On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

US September payrolls were a big miss, but strong revisions to prior months alongside a decline in the unemployment rate and lift in hourly earnings resulted in a relative subdued reaction by markets, suggesting the figures were strong enough to keep the Fed on track to begin its QE tapering programme in November.

US September payrolls were a big miss, but strong revisions to prior months alongside a decline in the unemployment rate and lift in hourly earnings resulted in a relative subdued reaction by markets, suggesting the figures were strong enough to keep the Fed on track to begin its QE tapering programme in November. UST yields ended the day higher with a rise in oil prices and upcoming supply likely contributing to the move, the USD was little changed on Friday, but a solid week for commodities helped CAD,NOK and AUD outperform on the week.

The September US labour market report was a mixed bag. Payrolls missed at 194k vs 500k expected, but solid revision added a net 371k jobs, the unemployment rate fell to 4.8% from 5.2%, below the 5.1 expected while Average hourly earnings rose 0.6%, lifting the yoy number to 4.6%. Looking at the details, the headline payroll number was depressed by a 123K drop in government employment, all in the education sector with seasonals playing a hindering role. After a sharp drop slowdown in August, leisure and hospitality only added 74k jobs in September, but with the delta covid waving fading, expectations are for significant increase in jobs from these two sectors in October given the continued decline in Delta cases and rising activity in the restaurant, airline, and hotel sectors. The end to generous unemployment benefits and the return to schools in the US, the effects of which were unlikely to have been fully captured in this payrolls report, should also encourage labour force participation and bolster job growth going forward.

Notwithstanding the soft payrolls headline, the inner strength in the report suggests the numbers have past the Fed’s test for a “reasonable enough” report to allow for a QE tapering announcement in November. That said, the report also leaves a lot of questions unanswered, at 61.6% the US labour participation remains low relative to pre pandemic levels of around 63%, posing question over workers reluctance to re-join the workforce, given risk of infection. Uncertainties of school, infection on kids are also a potential factor while a post pandemic skill mismatch is also a consideration.

Reaction to the US labour markets figures triggered an initial decline in UST yields and the USD, but these moves were swiftly reversed as market participants concluded the report was unlike to change the Fed’s tapering intentions.

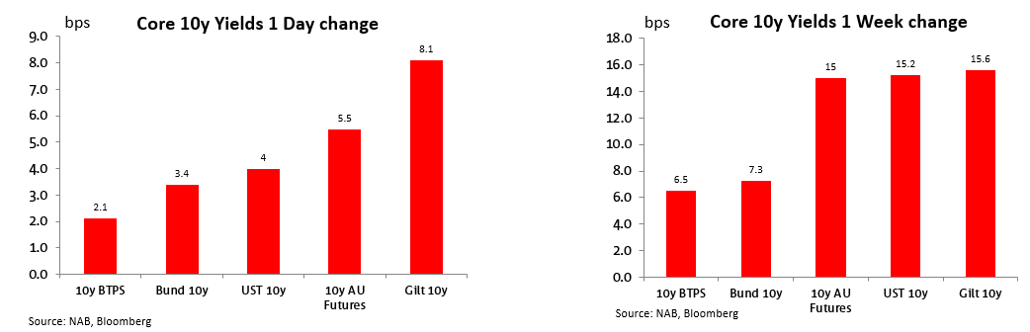

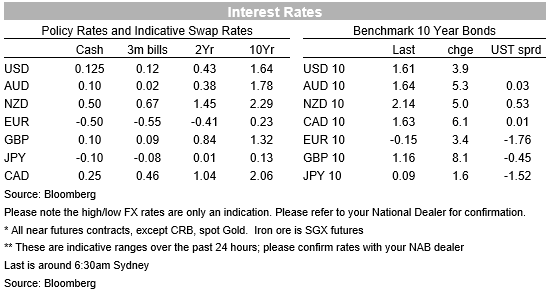

10y UST yields fell to a session low of 1.558% shortly after the jobs data and then it was onwards and upwards with the benchmark yield closing the week at 1.6118% while the 5-year US rate closed at an 18-month high, at 1.06%. The move up in UST yields was largely driven by a rise in inflation expectations with the 10y breakeven gaining 4bps on the day to 2.51%. The latter pointing to the UST market sensitivity to a rise in oil prices with WTI crude oil futures hitting $80 per barrel for the first time since 2014. Oil prices remain supported by strong demand, restrained supply from OPEC+ as well as demand from some energy consumers who can use oil an alternative to natural gas. The market may have also had in mind the new UST supply coming this week with a $58bn 3-year note and $38bn 10-year note auctions both scheduled for Tuesday and $24bn 30s on Wednesday.

