Online retail sales growth slowed in May following a fairly strong April

Insight

It was a quiet night for markets devoid of any top-tier data or news flow ahead of key risk events next week (of US CPI, FOMC, ECB).

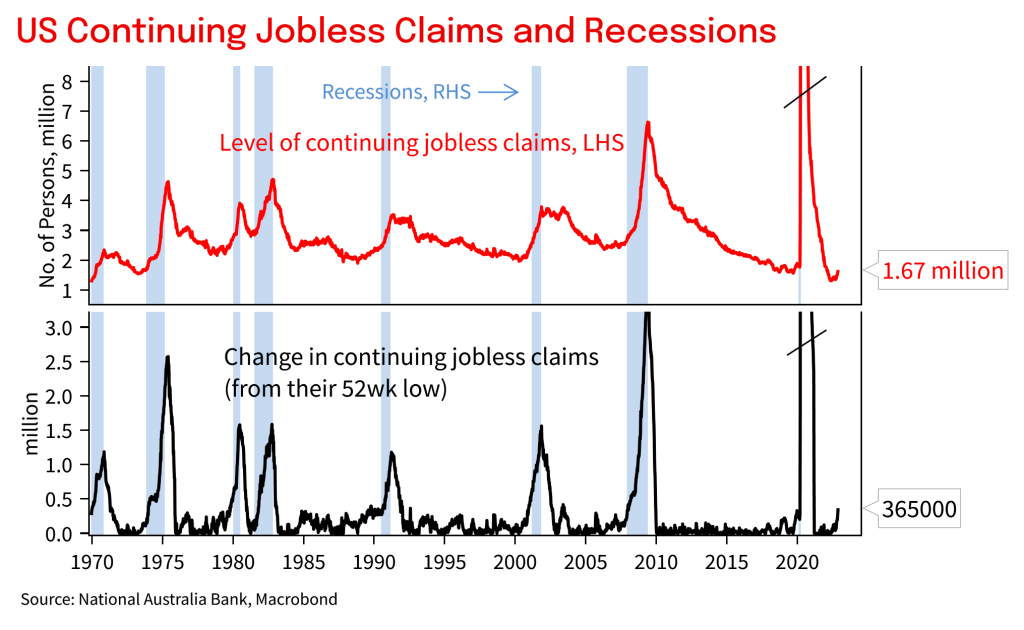

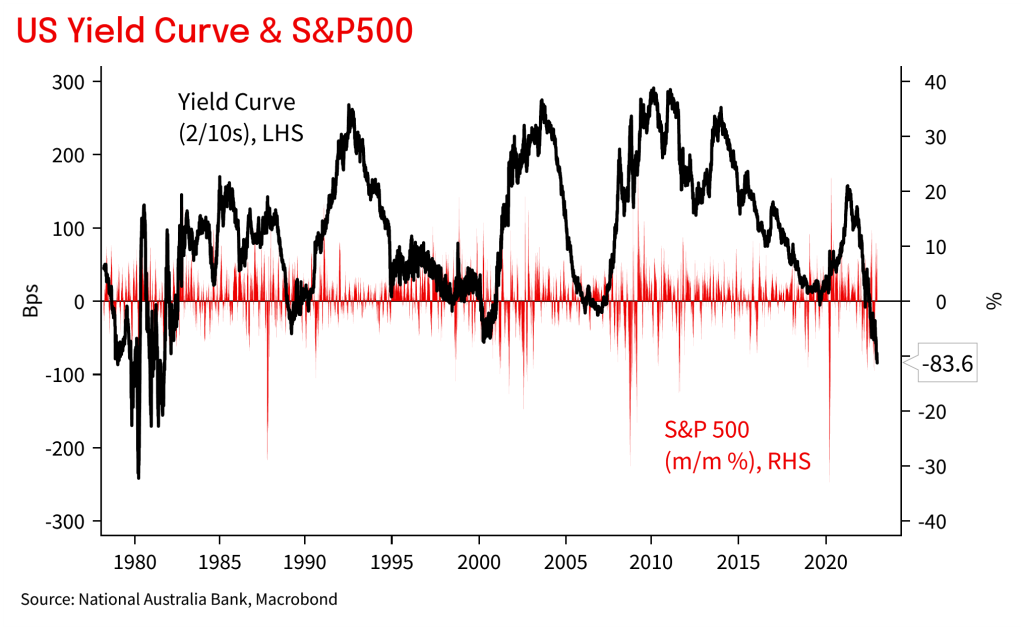

It was a quiet night for markets devoid of any top-tier data or news flow ahead of key risk events next week (of US CPI, FOMC, ECB). Consolidation was the theme ahead of those risk events with the S&P500 +0.5% into the last hour of power, after having fallen by -3.6% since the start of December. Global yields have rebounded, though moves haven’t been large in the context of recent volatility. The US 10yr is up 7.2bps to 3.49% and the 2yr is up around 5.9bps to 4.32%. The 2s/10s curve remains the most inverted since the early 1980s at around -83bps and continues to point towards a US recession in 2023. Also supportive of that recession narrative was US Continuing Jobless Claims last night, and although at still low levels, they are now 27% off their 52-week low (see macro chart of the day below). Looking to next week’s FOMC meeting, a 50bps hike is fully priced, while the peak in the fed funds rate sits around 4.94% and there are 46bps worth of cuts priced in H2 2023.

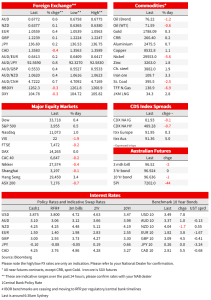

As for FX moves, the USD was broadly weaker with the DXY -0.2%. Positive news around China’s covid strategy and further support for the property sector saw commodity currencies leading the way with the AUD +0.5% and USD/CAD -0.3%. Reflective of the China narrative copper rose 1.1% to its highest close since June, and iron ore futures were +3.3% to be near a four-month high following their largest ever monthly gain. The oil price meanwhile was very volatile amid an outage of the Keystone oil pipeline which carries oil from Canada into the US – WTI had spiked as much as 4.8% before reversing to be little changed at $71.49 with many viewing the outage as temporary. As for the other majors currency pairs: EUR +0.3%, GBP +0.2% and USD/JPY 0.2%. The move in the EUR is notable at 1.0553, now near its highest level in six months.

Data was very second tier overnight. US Jobless Claims continued to trend slightly higher, though was as expected at 230k from 225k, and is consistent with the levels seen in 2019 prior to the pandemic. More interesting for your scribe was Continuing Jobless Claims which were 1,671k from 1,608k and are now 27% above their recent lows. This suggests that despite the very tight labour market, people who are being laid off are staying on unemployment benefits longer and are finding it harder to get re-employed. Given the rise in announced layoffs, jobless claims are likely to continue to rise. Meanwhile the rise in continuing claims from their low earlier in the year is already consistent with elevated recession risk (see chart below).

