Our monthly transaction data suggest spending has been softer as the year progresses.

Insight

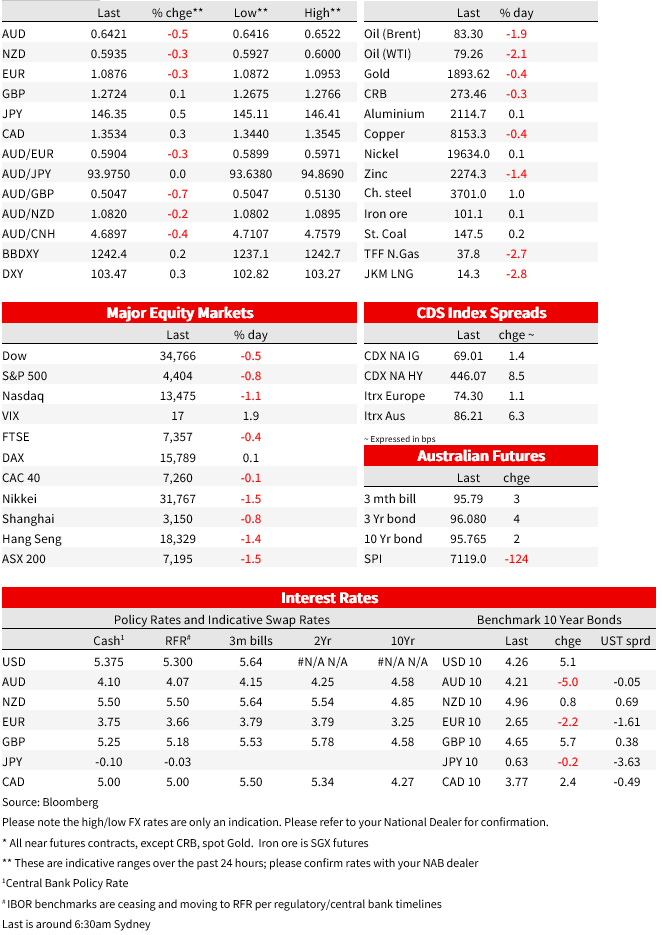

Todays podcast FOMC Minutes show concern about upside risks to inflation US yields higher led by 5bp rise in 10yr Equities were lower, S&P500 -0.8% with declines late in the session Asia equities weighed by China concerns AUD -0.5% against a broadly stronger dollar at 0.6421 Coming up: AU Employment, NZ PPI, JN Machinery Orders, […]

NZ: RBNZ official cash rate (%), Aug: 5.5 vs. 5.5 exp.

UK: CPI (y/y%), Jul: 6.8 vs. 6.7 exp.

UK: CPI core (y/y%), Jul: 6.9 vs. 6.8 exp.

EC: GDP (q/q%), Q2: 0.3 vs. 0.3 exp.

EC: Industrial production (m/m%), Jun: 0.5 vs. 0.0 exp.

US: Building permits (k), Jul: 1442 vs. 1468 exp.

US: Housing starts (k), Jul: 1452 vs. 1450 exp.

US: Industrial production (m/m%), Jul: 1.0 vs. 0.3 exp.

The FOMC minutes didn’t contain any big surprises, showing a FOMC that remains concerned about upside risks to inflation, but is watching the data. US yields were higher, led by a 5bp increase in the 10yr yields to 4.26%. That was the fifth straight session of gains and the highest end-of-day level since June 2008. US equities were lower, the declines largely late in the US session following the release of the Minutes. Elsewhere, UK inflation data was a touch above expectations showed uncomfortably strong services inflation, the RBNZ held rates unchanged at 5.5% as expected and US IP data was strong.

