Uncertainty remains high ahead of July reciprocal tariffs

Insight

Inflation fears are clearly lifting, with the latest driven by the rise in energy prices.

https://soundcloud.com/user-291029717/shares-rising-despite-everything-please-explain?in=user-291029717/sets/the-morning-call

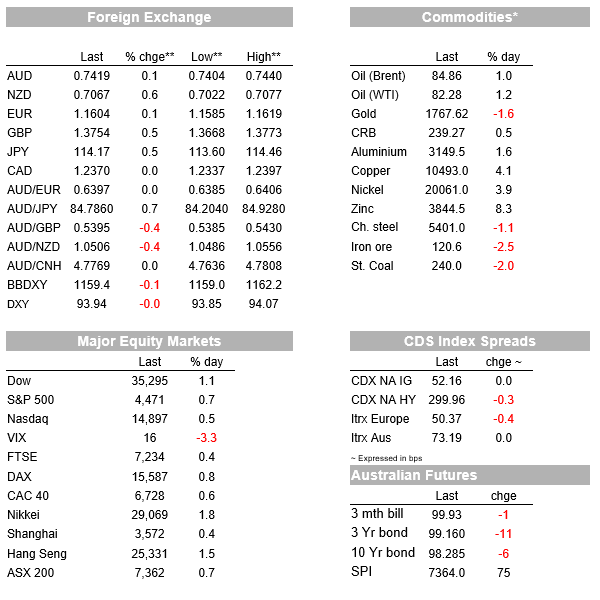

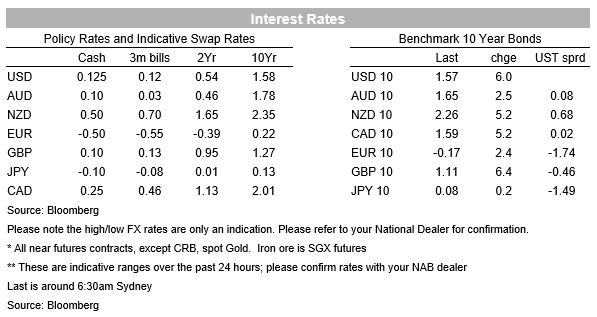

Central banks are set to hike in response to higher transitory inflation with BoE Governor Bailey penning on Sunday that “the energy story means [the period of high inflation] will last longer” and that the BoE will “have to act and must do so if we see a risk, particularly to medium-term inflation and to medium-term inflation expectations”. Markets fully price a BoE rate hike by December 2021, while across the pond US Fed pricing has also moved forward with a 50% chance of a June 2022 rate hike and rate hike is now fully priced by September 2022. How risk markets respond to the bringing forward of rate hike expectations will be key to watch this week, as will anecdotes from the profit reporting season to see how firms are dealing with higher input costs and to what extent they are able to pass this onto consumers. As for Friday’s moves, risk markets were positive with strong earnings and a solid beat on US Retail Sales seeing the S&P500 +0.7% to close the week up 1.8% and is now just 1.4% below its September record high.

Yield curves twist flattened again given the dynamics of bringing forward hike expectations, elevated inflation concerns, and notions of the Fed responding more aggressively and thereby perhaps slowing the economy. As noted above markets now price 50% of a rate hike by June 2022, meaning little gap between the end of tapering and the start of the hike cycle. On Friday the 2/10s curve steepened, up 2.5bps to 117.3bps, while the 5/30s curve flattened down another -4.9bps to 91.49bps. However, over the week though the 2/10s curve is lower by 11.5bps, while the 5/30s curve is down a sharper 18.5bps. The flattening in the curve over the past week is consistent with markets pricing in a more aggressive Fed and also lowering its estimate of where the terminal Fed Funds rate may be. Terminal Fed Funds proxies such as the 5Y1Y FWD OIS ended the week down 17.1bps to 1.66%. As for moves in the 10yr yield on Friday, this was driven by both the implied inflation breakeven (+2.8bps to 2.56%) and the real yield (+3.2bps to -1.0%).

Inflation fears are clearly lifting, with the latest driven by the rise in energy prices. Brent oil prices were up 1.0% on Friday to $84.9 a barrel. The lifting of international travel restrictions to the US is also likely to lead to increased oil demand from the aviation sector at a time of elevated demand due to the energy crisis in Europe. The lift in headline inflation is feeding into inflation expectations with the Fed’s benchmark measure of expectations (the Common Inflation Expectations Index) at its highest since 2014 at 2.06%. In a sign that employees have indeed regained bargaining power, strike action is on the rise in the US with Bloomberg reporting employees on strike at nearly 40 companies across the US, including John Deere and Kelloggs in what is being referred to as ‘strike-tober’. The Atlanta Fed’s Wage Growth Tracker which controls for compositional effects shows annual wage growth at 4.2% in September, its highest level since just before the GFC, while the rate of wage growth for those switching jobs was 5.4%, its highest level since 2002.