There were also some interesting anecdotes doing the rounds, hinting of hefty price falls on the goods side of the US economy. Adobe reported prices for computers and electronics solid online fell sharply in November with computer prices down -18% y/y. The Manheim Used Care Value Index meanwhile also continued to fall to be -14.2% y/y and the lowest in level terms since August 2021 (see Manheim for details). These anecdotes suggest we should expect a sharp reversal of price pressures on the goods side of the economy as hinted at in the most recent ISM Manufacturing, but the extent to which this is reflected on the services side of the economy remains less clear given the still tight labour market.

Finally in terms of China news, it was positive from a market viewpoint. Bloomberg reported that China is set to announce further measures to support the property sector next week as the government refocuses on the economy. The authorities are expected to announce a 5% GDP growth target for next year which many analysts are sceptical can be achieved if the property sector remains under severe pressure. Industrial commodities are higher overnight amidst hopes for a rebound in the property sector and iron ore and copper rose as noted above. As for the shift on the covid policy, one example of a further shift was in Hong Kong where officials cut the isolation times for infected people to five days from seven. While the transition to living with covid is unlikely to be smooth, international experience suggests if widespread transmission is occurring then within 3 months the re-opening wave would have passed. China will look different by March/April and markets are likely to downplay any weak data prints before then.

US: PPI & Uni Mich. Consumer Sentiment: The PPI will be closely watched for further signs of moderation in inflation pressures as seen last month. Most focus will be on the ex-food, energy and trade services, and consensus is for 0.1% m/m and 4.7% y/y. The PPI along with the CPI on Tuesday will help shaped the Fed’s view of inflation pressures ahead of the FOMC meeting on Wednesday.

Chart 1 – Macro chart of the day: rise in continuing jobless claims off the recent lows is consistent with elevated recession risk

Chart 2 – Markets chart of the day: yield curve remains the most inverted since the early 1980s. Inverted curves historically have pressured risk assets even when they have started to re-steepen.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.