NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

NAB's Rodrigo Catril says the Canadians are out shopping; we also saw a big increase in purchase prices in Germany, in fact the largest monthly rise since 1949.

NZ: Trade balance (ann $b), Jul: -11.6 vs. -10.9 prev.

UK: GfK consumer confidence, Aug: -44 vs. -42 exp.

JN: CPI (y/y%), Jul: 2.6 vs. 2.6 exp.

JN: CPI ex fr. food, energy (y/y%), Jul: 1.2 vs. 1.1 exp.

GM: Jul PPI +5.3%mom vs 0.7% exp.; +37.2% yoy vs 31.8 exp.

UK: Retail sales ex auto fuel (m/m%), Jul: 0.4 vs. -0.3 exp.

CA: Retail sales ex auto (m/m%), Jun: 0.8 vs. 0.9 exp.

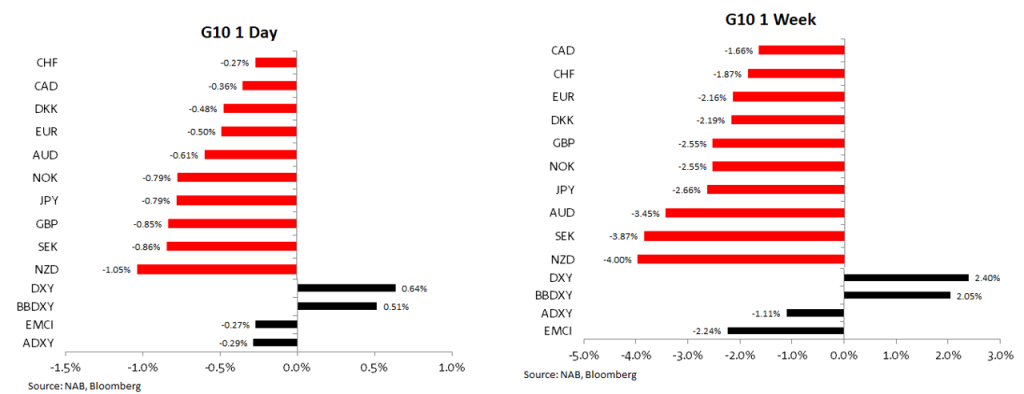

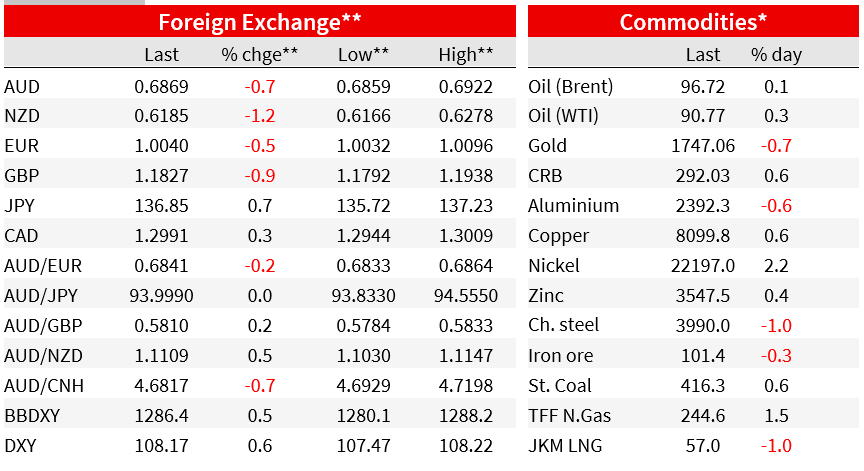

The move up in core global bond yields which began during our time zone on Friday accelerated during the European session as bond investors reassessed the hawkish message from Fed speakers ahead of the Jacksons hole symposium this week. European data releases did little to dissuade the notion that that more Central Bank work is needed to bring inflation to heel. After four consecutive weeks of positive returns, US equity investors got that sinking feeling with equities down on Friday and on the week. Against a backdrop of uncertainty, the USD proves yet again the be the safe-haven of choice, stronger across the board. USD/CNY was a notable mover on Friday, trading above 6.80 while NZD was the G10 underperformer on Friday and on the week. AUD was not far behind, down 4% on the week, opening the new week at 0.6869.

