Price growth edges lower despite reasonable economy

Insight

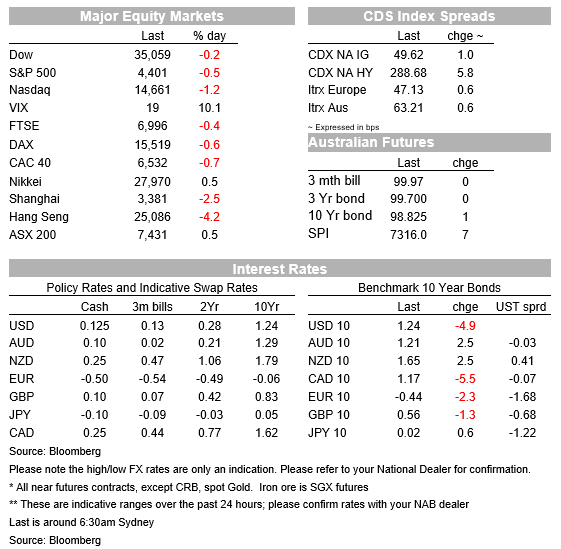

For the first time, we are now seeing contagion from the sell-off in Hong Kong and US-listed Chinese shares, to global markets – the NASDAQ in particular, ending the day down 1.2% in front of the earnings results from Apple, Alphabet and Microsoft.

https://soundcloud.com/user-291029717/rocky-road-for-china-investors?in=user-291029717/sets/the-morning-call

This song title – from one of the great British punk rock bands – had admittedly been used before, two years ago in fact when the protests on the street of Hong Kong were at a peak and the airport had just been closed following mass demonstrations. But we figure the statute of limitations has since run out and such a great song is due another airing, after the Hang Seng index ended 4.2% to bring its loss for the week so far to 8.5%.

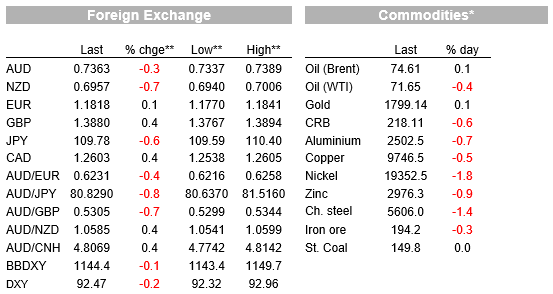

For the first time, we are now seeing contagion from the sell-off in Hong Kong and US-listed Chinese shares, to global markets – the NASDAQ in particular, ending the day down 1.2% in front of the earnings results from Apple, Alphabet and Microsoft. We also see bull flattening in the US Treasury market where 10s are off 5.5bps, while in currencies the safe-haven characteristics of the USD are being somewhat obscured by strength in the Swiss Franc and Japanese Yen, arithmetically supporting USD indices (EUR/USD is also a little firmer). AUD, NZD, CAD and NZD are all suffering though, AUD -0.3% to 0.7362 (not too bad in the circumstances). It’s a fair bet that what happens in Chinese and Hong Stock market today might be the bigger influence on the local market than this morning’s Q2 CPI report and the announcement expected from the NSW Premier this morning than the current lockdown is to extend at least through August. Whether or not the construction sector, at least in most of Greater Sydney, can get back to work will be of keener interest here, in terms of calculating the scale of the ongoing hit to the NSW economy.

The Hang Seng indeed and to a lesser extent Shanghai indices were under significant pressure throughout the APAC day yesterday but with losses accelerating into the close (in the case of the Hang Seng, perhaps not helped late in the day by news that the first person to be tried under Hong Kong’s new security laws had been found guilty by the presiding judge). This was largely incidental though, and where it is the exodus from not just Chinese technology stocks listed in Hong Kong and elsewhere, but in the education and property development sectors and where firms’ ability to continue operating profitability under a new regulatory environment is being called into question, which is why they being subjected to such acute price pressure. The NASDAQ Golden Dragon Index (covering 98% of Chinese shares listed in the US) is now down some 20% from its peaks.

Weakness in US share market doesn’t have much to do with covid developments, even though infection numbers there continue to rise (daily totals above 60,000) and in many places restrictions, such as mandatory mask wearing, are being put back in place. On the positive side, UK infections continue to fall, to below 25,000 on Tuesday and with the 7-day average down to 32,275 from 35,546. though hospitalisations are up – to 5,918 as of 5 days ago from 5,238 the day before, while the daily average of deaths has also crept up (68.6 from 63.1). the UK experiment with re-opening does though by and large look to working without overwhelming the National Health Service.

Incoming US economic data has also not been to blame for equity market travails. US durable goods orders were softer than expected in headline terms in June at 0.8% against 2.2% expected, though the ‘Capital goods orders ex-defence ex-aircraft’ sub-series, the best measure of underlying new orders, was 0.5% against 0.7% expected but with May revised up to 0.5% from 0.1%. Meanwhile Consumer Confidence, as measured by the Conference Board, rose to 129.1 from 128.9, well above the 123.9 expected – no sign here of rising covid infections yet dampening consumer spirits. And the Richmond Fed Manufacturing index lifted to 27 against 20.0 expected with June revised to 26 from 22.

After the NYSE close, Apple reported Q2 earnings of $81.4bn against a consensus for $73.82 (wow); Alphabet $50.95bn vs. the $46.08bn street consensus and Microsoft $46.15bn vs. $44.26bn expected.

In front of the conclusion of the two-day FOMC meeting tonight, another bull flattening move in US Treasuries where 10s are currently -5bps (as is the 30-year) to 1.24% and the 2-year note down 0.6bp to 0.204%. Earlier European bonds ended with the 10year German Bund down 2.4bps to -0.444% – a lucky Chinese number there, perhaps they’ll be buying it some more later today.

In currencies it’s the pro-cyclical/commodity currencies that have all suffered on the coat-tails of the risk-markets sell-off, with NZD and NOK both down 0.7% on Monday’s close and AUD and CAD a lesser 0.3% and 0.4% respectively. The JPY tops the leader board, +0.6% to see USD/JPY back below Y110 with CHF not far behind at +0.44%. CHF and JPY gain (together with a 0.1% rise in EUR/USD) has allowed for the DXY USD index to be weaker, -0.17%.

Finally, in commodities, oil has held in with a 0.2% gain for Brent crude but metals prices are all lower, albeit only modestly, led by a 1.8% fall nickel and 1.4% for steel futures, the latter following news yesterday afternoon that the Chinese authorities may soon impose new duties on steel exports.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.