Long-term signal vs. Short-term noise

Insight

The FOMC meeting is tonight and markets are being cautious, with little movement in bonds or equities. A weaker than expected set of retail sales numbers has added to the uncertainty.

https://soundcloud.com/user-291029717/retail-sales-numbers-add-to-caution-ahead-of-the-fomc?in=user-291029717/sets/the-morning-call

Markets were cautious overnight ahead of the FOMC meeting later tonight (4.00am Thursday Sydney time). While no-one expects much from the FOMC meeting, Chair Powell will be questioned persistently about whether the Fed is talking about tapering. We think Chair Powell will indicate officials discussed talking about tapering, but tapering itself is still someway off given the Fed remains well short on making substantial progress on employment with payrolls still 7.3m below pre-pandemic levels. There will also be interest in the Fed dot plot and whether the majority of the FOMC see a rate hike in 2023 (previously only 7 out of 18 had pencilled in a 2023 hike) – note the first 25bp Fed rate hike is fully priced for Q2 2023.

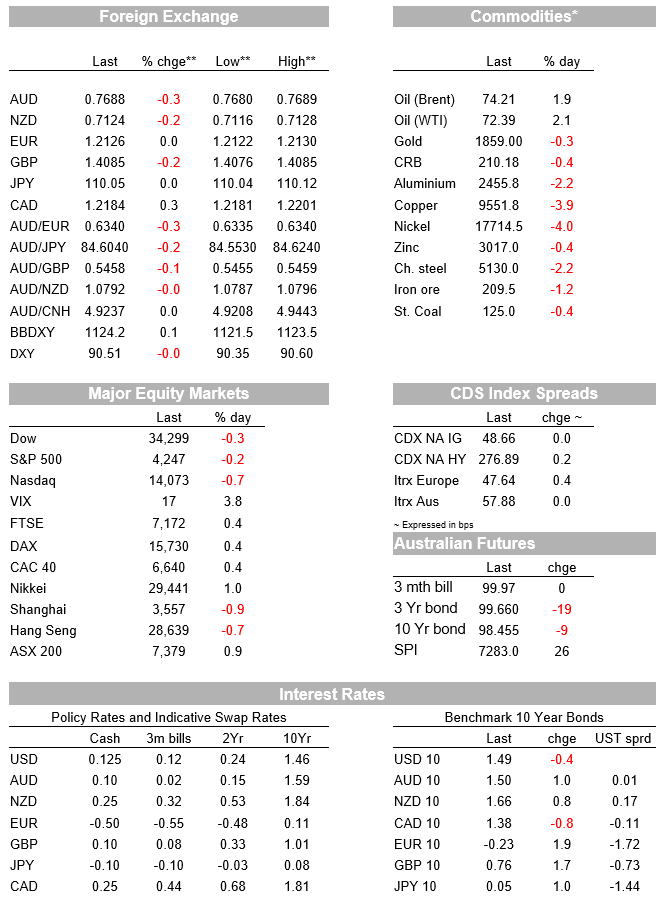

As for market moves overnight, the S&P500 fell -0.2%, easing back just a little from its record high set yesterday. The USD (BBDXY) is up slightly at 0.1%, having reversed some of the slight strength seen in the wake of the weaker than expected US retail sales figures (Headline Sales -1.3% m/m v. -0.8% expected). Yields have been broadly steady with the US 10yr yield -0.4bps to 1.49%. Commodities have seen the biggest moves with copper down -3.9% with falls in other base metals, while oil is up 1.9%. The AUD took its cue from the weakness in commodities, underperforming and down -0.3% to 0.7688.

Data overnight has been plentiful with US Retail Sales the highlight, though markets of course are little moved on most data pieces ahead of the FOMC. Headline Retail Sales fell more than expected in May at -1.3% m/m v. -0.8% expected. The Core Control Measure also fell more than expected at -0.7% v. -0.5% expected. While the print seemed to add to the amount of caution at the time, looking under the hood the retail numbers tell an encouraging story. The prior month was revised higher (April Core Control now -0.4% v. the initial print of -1.5%). The pivot from goods to services also appears underway with spending on restaurants and bars up 1.8% m/m with total sending on food-service sales now above pre-pandemic levels. If a pivot from goods to services is occurring in earnest, that may also alleviate some of the price pressures being seen on the goods side of the economy.

Elsewhere, the US NY Empire Manufacturing Survey fell by more than expected, perhaps a sign that the manufacturing sector is moving past peak growth, even if activity remains very strong in an absolute sense. US Industrial Production also played to that view with the level of manufacturing production now back to the pre-Covid levels and capacity utilisation not being far off pre-COVID levels. A few high-level anecdotes out of the US press also suggest some moderation in end-goods demand with sales at furniture retailers slowing sharply recently after having doubled during the pandemic, while lumber prices have slid more than 40% over the past week. Key for lumber will be the housing starts/permits data later tonight.

The biggest moves have been in base metals with copper prices down 3.9% overnight to around $9,550/ton and are off some 11% from their all-time high reached in May. Other industrial metals such as nickel (-4.0%) and aluminium were also lower. The move in copper prices follows speculation that China might release some of its stockpiles in the next few months, as part of its broader efforts to contain commodity prices, while there are also reports of copper inventories rising in Asia. In contrast, oil prices have continued to push higher, with Brent crude oil rising 1.9% to $74.21, its highest level in over two years. Over the past few days there have been numerous reports citing $100 oil being a real possibility given the confluence of strong demand and constrained supply.

As for FX, it is been relatively quiet. The USD did initially lift in the wake of the weaker-than-expected retail numbers, but has reversed this mostly with the BBDXY now only up 0.1% overnight. USD/Yen (+0.0% to 110.05) and EUR (+0.0% to 1.2163)) are little changed on net, though initially Yen and CHF did see some mild safe haven demand. Commodity currencies have been the laggards given the commodity backdrop with the AUD falling back below 0.77 to be currently 0.7688 (-0.3% on the day). Other commodity currencies have fared similarly with NZD -0.2% and USD/CAD +0.3% despite the strength in oil.

Closer to home, the RBA Minutes yesterday were overwhelmingly dovish, which suggests the RBA is in no hurry to follow the RBNZ or BOC in flagging higher rates in 2022. The RBA still notes inflation is unlikely to be sustainably within the 2-3% band “until 2024 at the earliest”, while also downplaying recent wage anecdotes by noting further increases in the participation rate were possible and that “ firms facing labour shortages were citing a preference for non-wage measures to attract and retain staff….Some firms were also opting to ration output because of labour shortages, rather than pay higher wages…”. The RBA again restates that a return to full employment is “a priority” and concludes that it will not increase the cash rate until actual inflation is sustainably within the 2-3% target and this is unlikely to occur until 2024 at the earliest. As for the July Board Meeting where the RBA will announce its decisions on QE and YCC, the RBA played a fairly straight bat, while also opening up the possibility of moving to a more flexible QE purchase schedule. NAB’s view remains the RBA will not extend the 3yr YCC target from the April 2024 bond to the November 2024 bond and that the RBA will taper QE to $75bn over 6 months in a 3rd round.

A quiet day domestically with only Weekly Consumer Confidence. All international focus will be on the Fed, details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.