The idea that bonds can provide diversification to equity investments was yet again refuted on Friday with the move up in yields sparking a broad risk off session with King Dollar the main beneficiary. We didn’t have a specific catalyst triggering the bond sell-off but ahead of Jackson Hole this week, it seems that bond investors decided to brace themselves for Fed Chair Powell to remind everyone that the Fed has not yet pivot and while we may be close to the end of the beginning of the current tightening cycle, we are still a long way from the end.

Recent Fed speakers have been stressing the message that more rate hikes are coming given the fight against inflation has not yet been won. On Thursday last week Fed Bullard reiterated his call for another 0.75% hike and on the same day Fed George also suggested more rate hikes are needed although she was more circumspect and didn’t suggest a hike magnitude. Then on Friday, Fed Barkin said the Fed will “do what it takes” to tame price rises. Noting that “There’s a path to getting inflation under control but a recession could happen in the process,”. Also on Friday, speaking to CNN Fed Daly, who has been quite dovish in the past said, “The job market is strong, inflation is too high, and the Federal Reserve is committed to using its tools to bring the economy back to a sustainable path where people don’t have to wake up every morning worrying about whether their real wages are eroding”.

Meanwhile, European data releases added further fuel to the notion that central banks need to do more to win the fight against inflation. Germany’s PPI set a new yoy record, skyrocketing by +5.3%mom vs 0.7% expected, taking the yoy reading to +37.2% vs 31.8% expected. That was a huge number, but with gas prices on the rise again, a new record may well be around the corner. TFF natural gas futures rose 2.35% on Friday and now they are up around 33% month to date. On this score worth highlighting too that Gazprom announced on Friday that it will be halting Nord stream 1 gas supplies to Europe for three days at the end of the month, given the pipeline’s only remaining compressor requires maintenance.

Speaking to Rheinische Post on Friday, Bundesbank Chief Nagel, warned that Germany faces a recession if the energy situation escalates . Arguably this is happening already, Russia is clearly weaponising gas supplies to Europe with the situation exacerbated by a recent dry spell that has made the Rhine River – vital for the transport of fuel and other industrial goods — difficult to navigate. Importantly, and like the recent Fed messages, Nagel said “Given high inflation, further interest-rate hikes must follow” adding that “I am convinced that the Governing Council of the ECB will take the necessary monetary-policy measures.”

UK retail sales also surprised to the upside, sales volumes including autos fuel rose by 0.3%mom in July, versus a 0.3% decline expected. The resilience of the UK economy has been a surprising feature in recent months, but it is hard to see it will last, given the huge burden consumers face from higher energy bills and rising interest rates. Thus, the main take away from Friday’s data is that inflation and demand are not falling yet.

