NAB specialists and clients from across the bank’s Fund Sponsors, Strategic Investors and Alternative Assets (FSA) business gathered over lunch recently to share career stories and advice on promoting greater diversity and inclusion.

Oil prices have fallen to their lowest since early February 2022 with falls of around 4% in part due to weaker China demand.

https://soundcloud.com/user-291029717/slow-boat-from-china?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

There’s a global economic slowdown in train as evidenced by yesterday’s much weaker than expected China July activity data, which should be bad news for US stocks given the dependence of S&P500 companies on foreign demand for about 30% of their revenue. You would ordinarily have also expected a bite to have been taken out of risk assets from some shockingly weak US economic numbers, care of the NAHB Home Builders Sentiment index and Empire (NY) State Manufacturing survey.

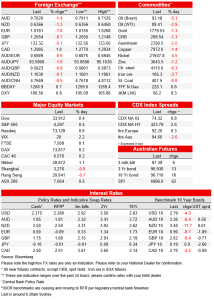

Not so, Wall Street having just closed with the S&500 up 0.4% and the NASDAQ a slightly bigger 0.6%. Lower oil prices might be one factor – notwithstanding a 2% fall in the Energy sub-sector – portending as they might further falls in headline inflation. Lower bond yields are another, for the tech. sector in particular and which has led Monday’s gains, with Treasury yields 3-4bps lower across the curve. The AUD (and NZD) have both fallen victim to the China news, in conjunction with a fall of more than 1% in the offshore RMB, USD/CNH now trading above 6.80 from around 6.74 prior to yesterday’s surprise 10bps cut to the Medium Term Loan Financing (MLF) rate.

Monday morning didn’t start as Friday left off. Hot on the heels of some very much weaker than expected China July credit data published after our market went home on Friday but which was ignored in offshore markets, the PBoC unexpectedly cut its 1yr MLF rate by 10bps to 2.75% , a move which should portend a cut to both one and five year Loan Prime Rates at Friday’s rate set. Depending on the extent to which the 5-year rate is cut relative to the 1-year rate, the former more relevant to mortgage rates, the latter to corporate borrowing rates, this will offer clues as to the precise motives for this unexpected move. The answer may be ‘both’ in which respect validation or the cut also came from the much weaker than expected July activity data published shortly after the MLF announcement.

The May and June post-zero covid lockdown-related bounce back in China activity has been quickly rendered a thing of the past. Retail Sales fell to 2.7% y/y from 3.1% against a riser to 4.9% expected, Industrial Production growth slipped to 3.8% from 3.0% against 4.3% expected and Fixed Asset Investment in YTD y/y terms to 5.7% down from 6.1% and 6.2% expected. Remember these are nominal numbers so the latter in particular is heavily inflated by price effects.

Immediate impact of first the MLF news then the softer than expected activity readings was to push USD/CNH up from 6.74 to first 6.75, then to above 6.77 post the data. These gains have extended to as high as 6.82 overnight, a rise of more than 1% on the day. Given the historical sensitivity of AUD and NZD to volatility in the RMB, albeit not all the time, the move up in USD/CNH did a more than adequate job in explaining the fall from grace in both AUD and NZD yesterday, in the case of AUD/USD from 0.7120 to an overnight low of 0.7011.

Economic news out of the US overnight has been quite shocking, in particular the plunge in the Empire (New York state) Manufacturing Survey , to -31.3 from 11.1 and against an expected expected drop to 5. This is by far the lowest read since the early months of the pandemic (the seis low was -78.2 in April 2020) and is driven by weakness in New Orders and Shipments. Analysts note though this is a relatively small survey and tends not to map well to the nationwide ISM manufacturing index, meaning we shouldn’t read too much into it, pending the signal from other regional PMI surveys in coming days. Also of note though was an 8.8pts fall in Price Paid, which most likely reflects lower oil prices which, if maintained, should flow through to further falls in headline CPI inafltion rates (see more on oil below)

Perhaps of greater significance, the NAHB (Homebuilders) sentiment index fell a much bigger than expected 6 points to 49, against an expected fall of just one point to 54. The reading is the weakest since the initial covid hit, with the industry spokesman talking explicitly of a recession in the sector, citing weakness in present sales, expected sales, and buyer traffic. This can all be blamed on the 30% fall in mortgage demand off its peak. Whether the recent modest fall back in mortgage rates can do anything to support the sector remains to be seen, but likely not. Tonight’s Housing Starts numbers will now attract more than usual interest (see Coming Up).

Oil prices have fallen to their lowest since early February 2022 ,with falls of around 4%. Weaker China demand or expectations thereof must be part of the story, but there are also hopes that the weekend concession by the EU in an effort to break a deadlock in talks over an Iran nuclear accord, related to the current U.N. investigation into the Islamic Republic’s past atomic activities, could see an early breakthrough. Our commodities experts are sceptical, noting that in reality this is a U.S., not EU deal to do and that a deal with Iran would likely not be popular with US voters and so is hard to envisage before the November mid-terms. Markets are currently prone to optimism though and hopes for a deal – which if it transpired could bring perhaps a million barrels per day of additional Iranian oil on to the market, have added to downward pressure on oil prices. This in turn engenders hopes for more petrol price driven softness in headline inflation rates in the US and elsewhere (and which could eventually feed through to core inflation rates).

Finally in FX, the sharp fall back in risk sensitive/pro-growth currencies overnight, encompassing AUD, NZD, NOK and SEK (all off by between 1.3% and 1.5% versus Friday’s new York close) undermines of a lot of the technical positivity generated from the prior run-ups, albeit for now AUD/USD is (just) holding on to the 0.70 handle it first recaptured back on 27 July (overnight low of 0.7011). NAB’s FX Strategy team continues to expect a deeper pull back in coming weeks in conjunction with the USD recovering some poise, in which respect the DXY index has just finished Monday 0.83% stronger.

NAB specialists and clients from across the bank’s Fund Sponsors, Strategic Investors and Alternative Assets (FSA) business gathered over lunch recently to share career stories and advice on promoting greater diversity and inclusion.

Hybrid issuance is becoming an ever more relevant funding instrument and capital management tool for corporate issuers today, attracting strong investor demand, write Tabitha Chang and Stefan Visser from the NAB Capital Markets Origination team.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.