NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Strong earnings have swept away Delta concerns in the US with 85% of companies reporting so far beating expectations.

https://soundcloud.com/user-291029717/risk-back-on-with-rebound-expectations?in=user-291029717/sets/the-morning-call

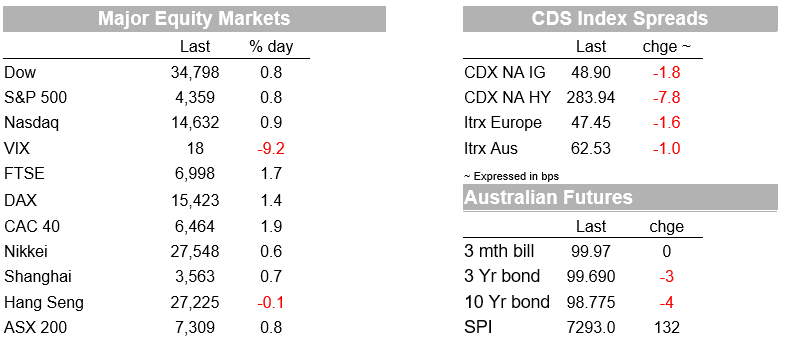

Strong earnings have swept away Delta concerns in the US with 85% of companies reporting so far beating expectations. The base case in the US is that the rise in delta infections will not see restrictions tightened and although vaccination rates differ by state, 79.5% of the over 65 years population is now fully vaccinated. The S&P500 rose 0.8% with eight of the eleven sub-sectors in the green. Across the pond the Eurostoxx600 was +1.7%. Companies reporting showed a strong re-opening theme with 85% so far beating expectations. Notable anecdotes included Chipotle (+11.5%) which saw revenues surpass pre-pandemic levels, Coca Cola (+1.3%) raising its outlook after beating expectations, and United Airlines (+3.8%) reporting a surge in airline travel and expects it to continue.

Earnings season has also brought with it a slew of inflation anecdotes amongst manufactures with many seeing inflation pressures higher and longer than expected. Unfavourable frost conditions in Brazil has also seen coffee futures soar 5%, the frosts coming after a prolonged period of in the Americas (La Nina has meant the reverse in Australia with two years of bumper harvests and a negative Indian Ocean Dipole likely making another bumper year). The key uncertainty for inflation though is whether these cost pressures are persistent and whether they are passed onto retail prices. As economies reopen, the supply side should start to recover at the same time as concentrated goods demand abates given some likely bring forward of consumer demand driven by stimulus.

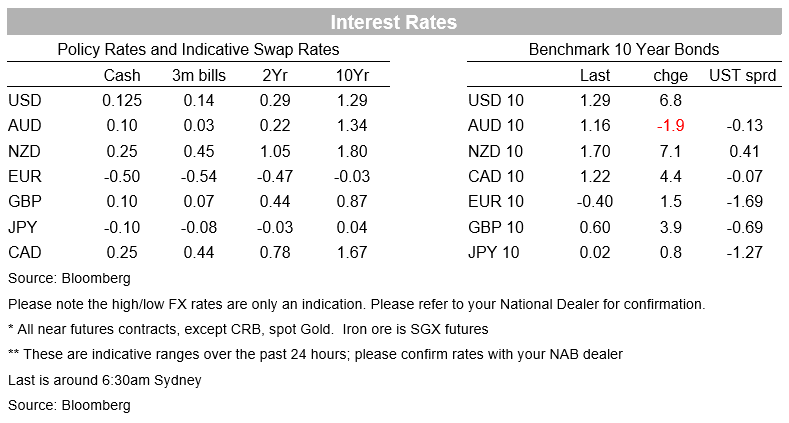

The US 10yr yield which had only recently touched an intra-day low of 1.1260% on Tuesday, is up 6.5bps to 1.29% and is back to where it was on Friday. Breaking up the 10yr yield shows the move in yields has been driven by both the inflation breakeven 3.2bps to 2.30% and the real yield +3.5bps to -1.02%. Overall the implied inflation breakeven is broadly consistent with PCE inflation being at the Fed’s 2% target, so markets are still holding to the transitory line.

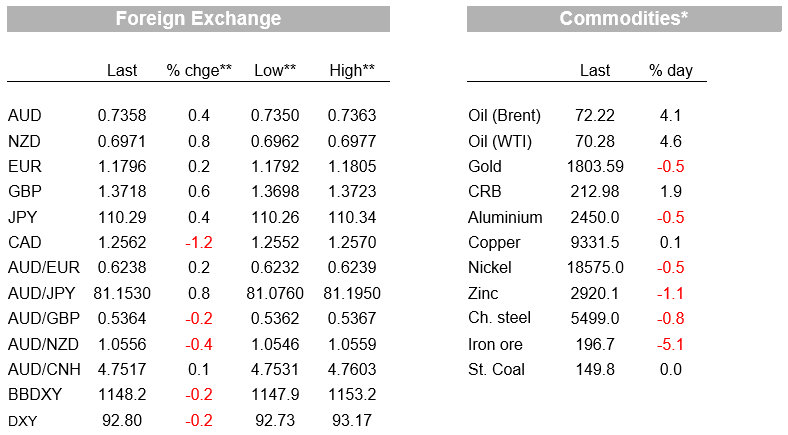

FX moves has also seen some caution abate, with USD/YEN +0.3% and global risk proxies up (AUD +0.4% and NZD +0.8%). The USD is down (BBDXY -0.2%) amid broad-based falls amongst most currency pairs, while a recovery in oil (Brent +4.2%) has also helped USD/CAD -1.2% outperform. GBP has also rebounded around 0.6% after being hit hard early this week, the market ignoring the return of Brexit headlines. Arguments over the Brexit deal headline the FT this morning, with the EU insisting that it will not renegotiate the deal after the UK warned it was willing to suspend part of the deal unless the EU agreed to new trading rules for Northern Ireland.

Despite the recovery in risk sentiment, the AUD remains on a 0.73 handle at 0.7358 and in APAC yesterday made a fresh year-to-date low of 0.7290. The moves came in the wake of a report that some Chinese steel companies in Jiangsu province received guidance to rein in output from last year’s levels with the pressure to cut falling in August through to December, as well as after the sharper than expected fall in Australian retail sale (-1.8% m/m vs. -0.7%). The fall in retail sales signals that lockdowns in Australia will have a severe impact on growth.

With the August RBA meeting less than two weeks ago, speculation continues that the RBA will reverse its decision to taper QE purchases to $4bn from $5bn a week from September. Smoke signals from the RBA continue to be sent by the media with James Glynn writing yesterday “keeping bond purchases at A$5 billion per week in September would also demonstrate the RBA’s willingness to be flexible in times of renewed uncertainty”, while also pushing back on some calls to increase the pace of QE to beyond $5bn (“Raising RBA Bond Purchases a Break-Glass Option Only ”) (see The Australian for details).

As for Delta concerns, they remain, but the consensus is that it does not pose an immediate risk to the recovery. At most given effective vaccines, delta pushes out the recovery by a quarter as countries seek to vaccinate a higher share of their respective populations before fully repealing virus restrictions. Studies continue to show high vaccine efficacy and the UK is being watched closely as to whether hospitalisation and death rates can remain low as the delta variant spreads through unvaccinated cohorts, which are mostly younger and are less effected by COVID-19.

A quiet day domestically with only second-tier data scheduled. Offshore the highlight is the ECB meeting: Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.