Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

The Fed will push on with ending its lower capital requirements held against Treasurys, sticking with a schedule that will see the so-called supplementary-leverage ratio (SLR) ending on 31st March.

https://soundcloud.com/user-291029717/slr-and-all-that?in=user-291029717/sets/the-morning-call

Cold turkey has got me on the run – John Lennon

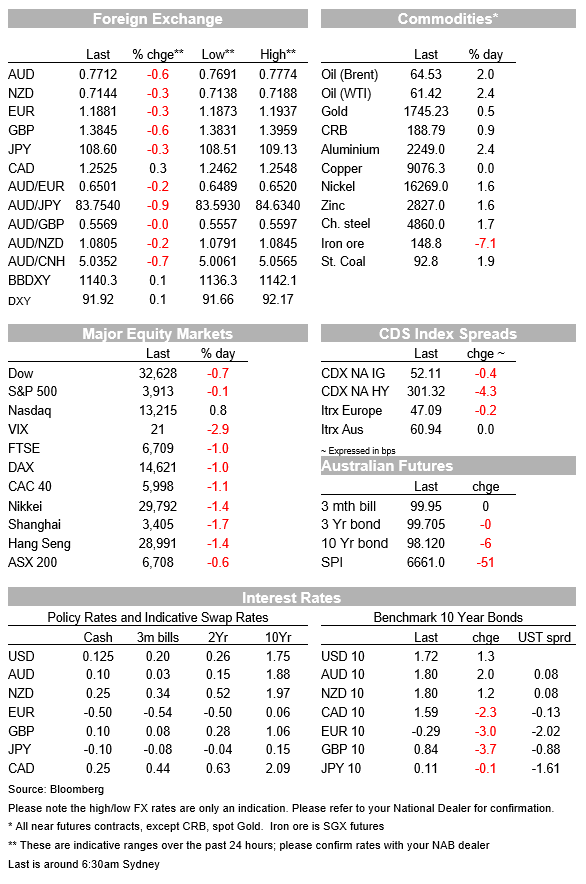

After a soft lead from Europe, US equities opened Friday’s session on the backfoot followed by a tame recovery before the close. The Fed decision to let its Supplementary Leverage Ratio (SLR) exemption expire, as scheduled, rattled the UST market, but the move faded before the close. Bank shares were also affected by the announcement weighing on the Dow and the S&P while investors expressed a preference for IT. The USD closed the day and the week marginally stronger; GBP was Friday’s underperformer while NOK was the week’s laggard. News that Turkey’s president Erdogan fired the country’s Central Bank Governor sees EM FX start the new week under pressure with AUD and NZD on the back foot at 0.7715 and 0.7146 respectively.

Volatility in the US Treasury market was one of the main themes on Friday with the Fed decision to let the SLR exemption expire the trigger. SLR exemption was introduced last year by the Fed in order to help improve liquidity in the financial system. The exemption effectively meant that Banks could exclude UST and central bank deposits when measuring the size of their balance sheets used to estimate the minimum level of capital they are required to hold (for the biggest US banks, capital must be equal to at least 5% of total assets). The lapsing of the exemption does take away an incentive for banks to hold UST, and this of course is happening in environment of increasing UST supply, so the concerns is that the decision will exacerbate the current elevated level of volatility in the UST market.

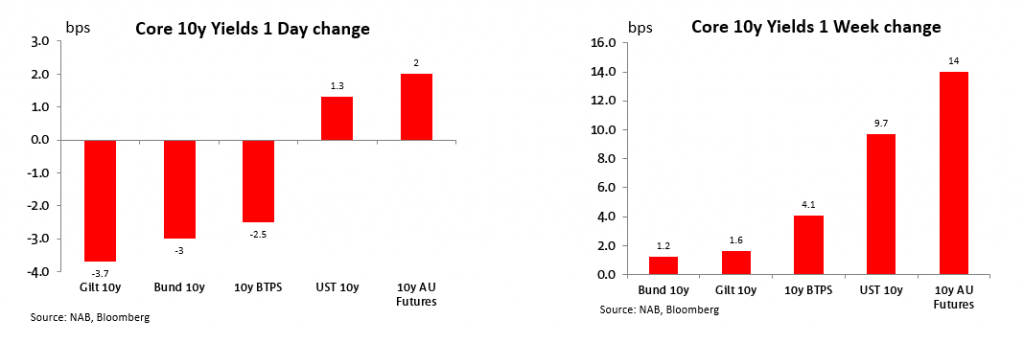

News of the Fed decision triggered a jump in UST yields with the 5 year Note rising 5bps to 0.8996% on the news while the 10y Note climbed from 1.6803% to an overnight high of 1.748% before it pared gains to settle at 1.721%, about 1bps higher on the day.

Fed Chair Powell released a WSJ op-ed, reiterating a number of messages from the Fed statement. The dovish punchline was “but the recovery is far from complete, so at the Fed we will continue to provide the economy with the support that it needs for as long as it takes” but there wasn’t much market reaction.

UST volatility has remained elevated with the Move index ending the week at 68.8, well above the low 40’s level seen over November last year to February this year. Looking at the week, there was an increase in UST curvature with the 10y note climbing 9.7 bps while the 5y gained 4bps (to 0.88%) and the 30y Bond was up by 5.6bps to 2.43%, after briefly trading above the 2.50% mark during the week.

EU core yields were little changed on the week (marginally higher) while 10y AU bond futures underperformed, climbing 14bps to 1.84% in yield terms (98.120 in price terms).

