Online retail sales growth slowed in May following a fairly strong April

Insight

The Fed has upped its growth expectations for the US economy, driven by the fiscal support and the vaccine rollout.

https://soundcloud.com/user-291029717/strong-market-reaction-as-fed-changes-nothing?in=user-291029717/sets/the-morning-call

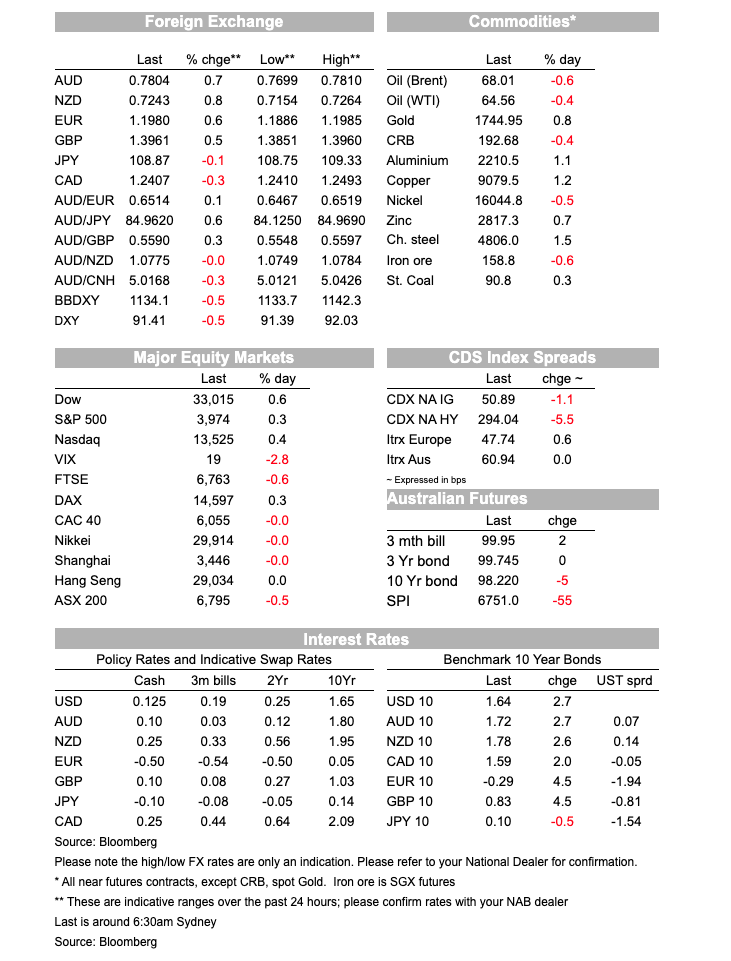

There was a distinct sense of market nervousness ahead of the FOMC meeting. Longer dated UST yields recorded new one-year highs, the USD enjoyed a safe-haven bid while tech shares led declines in equities. But a dovish FOMC has seen a reversal on these moves, the Fed upgraded its economic outlook and despite unemployment seen declining to 3.5% in 2023, the median dots project no hikes in 2022 and or 2023. US equities are now trading in the green, longer dated UST yields have pared some of their early gains and the USD has fallen by more than its pre FOMC gains.

As expected, the Fed left its policy setting unchanged and its QE pace steady at $120bn p/m ($80bn UST and $40bn MBS). Despite some concerns by the market over a potential shift up, the new median dots still show no hikes in 2022-23 . Looking at the updated dots plot, however, there has been a small bias change towards a hike. 7 of 18 officials now see the potential for at least one hike in 2023, up from 5 in 17 back in December. In 2022 now we have four dots projecting hikes, three of them suggesting one hike to 0.375% and one reflecting two hikes to 0.625%, that compares to the lonesome dot in Dec last year suggesting one hike to 0.375%.

Importantly, the unchanged median dots have been delivered alongside a meaningful upgrade to the economic projections. PCE is forecast to rise 2.4% this year before declining to 2% in 2022 and 2.1% in 2023. Core PCE, the Fed’s preferred inflation measure, is projected to reach 2.2% this year and fall to 2% in 2022. Thus, true to its new average inflation approach, the Fed is confirming that it will tolerate a period of above-target inflation before considering raising interest rates.

The Fed’s other projections showed a strong rebound in GDP growth to 6.5% in 2021 (previously 4.2%) and 3.9% in 2022. The unemployment rate falls to 4.5% in 2021 and back to 3.5% by the end of 2023 . The projected policy stance against this economic outlook is a big shift relative to the “old school” Fed reaction function, unlike its historical pattern the Fed is no longer signalling a tightening in policy as and when the unemployment approaches NAIRU.

Another conclusion from new projections is that the Fed does not see a material rise in wages growth even with the unemployment at 3.5% in 2023. If inflation is seen steady at 2.1% in 2023, then maximum employment requires a lower level of unemployment. Indeed, speaking at the press conference Fed Chair Powell reiterated that the criteria for lifting rates include maximum employment, using a wide range of labour indicators, 2% inflation, not just transitory along with an expected trajectory for inflation to exceed 2% “for some time”. So, on this basis the Fed is not going anywhere for a while.

Market reaction to a dovish Fed has been a risk positive one. Ahead of the FOMC announcement the S&P 500 was down 0.55% while the NASDAQ was down over 1%. Now as I type the S&P 500 is up 0.25% and the NASDAQ is +0.20%. Earlier in the session European equities close mostly lower with the Stoxx Europe 600 down 0.5%.

Prior to the FOMC and playing to the equity weakness led by the IT sector, longer dated UST yields were on the move up with the 30y Bond yield spiking to 2.4587%, a level not seen since 2019 while 10y UST yields traded to a high of 1.686%. The 30y Bond now trades at 2.41% and the 10y Note is at 1.6374%, up 3 and 1bps respectively over the past 24 hours.

Moving onto to currencies the USD has done a big u turn. Pre the FOMC the move up in yields and risk aversion favoured the green back with BBDXY gaining 0.23%. But the improvement in risk appetite and paring of UST yields gains has resulted in a bigger downward reaction with the USD, now down 0.52% in BBDXY terms (DXY -0.40% to 91.50).

European currencies are at the top of the G10 board with NOK, DKK and EUR up around 0.50 %. The Euro now trades at 1.1978 after trading down to a overnight low of 1.1899. Early in the overnight sessions the World Health Organization said AstraZeneca Plc’s Covid-19 vaccine should continue to be administered as the benefits outweigh its risks. Following reports of blood clots in some people who received the Astra shots prompting the suspension of the vaccine programme in many European countries, the European Medicines Agency is due to provide a definitive assessment later today with Italy and France, among other EU countries, indicating that they will lift suspensions if the shot is deemed safe.

The AUD and NZD have also more than recovered the pre FOMC loses. The AUD now trades at 0.7804 (+0.32), after trading to a low of 0.7700 earlier in the session and NZD now trades at 0.7246, after trading around 0.7160 pre-announcement.

Earlier in the day, both US housing starts and permits undershot market expectations, both down more than 10% m/m in February, with weakness attributed to the severe mid-month storm as well as a natural pullback from recent strength. Canadian CPI inflation indicators remained benign but, like the US, are expected to pick up over coming months.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.