Online retail sales growth slowed in May following a fairly strong April

Insight

A quiet night overnight given shortened pre-holiday trade in the US ahead of Independence Day today.

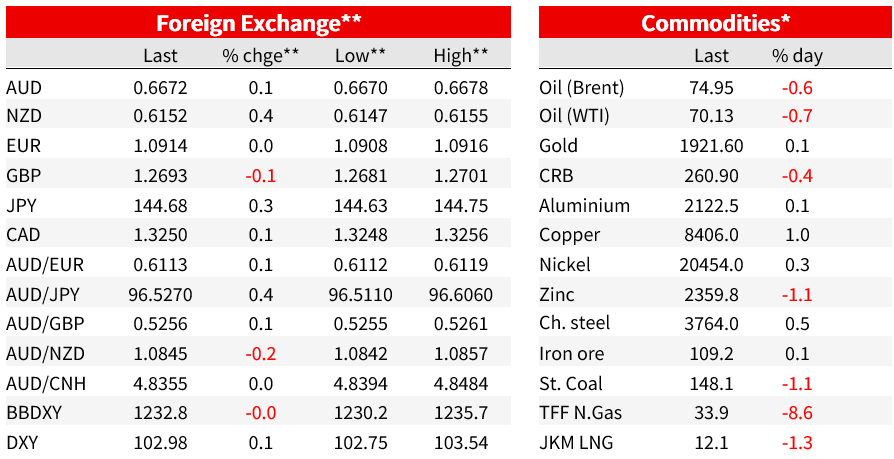

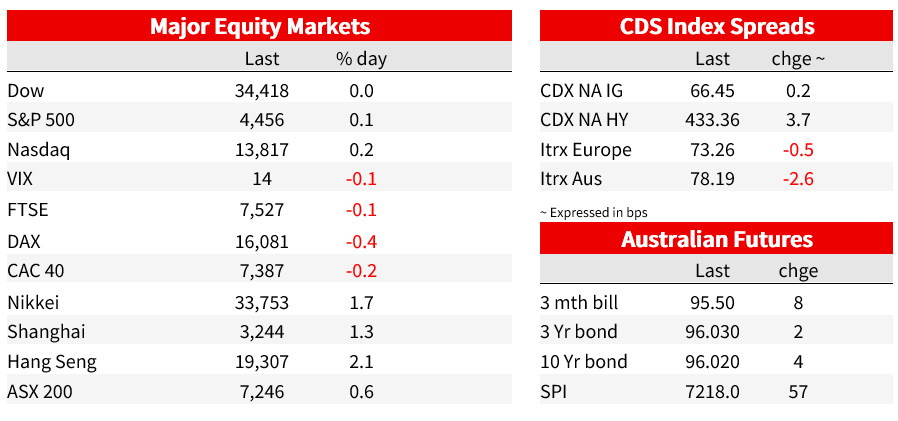

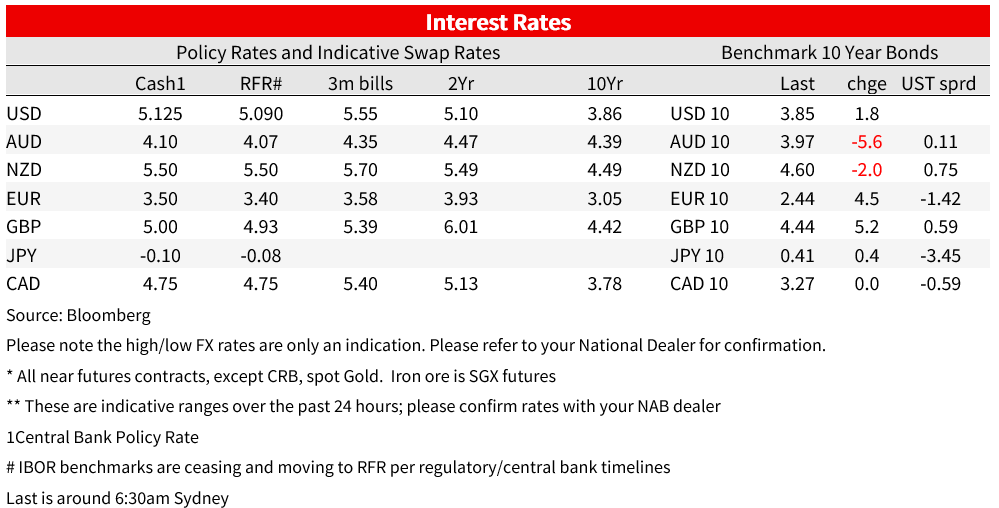

A quiet night overnight given shortened pre-holiday trade in the US ahead of Independence Day today. Data printed on the weak side, though the initial market reaction was not sustained. The US ISM Manufacturing came in at 46.0 vs. 47.1 expected and 46.9 previously, while the final German Manufacturing PMI was even weaker at 40.6 vs. the 41.7 flash estimate. Yields moved higher with the US 10yr +1.8bps to 3.85%, fully reversing an initial dip lower on the ISM to 3.77%. The 2/10s curve inverted further to -108.5bps with US 2yr yields up 3.9bps to 4.94%. Market pricing for the Fed is little changed with around 21.3bps for July and a cumulative 34bps by November. Equity markets mostly rose, resilient to both the weaker data and higher yields. The S&P500 rose 0.1%, helped along by a 6.9% rise in Tesla after Q2 sales figures beat (466.1k vs. 445.9 expected). Oil traded lower (Brent -0.6%) despite moves by Saudi to extend production cuts and Russia to reduce exports. FX moves were not large with the USD (DXY) +0.1%, EUR +0.0%, GBP -0.1% and USD/Yen +0.3%. The NZD rose 0.4% and the AUD is up 0.1% to 0.6672, with all focus on today’s RBA decision which is seen as a genuine 50/50 (more on that below).

First to the US ISM Manufacturing. The headline index was weak at 46.0 vs 47.1 expected and 46.9 previously. All key components are now in contractionary territory and highlight the defacto recession being seen in the manufacturing sector. Production fell to 46.7 from 51.1, New Orders were 45.6 from 42.6, Employment was 48.1 from 51.4, and Prices Paid was 41.8 from 44.2 previously. In many respects this is not new news given manufacturing has been below 50 for some time, with little sustained market reaction after today’s numbers. Instead, markets are likely to be more sensitive to Thursday’s ISM Services Index. For your scribe, the most interesting aspect was the anecdotes. One firm noted “ Orders and business are steady with a healthy backlog, but new prospective orders seem to be getting pushed back into 2024” and another said “North American demand stabilizing, but European markets showing slowing in the second half of 2023 and 2024” (see June 2023 Manufacturing ISM® Report On Business® for details).