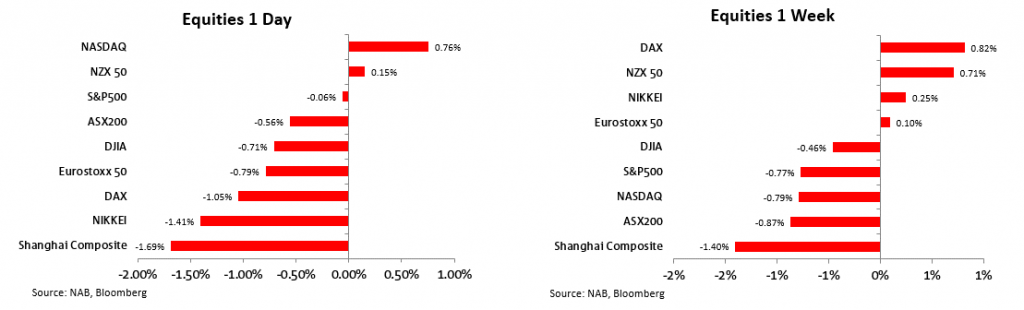

European equities ended the week on a downbeat tone with the Stoxx Europe 600 Index falling 0.8%, erasing its weekly gains along the way. Banks were the worst performing sector on Friday, dropping 2.3%, utilities was the only sector that managed to stay on the green.

Meanwhile US equities ended the day mixed, although they did stage a recovery after the negative lead form Europe and the Fed decision to not extend the SLR rule. US banks were the big underperformers on the day weighing on the Dow (-0.71%) and the S&P 500 (-0.06% with Financials down 1.95%). A preference for high tech helped the NASDAQ close the day in positive territory, although on the week all US equity indices lost ground with the DAX and NZX the outperformers.

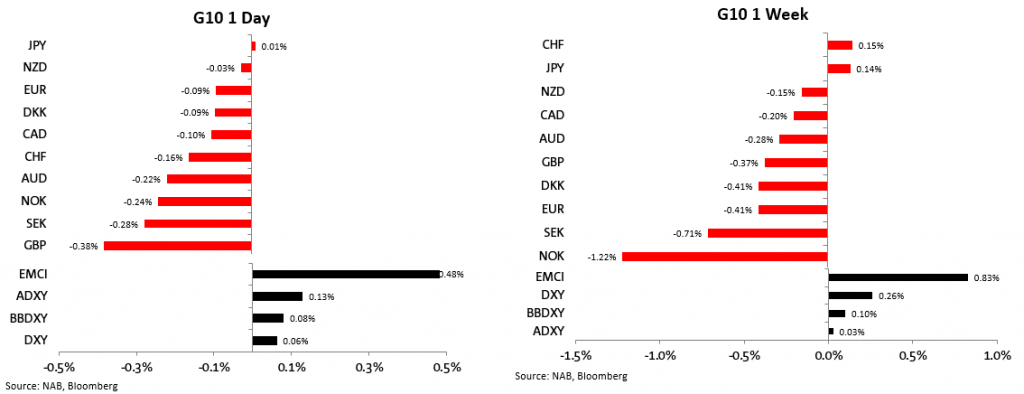

The USD was moderately but broadly stronger on Friday, helped by the move in UST yields and a tinged of risk aversion in the air. GBP was the notable underperformer, down 0.38% on the day, closing week at 1.3861. There had been some news on vaccine supply concern that might have weighed on the pound, but relative to other countries the UK continues to be an example of how to efficiently implement a vaccine roll out, on Saturday the UK hit a new record high of daily vaccines, a total of 844,285 combined first and second doses were given on Saturday, up from 711,157 on Friday.

The euro was little changed on Friday, showing little impact to the news that many European countries are considering tighter lockdown restrictions, amidst a renewed pick-up in Covid-19 cases in the region. Germany’s Chancellor Merkel said it was likely the country would need to apply the “emergency brake”, re-imposing tighter lockdown rules, rather than easing restrictions in April as previously planned. Italy imposed a tighter lockdown last weekend while Paris entered a month-long lockdown on Friday night. The stuttering vaccine rollout in Europe means it will be slower to exit lockdown conditions and its economic recovery will lag countries like the UK and US, which are more advanced in vaccine distribution.

Looking at the week the NOK was the big underperformer, no doubt feeling the weight on the big decline in oil prices, down over 6% on the week, after recovering 2% on Friday. The euro lost 0,41% while the AUD and NZD were relatively steady and still contained within recent ranges. AUD closed the week at 0.7741while NZD ended at .07166.

That said, after Friday’s close Turkey’s President Erdogan fired Turkey’s central bank Governor just three months into his four-year term and days after he raised interest rates by more than expected. Erdogan’s decision to fire Governor Agbal, who had sought to instil some price stability and perception of Bank independence, now raises question as to whether the new Governor will look to lower rates while still aim to fight higher inflation.

EM FX has opened the new week under pressure (TRY down 15% to 8.25 and ZAR -1.15%) with both antipodean currencies felling some of the repercussions, AUD now trades about 30bps lower at 0.7714 while NZD is at 0.7146. USD/JPY is also down about 35 pips to 108.578 and the market will be on alert for any gap lower in USD/JPY as Japanese retail investor look to re asses the outlook for TRY and potential short covering of positions.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

Uncertainty remains high ahead of July reciprocal tariffs

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.