We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

It has been a volatile session in markets with risk assets initially lifted by rumours China was looking at phasing out its zero-covid policy, only for Beijing to later deny the speculation.

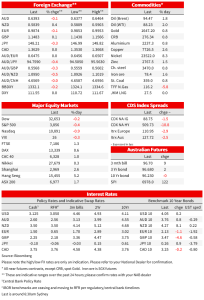

NZ: Building permits (m/m%), Sep: 3.8 vs -1.6 prev.

CH: Caixin PMI manufacturing, Oct: 49.2 vs. 48.5 exp.

AU: RBA cash rate target (%), Nov: 2.85 vs. 2.85 exp.

US: JOLTS job openings (m), Sep: 10.72 vs. 9.75 exp.

US: ISM manufacturing, Oct: 50.2 vs. 50.0 exp.

It has been a volatile session in markets with risk assets initially lifted by rumours China was looking at phasing out its zero-covid policy, only for Beijing to later deny the speculation. Sentiment was then dented further on good US economic news being bad news, likely forcing the Fed to remain hawkish. After opening higher, US equities end the day marginally in the red. Gilts outperformed ahead of the BoE meeting on Thursday while the UST curve twist flattened with the 2y tenor climbing another 5bs to 4.54%. 10y UST yields end the day close to their highs at 4.06%, after trading down to an overnight low of 3.92%. After a volatile session, FX ended the day little changed. USD regained mojo vs euro and GBP while the AUD starts the new day just below 0.64.

Chinese stocks led a rally during our day yesterday after traders latched onto unconfirmed media posts that China had formed a “Reopening Committee” looking at different reopening scenarios, targeting March next year. The rumours triggered a rally in Chinese and Hong Kong equities spreading to US equity futures, weaking the USD and boosting commodity linked currencies. Later in the session, Beijing spoiled the party with China Foreign Ministry spokesman Zhao Lijian saying he was “not aware” of any such committee. More credible media reports also pour cold water on the speculation noting that the country has actually ramped up its lockdowns after the Party Congress ended due to rising Covid cases.

Sentiment was further dented later in the session following better US economic news. As it has been the case recently, the market has been looking for bad US economic news as a signal the Fed may ease up on its hawkish intentions. Well last night, it was the opposite with a decent bounce in the JOTS report alongside a better-than-expected ISM report suggesting the US economic is not yet showing signs cooling materially.

The ISM Manufacturing fell for a fourth time in the last five months, contracting by 0.7 to 50.2, beating expectations for a decline towards 50 , while many were calling for contraction levels (sub fifty) given the recent decline in the regional surveys. Orders contracted for the fourth time in five months, while the sub-index of prices paid fell to a more than two-year low (46.6 from 51.7). Meanwhile, the employment sub-index edged up to the breakeven reading of 50 after shrinking in September, suggesting manufacturers are either limiting hiring, having trouble finding skilled labour or a combination of the two. Comments in the survey also pointed to lessening price pressures and easing supply-chain pressures

The number of job openings (JOLTS) rose to 10,717K in September from 10,280K in August, above the consensus, 9,750K. The openings rate rose to 6.5% from 6.3% (was 6.2%) and the latest data suggests there are 1.9 job openings for each unemployed job seeker. The report is a frustrating outcome for the Fed, which had been hoping the increase in the funds rate so far would take some pressure off the labor market and wages. The lack of softening in the JOLTS report alongside a still resilient ISM manufacturing, suggest the Fed still has a fair bit work to do in order to bring inflation to heal.

Ahead of the report 10y UST yields were heading south, trading to an overnight low of 3.92%, but then the data releases jolted the market with the 10y tenor ending the day at 4.05%. The curve twist flattened with the 2y rate ending the day 5bps higher at 4.54%. Earlier in the session UK Gilts outperformed led by the short-end as money markets pare back BoE rate hike ahead of Thursday’s MPC outcome.

Sticking with the UK, the BoE kicked off it quantitative tightening programme, successfully selling £750m gilts back to the market, a remarkable achievement after last month’s turmoil in the market which saw it needing to buy gilts during a period of turmoil. The Bank is looking to actively sell about £40b of gilts back to the market over the next year.

After opening sharply higher, reflecting the China rumour gains in the futures, US equities ended the day marginally lower with the S&P 500 down ~0.40% while the NASDAQ was -0.89%. Good US economic news spooking investors as the resilience of the economy is likely to keep the pressure on a hawkish Fed.

The USD has ended the day slightly higher, but a look at intraday chart shows a reversal of an initial steady decline with initial gains by the euro and GBP reversed later in the session. The US economy while slowing is still performing better than other majors and the Fed so far has remain more hawkish than other central banks. After trading to a high of 0.9953, the euro now trades at 0.9876. Similarly, the pound climbed to 1.1566 earlier in the session, but now trades at 1.1481.

Yesterday the AUD enjoyed a steady rise before and after the RBA meeting, reaching on overnight high of 0.6464. Then all these gains were quickly reversed after the better-than-expected US data releases. The AUD starts the new day at 0.6394, little changed over the past 24 hours. The NZD fared a little bit better, temporarily breaking up through 0.59, but has settled back down to 0.5845, still up about 0.5% from this time yesterday

The RBA raised interest rates by a quarter-percentage point to 2.85% as widely expected and signalled further tightening to come as it combats escalating inflation, with future moves to depend on data, as always. The statement also noted the Board is closely monitoring the global economy, household spending and wage and price-setting behavior”.

The central bank also lowered its outlook for economic growth in response to higher rates and now expects inflation to peak at around 8% later this year, slightly up from a previous expectation of 7.75%. On Friday we will get the full new set of RBA forecasts and if the new forecast show inflation is expected to remain elevated for an extended period of time (beyond 2024), then the RBA will be forced to keep the cash rate at an elevated (restricted) level for a long time. Speaking last night, Governor Lowe said that the risks are more two-sided than they were a few months ago, and the bank needs to factor in the risk of the lag. In contrast to the Fed, the RBA has now seemingly shifted towards a more gradualist approach.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.