Speaking about Europe, the final-Manufacturing PMIs were revised lower with the wider Eurozone measure at 43.4 from 43.6. Of some concern was the German Manufacturing PMI which was revised lower to 40.6 from 41.0. S&P Global who compile the PMIs noted that the “worsening performance stemmed from a sustained deterioration in new orders across the sector. Firms commented on a range of factors behind the decline, including customer hesitancy and destocking. survey pointed to weaker sales both domestically and abroad”. Interestingly firms had only “ just started to cut their selling prices in June…while input prices have already been falling for several months. The most important reason for this certain serenity observed among companies is likely to be the order backlog, which, although declining, is still significantly higher than the historical average…” (see HCOB Germany Manufacturing PMI for details).

Elsewhere, in oil markets, Saudi Arabia said that it would extend its 1m barrels a day cut in production by a month, through August and it could extend it further. Russia added that it would reduce oil exports by 500,000 barrels per day in August and aim to reduce production by this amount. The announcements only had a temporary positive impact on oil prices before falling back. Brent crude is currently down less than 1% for the day and back below USD75 per barrel, suggesting little concern by traders, with the market seemingly well supplied compared to sluggish demand. In FX, the Chinese yuan has strengthened a little (USD/CNH -0.2%) bouncing off of 2023 lows reached on Friday, after the central bank set a higher than expected fix by 310pips, thus confirming its displeasure with the recent depreciation. It is also worth noting that the PBOC said in its quarterly monetary policy committee meeting on Friday that it will adopt “comprehensive measures and stabilize expectations” about the yuan. Also out yesterday was the Caixin Manufacturing PMI which was 50.5 vs. 50.0 expected and 50.9 previously.

Finally in Australia, there was a lot of housing market data yesterday which was consistent with the stabilisation seen in the housing market most recently , though expectations of further rate rises will hamper borrowing capacity and is likely to challenge the sustainability of the recent rebound. Housing loan commitments rose 4.8% m/m in May (consensus +1.4%), coming after -1.0% in April and +4.7% in March. Dwelling approvals meanwhile surged in May, up 20.6% m/m (consensus 3.0%). The large rise was the result of a 59.4% m/m gain in the volatile attached dwelling approvals category, led by a spike in NSW apartment approvals. Detached approvals did not rise sharply, up only 0.9% m/m. The overall outlook for dwelling construction though is still weighed down by uncertainty and availability of material and labour

Coming up:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.