Economic and financial market update

Insight

After a negative start, US equities managed to end the day in positive territory supported by better than expected earnings reports from retailers.

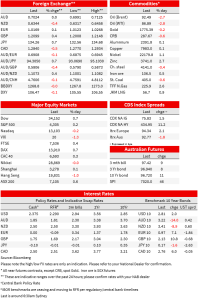

UK: Unemployment rate (%), Jun: 3.8 vs. 3.8 exp.

GE: ZEW survey expectations, Aug: -55.3 vs. -52.7 exp.

US: Building permits (k), Jul: 1674 vs. 1640 exp.

US: Housing starts (k), Jul: 1446 vs. 1527 exp.

US: Industrial production (m/m%), Jul: 0.6 vs. 0.3 exp.

CA: CPI (y/y%), Jul: 7.6 vs. 7.6 exp.

CA: CPI Core (avg, y/y%), Jul: 5.3 vs. 5.0 exp.

NZ: GDT dairy auction price index (% chg): -2.9 vs -5.0

After a negative start, US equities managed to end the day in positive territory supported by better than expected earnings reports from retailers. Walmart has widened its customer base, moving up market. Core global yields reversed yesterday’s decline with the UST curve showing a bear flattening bias. Most G10 currencies are little changed, CAD outperforms after strong Core CPI readings keeps BoC rate hikes expectations elevated while the risk positive backdrop and move up in UST yields weighed on JPY.

US equities had a shaky overnight session, starting the day with a negative tone after mixed US economic data weighed on sentiment (more below), but then better than expected earnings reports from Walmart and house Depot, triggered a turn around with the S&P rebounding to 0.65% after initially being down close to -0.5%. A tech slide close to the end day, trimmed earlier gains with the benchmark closing the day up 0.19%, a third consecutive day of positive returns. The NASDAQ was -0.19% and the Dow was 0.44%. Meanwhile EU stocks extended their recent gains with the Stoxx 600 Index closing 0.2% up and at its highest in more than two months. Miners outperformed along with utilities and telecoms.

Investors embraced Walmart earnings figures which exceeded the market’s diminished profit expectations and modestly improved full-year forecast . US chain’s same-store sales grew 6.5% from a year earlier in the quarter ended July 29, better than the 6% growth it forecast in last month’s update. Walmart also raised its operating income guidance for the full fiscal year ending in January 2023. Food inflation is attracting more affluent customers while lower income customer have stayed loyal. Home Depot also posted better than expected results even as the US housing market showed more evidence of cooling off.

US July housing starts plunged 9.6% to 1,446K, below the consensus, 1,527K while Building permits fell 1.3% to 1,674K, above the consensus, 1,640K. The decline in housing start was primarily driven by the core single-family component, down 10.1%, a fifth consecutive monthly decline. Overall, this is a story of homebuilders responding to a steep drop in demand. Pantheon economics notes more of the same should be expected given this data lags sales, which lag mortgage applications, which are down 30% from their December peak and still falling. In contrast, US Industrial production was stronger than expected at 0.6% m/m in July, driven by a 6.6% surge in motor vehicle production, on easing bottlenecks that are allowing a return to more normal production levels. Excluding the auto sector, manufacturing output rose 0.3% in July, not enough to offset the 0.7% total decline across May and June.

Notwithstanding BoE rate hikes and elevated inflation, the UK labour market remains very strong amid a lack of supply (not helped by Brexit) and an economy that has remained resilient, until now at least. The June report revealed robust job growth and an unchanged unemployment rate of 3.8% alongside higher wage inflation, with average weekly earnings of 4.7% y/y (ex bonuses). Of note, the data may be showing some crack in labour demand with a 19.8K drop in Job vacancies in the May-July quarter, the first quarterly fall since Aug 20. Still very high at 1.274m, 0.479m above Mar 20 pre-pandemic levels and +32.1% y/y. The BoE debate remains whether the Bank will judge the strength in average weekly earnings as problematic or whether the real income erosion is enough the bring inflation to heel.

Core global yields reversed yesterday’s decline, aided by the positive equity backdrop. In Europe, 10y Bund yields gained 7bps to 0.97% and after the UK labour data 10-year gilt yields jumped 11bps to 2.13%. Meanwhile in the US, the 2y yield lead a bear flattening of the curve, up 8bps to 3.265% while 10y UST yields gained 2bps to 2.8090%.

In currency markets, CAD has been the top performer overnight, up 0.4% following stronger than expected core CPI readings and despite of a 3% decline in oil prices. Canadian CPI inflation showed the expected cooling of the headline rate, down to 7.6% y/y, but core measures continued to rise, with the three key measures all rising to reach a 5-5½% range, adding to the chance of more “front-loaded” tightening from the Bank of Canada, with the 2-year bond rate up 13bps on the day. Meanwhile the decline in oil prices (Brent now $92.70) has been largely attributed to expectations the Iranian deal, which would imply an extra 1.3m oil barrels per day, may be approved, at least based on EU commentary, although the decision still largely depends on the US and Iran agreeing the terms.

The move up in UST yields and relatively buoyant equity backdrop, sees JPY as the G10 underperformer, down ~0.75% to ¥134.23 while pro-growth currencies such as AUD and NZD are little changed. Overnight the AUD briefly traded sub the 70c mark but opens the new day at similar levels to yesterday’s opening at 0.7023. The NZD traded down below 0.6320 overnight, but higher risk sentiment and a turnaround in the USD sees the NZD trading just under 0.6350.

Economic and financial market update

Insight

Online retail sales growth slowed in March

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.