rate volatility which looks to be impacting risk assets? Markets now ascribe a 12% chance of a 50bp hike in March, while terminal fed pricing has also lifted to be above the Fed dot plot at 5.30% by July 2023.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.