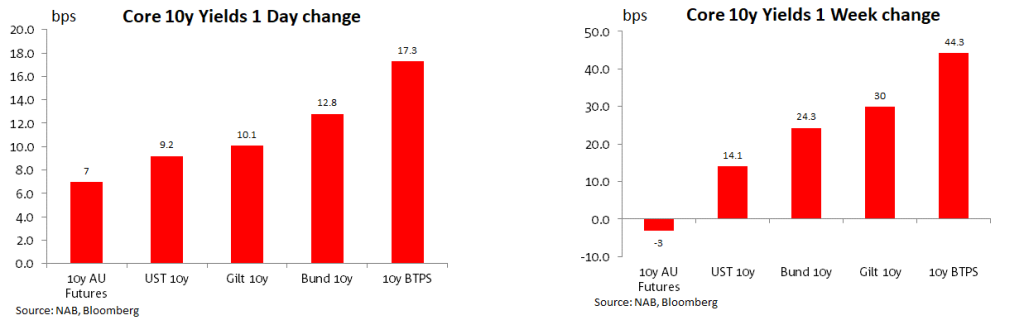

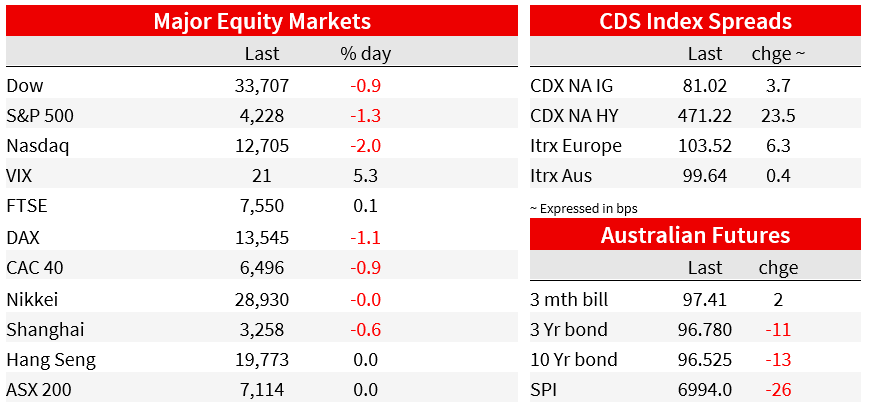

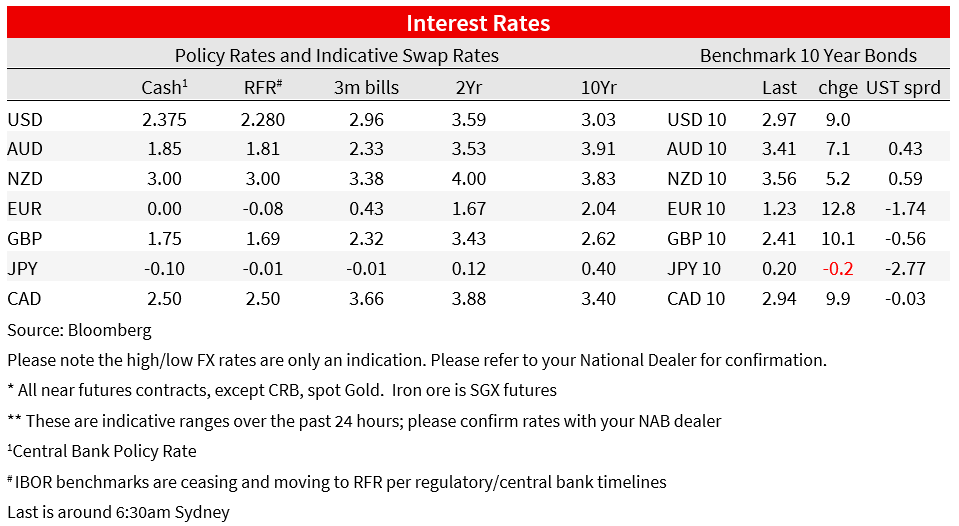

Against this backdrop, global bond yields closed the week under pressure, rising on both side of the Atlantic. UK 10-year yield climbed by the most in five years this week, up 30bps to 2.406% while its 2-year peer surges by the most since 2009, up 44bps and closing the week at 2.46%. 10y Bund yields rose 13bps to 1.24% on Friday and in the US, 10y UST rose 9.2bps, closing the week just shy of 3% (@2.96%). Curve steepening was the order of the day, with the US 2y10y yield curve steepening 5bps although, at -26bps, it remains deeply inverted and consistent with the US economy heading into recession next year.

