Total spending grew 0.9% in June.

Oil prices have recovered somewhat and equities have risen again.

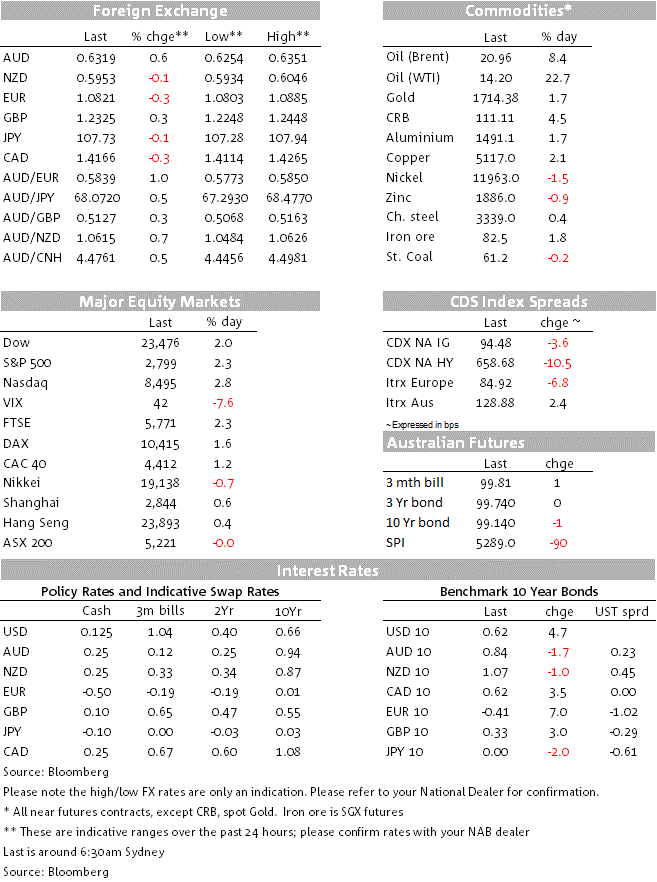

Risk sentiment has taken a fresh turn for the better overnight, aided by a decent bounce in oil prices and media reports – confirmed post European close – that the ECB will include sub-investment grade debt in its bond buying armoury. The latter sees Italian bonds buck the trend of higher benchmark yields elsewhere though hasn’t helped the EUR. The USD is marginally firmer but AUD is the best performing major currency of the last 24 hours, +0.7% to 0.6320.

Statistics have been somewhat mixed and not a major market driver overnight,. The trend in new infections in New York remains down and the death toll has fallen to its lowest since early April, though Italy posted the highest number of new cases in four days. Singapore reported more than 1,000 new cases for the third day running while in Spain the prime minister’s request to extend the state of emergency through May 9 has been approved by parliament (Bloomberg reports).

The oil price bounce, by 20% for the June WTI contract to around $14 and by 7% to just under $21 for Brent, hasn’t had an obvious catalyst, though some are pointing to an edict from President Trump for US forces to shoot and destroy any Iranian gunboats harassing US military ship in the Middle East, as they reportedly have been in recent days. The latest oil inventory stats from the EIA, meanwhile, show a 15 million barrel build. The oil price rally has seen the energy sector of the S&P 500 rally by around 4% – though so too has the IT sector – leading the 2.3% run-up in the overall index just in front of the close. European stocks market earlier closed with gains of between 1.25% (CAC 40) and 2.25% (FTSE 100).

Incoming corporate earnings don’t look to have been a major influence, Kimberly Clark the latest to cancel forward guidance and earlier share buy-back intentions. A little surprising perhaps given they are the world’s biggest suppliers of toilet tissue (presumably they see the recent surge in sales on panic buying as a ‘flush in the pan’ – Ed?)

The improved risk appetite has its mirror image in higher benchmark bond yields bond yields, US Treasuries +5bps at 10 years to 0.62% and 5s +3bps to 0.36%, up from Tuesday’s record low of 0.29%. European government bond yields also rose overnight, except for Italy, which saw yields fall after reports (since confirmed) that the ECB was considering accepting high-yield bonds as eligible collateral in its operations.

Italy’s credit rating is just above the high-yield threshold and it’s conceivable that it is downgraded below investment-grade this year. But the ECB announced a short while ago that it will accept all bonds (including corporates and banks) in its lending operations that were ratings-eligible as at 7th April 2020 (until at least September 2021). The move formalises what it is already doing with sub-investment grade Greek government bonds, which it accepts as collateral and purchases in its QE programme. The announcement also opens the door for the ECB to buy high-yield corporate bonds at a future point, following the lead of the Fed.

It’s been a mixed night for G10 currencies, the BBDXY USD index 0.15% stronger led by a 0.34% fall in the EUR (the above ECB news notwithstanding). AUD (0.65%) CAD (+0.35%) and GBP (+0.33%) are firmer while the NOK is somewhat surprisingly 1% lower despite the oil price pop, confirming that trading this particular currency is not for the faint-hearted.

AUD/USD strengthened yesterday in the wake of the preliminary March Retail Sales data. The history books will record the eye-popping 8.2% monthly rise as the reason, though the move higher only occurred half an hour after the data was released. Strange days indeed. This was the largest monthly rise in sales since monthly data became available in 1965, marginally surpassing the 8.1% rise in June 2000 when spending was brought forward ahead of the introduction of the GST in July. The ABS said there was sharp increase in the purchase of essentials, where monthly sales volumes doubled for toilet and tissue paper, rice and pasta, while sales of canned food, medicinal products and cleaning goods rose by more than 50%. The ABS also pointed to strong demand for goods needed to work from home. These factors more than offset a sharp fall in spending at restaurants, apparel retailers and department stores, which were most affected by containment restrictions.

The March result is likely to be quickly unwound. Early indications are that the panic buying at supermarkets is subsiding, assisted by limits on some purchases. At the same time, some spending, such as at cafes and restaurants, has of course stopped completely given stricter health measures.

Flash Markit April PMI data for the Eurozone, UK, US, Japan and (lesser watched) Australia hold centre stage on the economic calendar.

For the pan-Eurozone reads, consensus for Manufacturing is 38 from 44.5 in March, Services 22.8 from 26.4 and Composite 25.0 from 29.7. The UK Composite is seen at 29.5 from 36.0. For the US, consensus is 35 from 48.5 for Manufacturing and 30.0 from 39.8 for Services.

The US also has weekly jobless claims (consensus +4.5 million) and in the UK March Retail Sales (consensus -4% ex auto-fuel) but where after yesterday’s Australian +8.2% retail sales print the risk must be that economists have seriously low-balled the extent to which panic buying boosted overall retail sales.

EU leaders hold a video conference to rubber stamp the recent FinMin agreement on pandemic economic response mechanisms and the amounts therein, but will likely also be initiating discussion – and probably no more than that at this stage – on a longer term Recovery Fund, potentially utilising the 2021-2027 EU Budget.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.