The move up in yields was not just confined to the US market, In the UK, the 10yr rate hit its highest level in more than 2 years, up 8bps to 1.16%, while Germany’s 10-year rate is nearing its own 2½-year high (within 10bps), closing at -0.15%. The European bond market ignored a third consecutive daily fall in natural gas prices, which were off by almost 20% in the UK and Europe on Friday, with both benchmarks now almost 50% off the panic-driven highs from the middle of the week.

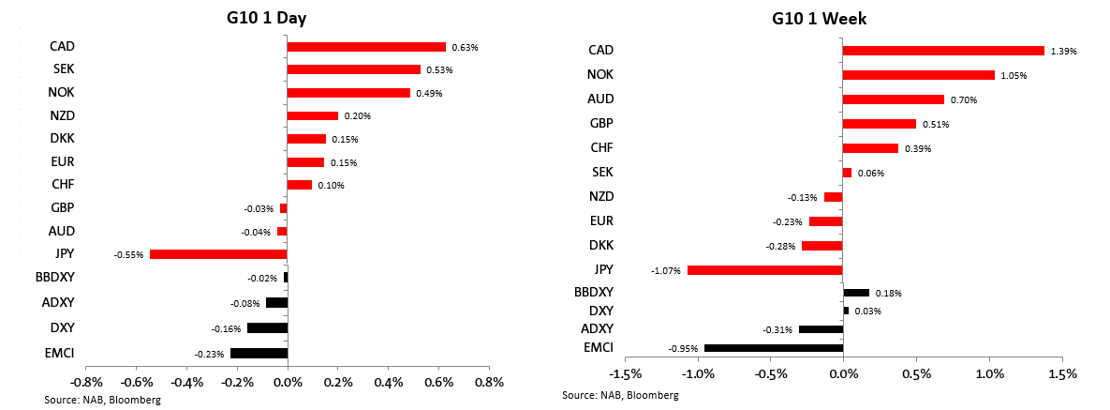

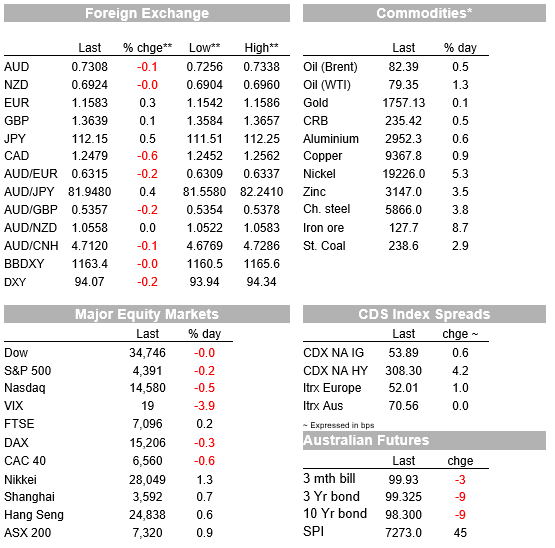

Moving onto the FX markets, after a down and then up move post the payrolls report, the greenback ended the day little changed with JPY weakness ( -0.55%) offset by gains commodity linked currencies and small European pairs, reflecting a pro-growth bias, although of note the AUD was a bystander, unchanged on the day, ending the week at 0.7309. USDJPY closed the week above ¥112, following the move up in 10y UST yields while CAD was the top performer, up 0.63% helped by a solid labour market report. Canada’s seasonally adjusted unemployment rate fell by 0.2% to 6.9% in September, aided by a gain of 157.1k jobs vs 65k expected.

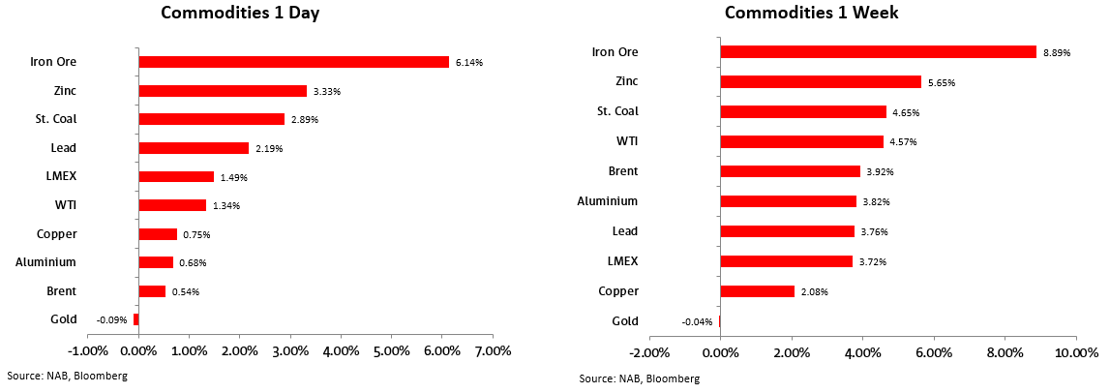

On the week the CAD (+1.39%), NOK (+1.05%) and AUD (0.70%) were the top G10 performers. The AUD starts the new week at 0.7308 and still remains unable to make a sustain break above 0.7315. Iron ore recovery, up over 6% on Friday along with gains in energy prices are helpful commodity tailwinds while today NSW embarks on the first stage of reopening, good news for the economy.