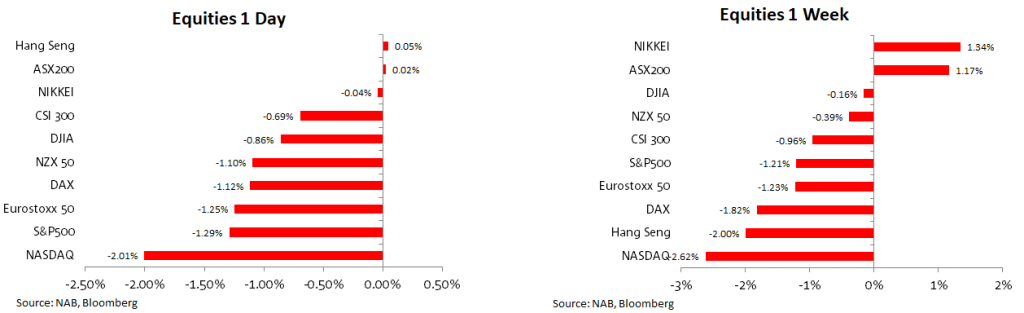

US equities fell on Friday (S&P 500 -1.29%, NASDAQ -2.0%) and on the week, ending a streak of 4 consecutive weekly gains. The move up in yields and prospect of hawkish messages coming from Jackson Hole were noted as the main catalysts for the sell off. From a technical perspective, many also noted the S&P 500 failed multiple times to take out the 200-day moving average around 4,320 and closing below the psychological 4,300 level.

Meanwhile in Europe, the Stoxx 600 index posted its worst week in a month given similar concerns around rampant inflation, the need for more hikes from the ECB and prospect of no gas from Russia. about the impact of future interest-rate hikes aimed at curbing inflation. The Stoxx Europe 600 index fell 0.8% on Friday and declined by the same amount in the week.

Against a broad risk off backdrop, the USD was the only place to be in FX land with the greenback stronger across the board. In index terms BBDXY and DXY gained 0.51% and 0.64% on Friday, closing the week over 2% higher. USD/CNY was a notable mover on Friday, making a decisive move above 6.80, in recent months the pair has founded difficult to sustain moves above the 6.80 mark, but with Fed-PBoC policy divergence and challenging domestic economic environment in China, the move in CNY this time looks more sustainable. This is an important dynamic for the AUD and NZD, we have noted that history tells us that antipodean currencies tend to struggle when CNY endures big depreciating moves.

NZD was the big underperformer on Friday (down 1.05%) and on the week (-4%) and now starts the new week at 0.6194. The AUD was not too far behind, down 0.61% on Friday and 3.45% on the week. After trading above 71c a fortnight ago, the AUD opens the new week at 0.6869. Jackson Hole is the big event for the week, but ahead of that China will be in focus with LPR cuts expected today (see more below) while news of energy cuts due to a heatwave is unlikely to help sentiment.

USD strength is also a by-product of weakness in the EUR, which is battling surging gas prices and staring down the barrel at a recession. The EUR was 0.5% weaker on Friday, ending around 1.0040, with another charge below parity looking just a matter of time. USD/JPY was 0.8% higher amidst the sharp increase in US Treasury rates, closing the week just below the 137 mark.

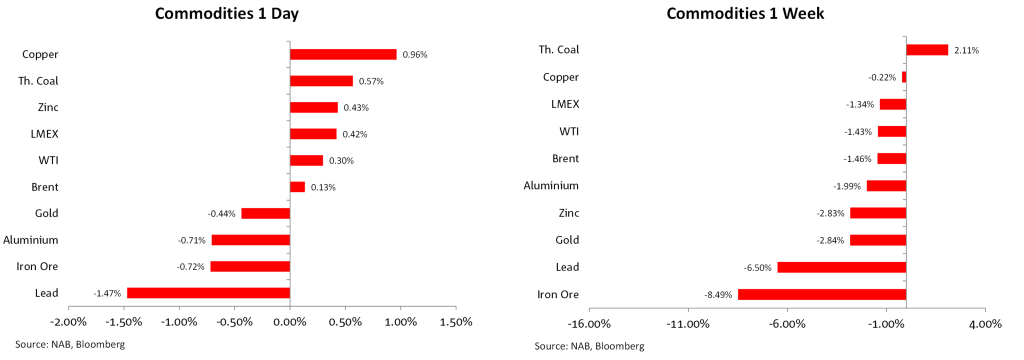

A final word on commodities, copper was well bid on Friday, up close to 1%, while iron ore and lead were the underperformers both on Friday and on the week , iron ore close the week at $101.4. Oil prices were little changed on Friday and down over 1% for the week.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.