The rise in inflation concerns may also be a factor for why US Consumer Sentiment has failed to bounce for the second consecutive month (71.4 vs. 73.1 expected) with the index sustaining the lows first recorded at the height of the pandemic in 2020. The 1yr ahead inflation expectation increasing to 4.8% from 4.6% to be at its highest since August 2008. The more important 5yr ahead though fell two tenths to 2.8% from 3.0%. When respondents were asked to describe in their own words why conditions were unfavourable, net price increases were cited more frequently than any time since inflation peaked at over 10% in 1978-80. This is potentially important. At least one prominent economist is warning of US recession risk given the sharp drop in consumer confidence since April 2021 – Blanchflower and Bryson (2001): The Economics of Walking About and Predicting US Downturns note that all US recessions since the 1980s have been predicted by at least 10 and sometimes many more point drops in consumer sentiment, and argue “there is every likelihood that the US is entered recession at the end of 2021”). For its part the write-up of the consumer sentiment report highlighted a slump in confidence in the government’s economic policies (lowest since September 2014).

The fall in consumer confidence though is yet to weigh on the economy with Retail Sales beating expectations with a the core control group +0.8% m/m vs. 0.5% expected. A delayed back-to-school shopping season may have boosted September’s numbers. The extent to which subdued confidence weighs on consumer spending will be closely watched. Given pandemic stimulus, households are sit sitting on roughly $1.6 trillion in savings, representing 9.4% of their disposable income. The retail sales beat combined with strong earnings saw the S&P500 up 0.7% and is now just 1.4% off its record high. Goldman smashed expectations with profits of $14.93 a share against $10.14 a share expected and Goldman stock closed up 3.8% on the day. So far of the 41 companies to report, 80% have beaten expectations. This week brings the first tech stocks to report with Netflix on Tuesday, Tesla and IBM on Wednesday, and Intel on Thursday. Focus will also be on industrials and materials for inflation signals with J&J and Procter & Gamble on Tuesday.

Currency moves were fairly restrained on Friday, the USD down around 0.1% in index terms, while the JPY continues to underperform against a backdrop of improving risk appetite and rising global bond yields. USD/JPY was 0.5% higher on Friday, closing the week at a 3-year high, around 114.20. The GBP was the best performing currency on Friday (+0.6%) amidst firming expectations that the BoE will kick off a tightening cycle before the end of the year, while the NZD also performed well, up 0.45% to around 0.7070. The AUD was flat on Friday, seeing the NZD/AUD cross trade back above the 0.95 mark, a gain of 0.5%. On the week, it was, unsurprisingly, a story of commodity currency strength, with the NZD leading the pack with a 1.85% gain, the AUD up 1.5% and the NOK and CAD seeing gains of 1.3% and 0.8% respectively. With the JPY falling 1.8% last week, NZD/JPY saw a big 3.6% appreciation to its highest level since the start of 2018, around 80.70.

Finally in Australia, VIC is set to follow NSW and the ACT in re-opening, bringing forward its re‑opening date to Friday October 22 (from October 26). NSW also starts its second stage of re-opening today with masks no longer required in offices (a relief to your scribe) after having hit 80% full adult vaccination (currently 80.3% are fully vaccinated, while those with at least one dose sits at 92%). Meanwhile progress on easing the international border is set to occur earlier than expected with NSW set to lift quarantine requirements for fully vaccinated travellers and lift incoming traveller caps from November 1. Although the removal of quarantine requirements will only extend to Australian residents/citizens and their families at this stage, this is the first sign of international border restrictions easing in Australia, while the removal of quarantine requirements may see a faster resumption of migration when migration resumes. A return of net migration should ease emerging labour shortages and reduce upward pressure on wages.

A quiet week for Australia with no top tier data and only the RBA Minutes of note. Internationally most of the highlights are today with NZ Q3 CPI and Chinese GDP. Two other events for China are also worth watching with Evergrande’s grace period for the 30 day interval on the USD bond coupons coming to end on the weekend, while the China’s National People’s Congress meets for five days which could see a continued regulatory crackdown. The Q3 earnings season also continues with a number of key names reporting this week including Netlifx, Tesla, J&J and Proctor and Gamble to name a few.

A very quiet day domestically with the only item being the RBA’s Head of International Department being on a panel. There will though be just as much domestic focus on NZ CPI as an indicator for Australian CPI the following week, as well as Chinese GDP figures. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Uncertainty remains high ahead of July reciprocal tariffs

Insight

Australian carbon project developers see a maturing of institutional financing as key to scaling the market and taking it on a similar trajectory as renewable energy.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.