Meanwhile the NZD closed Friday at around 0.6930, little changed on the week and unable to get any support from the RBNZ decision to lift the cash rate by 0.25bps to 0.5%. NZ Covid-19 cases continue to trend higher, with 60 cases reported yesterday and the seven-day average of new daily cases up to 37, both their highest levels since early September. Moreover, cases are now popping up in other areas of the North Island, with Northland put into an alert level 3 lockdown on Friday night and a case discovered in the Bay of Plenty over the weekend. The NZ government will announce today if it has decided to tweak more concessions into Auckland’s broader level 3 status.

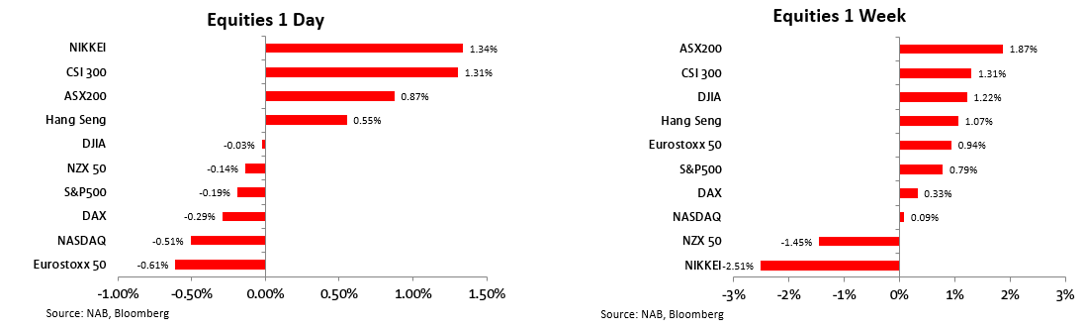

After two solid days of gains, US equities ended Friday a little bit softer, the S&P 500 was down by 0.1% and Nasdaq was lower by 0.4%. Energy and financials stocks closed higher while healthcare and materials sectors were the big underperformers.

Looking at the week our S&P/ASX200 was the top performer, up 1.83% with China CSI 300

up 1.31%. US and European equities recorded modest gains for the week while the Nikkei was the big underperformer, down 2.51%.

Commodities had a good week with iron ore gaining over 6% on Friday, close to 9% on the week (Singapore futrues closing at $ 124.65). Metals and energy also did well up close to 3% n the week with copper (2%) not too far behind while gold was unchanged.

The FT reports the EU has rejected the UK’s demands for a rewrite of the Brexit Northern Ireland protocol. The Guardian also notes that the UK is set to reject the EU proposal due to be unveil on Wednesday on the basis that it doesn’t go far enough. Key demands include an end to the EU imposition of inter-UK goods trade as well as the removal of the European Commission oversight protocol by the European Court of Justice (ECJ). Commentators have warned that the lack of concession on the ECJ would give the UK the justification to trigger article 16, placing the Northern Ireland protocol into a formal dispute process, implying the risk of the introduction of tariffs and quotas.

In other news, on Friday the OECD announced an agreement to implement a global minimum corporate tax , the breakthrough was achieved after some changes to the original text, namely that the rate of 15% will not be increased at a later date, and that small businesses will not be hit with the new rates. Ireland and Hungary, long time opponents to the proposal, came on board after the 15% tax level was agreed and reassurances were given that on a lengthy implementation period.

On Saturday Chinese President Xi Jinping reiterated his ambition to peacefully reunite with Taiwan , noting unification in a “peaceful manner” was “most in line with the overall interest of the Chinese nation, including Taiwan compatriots”. But he added: “No one should underestimate the Chinese people’s staunch determination, firm will, and strong ability to defend national sovereignty and territorial integrity.”. Taiwan’s President Tsai said a speech that her government will not bow down to pressure from Beijing and will continue to bolster the island’s defences in order to protect its democratic way of life . In a statement China noted Tsai’s speech incited confrontation and distorted facts, adding that seeking Taiwan independence closes the door to dialogue.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.