China concerns continue , with headlines grabbing attention including that some investment funds had been asked by officials this week to avoid being net sellers of equities, that Country Garden warned of ‘major uncertainties’ around bond redemption. News that Zhongrong International Trust, one of China’s biggest shadow banks, has not made payments on several investment products show risks facing the property sector are spreading to the financial industry. Investors looking for more aggressive support from policy makers amid soft activity have been disappointed as the recent incremental measures haven’t been sufficient to restore confidence. The Hang Seng lost 1.4%, while the CSI300 was 0.7% lower. The CNH was 0.2% lower against the USD. CNY neared, but held just below 7.3 yesterday, closing at 7.2985, not far from its 2022 peak of 7.3280.

The FOMC minutes for the July meeting showed most participants continue to see upside risks to inflation which could require further tightening of monetary policy, but that there was uncertainty about policy lags and some officials saw downside risks to growth despite resilience to date. Two official favoured holding rates steady in July, though the votes on the eventual decision were unanimous. The minutes also indicated that the data over coming months would help clarify the extent at which the disinflation process was continuing. There was little change to near-term pricing for the Fed funds track with 10bps of additional hikes priced over the next two meetings. US equities and the Treasuries were under pressure after the Minutes.

US 10yr yields were up 5bp to 4.26%, their highest end-of-day level in yields since June 2008. A broad story of resilience in activity to tighter monetary policy is challenging the case that the Fed will need to be retreating quickly towards accommodative settings any time soon even as recent inflation prints have supported expectations the Fed is at or near the top. US 2yr yields were 2bp higher to 4.97%. German 10yr yields fell 2bp to 2.65%.

The S&P500 was broadly flat going before the release of the minutes before declining to a loss of 0.8% over the day, closing around session lows. All sectors except for Utilities were in the red, with losses led by consumer discretionary, real estate and communication services. The Nasdaq underperformed down 1.1%.

In currency markets, the dollar was stronger, up 0.3% on the DXY. Gains came against all G10 currencies except the pound, with GBP +0.1%, supported by firm inflation data. The Australian dollar was down another 0.5% reaching an intraday low of 0.6416 late in the US afternoon and currently around 0.6421. The yen continued to grind lower. USDJPY was 0.5% higher to 146.35, move above 146 for the first times since early November.

UK annual inflation fell to 6.8% in July from 7.8% in June driven by lower gas and electricity prices. Core inflation was marginally higher than expected and was unchanged at 6.9% from the previous month. Notably, services inflation accelerated to 7.4% and will be a particular focus for the Bank of England (BOE). The market is pricing a further 79bps of tightening, an increase of ~25bp over this week following stronger than expected wages growth and the CPI data. UK gilt yields moved higher across the curve. 2-year gilt yields closed up 7bps at 5.18% while 10-year yields increased 6bps to 4.64%.

In the US, industrial production rose 1.0% m/m in July, well above consensus for 0.3%. Auto production was a support to the stronger monthly outcome. Ex autos, output increased a smaller 0.1% following 2 consecutive months of declines. Meanwhile housing starts and building permit data was close to consensus estimates. It is very early days and the GDPNow estimate should not yet be taken literally, but following strong retail sales and industrial production, the Atlanta Fed’s GDPNow model sits at 5.8% quarterly annualised growth!

The RBNZ left rates unchanged at 5.5% at the August Monetary Policy Statement . It was the second consecutive meeting the Official Cash Rate was left on hold and was unanimously expected by economists. The Monetary Policy Committee remains confident that with policy remaining at restrictive levels for some time, inflation will return to its 1-3% target band. In a modest hawkish tilt, the RBNZ increased its peak OCR to 5.59% in June 2024, up from 5.5% in the May MPS. However, in the accompanying press conference Governor Orr noted that the increase was model driven and there was not a signal for the next rate adjustment. NZD/USD gained immediately following the RBNZ monetary policy statement yesterday and extended up towards 0.5990 in offshore trade before fading back to 0.5950.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Our monthly transaction data suggest spending has been softer as the year progresses.

Insight

Business confidence down but costs, prices rise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.