Online retail sales growth slowed in May following a fairly strong April

Insight

US and European equities have ended the day in positive territory, supported by solid earnings reports and better than expected US data releases.

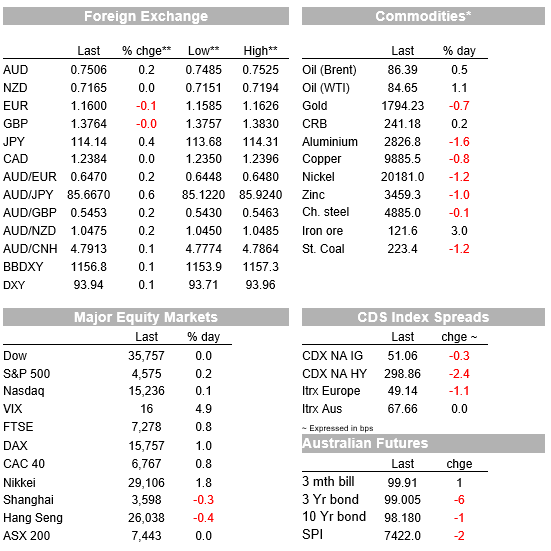

US and European equities are still marching on, recording another positive night with the S&P 500 and Dow printing new record highs. Solid company earnings reports and better than expected US data releases supported the price action. The UST curve flattening themes resumed while breakevens rose again. The USD is a tad stronger with AUD the only G10 outperformer in the past 24 hours while JPY was the weakest.

US and European equities have ended the day in positive territory, supported by solid earnings reports and better than expected US data releases. The S&P 500 ended the day 0.25% higher, after gaining around 0.7% early in the session. The Dow closed +0.04% and the NASDAQ gained 0.06%, after being up just over 1% early in the session. Energy and utilities led the gains in the S&P 500, up just over 0.5% while industrials and communications (both down around 0.5%) underperformed.

UPS (+7.6%) and GE (+2.36%) shares outperformed following strong earnings reports while Facebook struggled (-4.68%) with the market not impressed by yesterday’s after the bell report that revealed a revenue miss. Earlier in the session, Germany’s DAX rose 1% while France’s CAC, the FTSE 100 in the UK and Stoxx Europe 600 advanced about 0.8%.

US data releases where also supportive of the positive vibes evident in equity markets. US Conference Board Consumer Confidence reading surprised on the high side in October, up four points against expectations of a languid result . Present situation and Expectations both higher, gelling with some rise in restaurant booking and other high frequency readings suggestive of some stabilisation/growth in consumer spending into Q4 after what will be likely revealed as a softer Q3, partly held back by Delta. The net jobs plentiful index climbs to even higher levels, playing to the notion of either a further acceleration in vacancies, an even bigger pool of unfilled jobs. Meanwhile, the year-ahead inflation expectations jumped 0.5% to 7.0%, a 13-year high . New home sales also beat market expectations, rising to 800k, in line with the recent lift in mortgage applications.

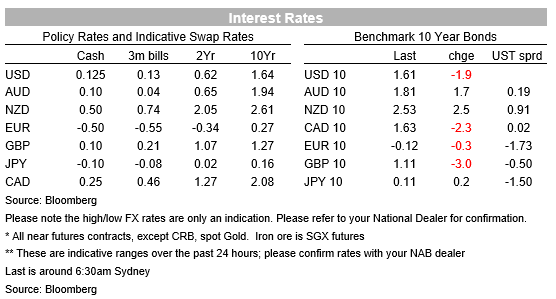

After a short reprieve, the UST curve flattening bias resumed overnight with the 5y30y curve down 3bps to 116.9bps while the 2y10y curve is down 4 bps to 86.8bps . Front end yields have edged a little bit higher while the decline in the long end of the curve was led by the 30y Bond, down 3bps to 2.055%. US breakevens have continued their rise, up another 3 to 4bps in the 2y, 5y and 10y space, the five year breakeven is now a whisker away from 3% at 2.9834% while the 10y now trades at 2.6917%. Inflation expectations are also on the rise in Europe with the 5y5y swap up 5.5bps to 2.08%, almost 20bps higher in the past 5 days.

Undoubtedly the jump in the US Consumer Board inflation expectation reading has played into the move up in breakevens, but the other factor has been the move up in oil prices. WTI gained 0.86% and now trades at $84.6 while Brent is +0.4% now trading at $86.37, oil traders are awaiting US Supply news with the industry-funded American Petroleum Institute’s inventory tally due out later Tuesday (US time). The market is waiting to see whether the data shows inventories tightened further at the Cushing, Oklahoma, crude storage hub.

Moving onto the FX market, it has been a quiet session with the USD a little bit stronger across the board, with the AUD the one exception. After climbing above 75c during our session yesterday the AUD traded to an overnight high of 0.7524, before easing a little as the USD regained its mojo. The AUD starts the new day at 0.7505, the only pair managing to outperform the USD in the past 24 hours (+0.15%). Australia’s CPI is the big data event today and potentially a big factor for RBA pricing expectations which currently see the cash rate at 0.5280% in a years’ time (see more below).

JPY has been the big G10 underperformer, now trading at 114.12 against the USD, likely reflecting the buoyancy in risk appetite, not only in the US but Japan as well with the Nikkei closing yesterday’s session up 1.77%. GBP is little changed on the day, after showing some perkiness overnight, trading to an intraday high of 1.3830 before reversing all the move to end unchanged at 1.3763. The Confederation of British Industry said Tuesday October retail sales were up 30% year over year, compared with September’s 11% annual gain. The latest reading exceeded expectations for an annual gain of 13%, while November sales are expected to be up 35% from a year earlier

In other news, Bloomberg reports that defaults on offshore bonds from Chinese borrowers have set an annual record (currently $8.7b), more than two months after defaults from onshore bonds topped their prior peak. The real estate industry has made up one-third of the offshore bond defaults as the government has pushed to cap property-related debt, crimping refinancing capabilities. Modern Land China , a Beijing developer of energy-saving homes, didn’t repay either the principal or interest on a $250 million bond due Monday, according to a filing Tuesday. Meanwhile, Chinese authorities are pressuring Evergrande’s founder and billionaire to use his personal wealth to prop up the company. Another delayed USD bond coupon will need to be paid by Friday to avoid default for another week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.