Online retail sales growth slowed in May following a fairly strong April

Insight

Bond markets have been supported by some market-friendly data and while Fed speakers were again mixed, it was the more dovish remarks that captured attention.

Events round-up

AU: Monthly CPI indicator (y/y%), Oct: 4.9 vs. 5.2 exp.

NZ: RBNZ Official Cash Rate (%), Nov: 5.5 vs. 5.5 exp.

EA: Economic confidence, Nov: 93.8 vs. 93.6 exp.

GE: CPI EU harmonised (m/m%), Nov: -0.7 vs. -0.5 exp.

GE: CPI EU harmonised (y/y%), Nov: 2.3 vs. 2.5 exp.

US: Goods trade balance ($b), Oct: -89.8 vs. -86.5 exp.

US: GDP (ann’lsd q/q%, 2nd est.), Q3: 5.2 vs. 5.0 exp.

US: Core PCE def. (ann’lsd, q/q%), Q3: 2.3 vs. 2.4 exp.

Bond markets have been supported by some market-friendly data and while Fed speakers were again mixed, it was the more dovish remarks that captured attention. In Europe, country level CPIs came in softer than expected ahead of the euro area print tonight, and while US GDP was revised higher, the Q3 core PCE deflator was revised down slightly. Bonds have extended the recent rally, seeing the US 10-year rate fall to as low as 4.25% overnight. Currency moves are modest on net, while equities wavered. The S&P500 is currently tracking around 0.1% higher.

The data flow as not top tier, but the US GDP was revised higher to 5.2% saar in Q3 from the already elevated 4.6%. That was despite a downward revision to consumption, which was revised down to 3.6% from 4.0%. In the other direction were upwardly revised investment and government spending. Consistent with the recent theme of more-benign-than-feared inflation outcomes, the Q3 core PCE deflator was revised down a tenth to 2.3%y/y from 2.4%, ahead of the October monthly data tonight. Separate October trade data showed a slightly wider than expected deficit of $89.8bn from $86.6bn (consensus $86.2bn) with imports unchanged but exports falling 1.7%. Despite the widening in the month, trade is again unlikely to have a big impact on growth outcomes in Q4, though it did help the Atlanta Fed GDPNow estimate edge lower to 2.1%.

Country level CPIs in Europe are off to a soft start in the run up to today’s preliminary November euro area HICP number. German CPI was 3.2% y/y, 3 tenths below the consensus and down from 3.8%. Spanish CPI was 3.2% from 3.5% (3.6% expected) with the surprise coming in the core, which printed 4.5% from 5.2% and 5.0% expected. Consensus for euro area inflation was 2.7% y/y from 2.9%, but expectations will have shifted to lower.

Fed speakers again offered contrasting views coming after yesterday’s differing messages from the Fed’s Waller and Bowman. Cleveland’s Mester, who has been on the hawkish end of recent commentary, said that “monetary policy is in a good place for policymakers to assess incoming information.” Atlanta Fed President Bostic said that tighter monetary policy and financial conditions are biting harder into economic activity, and that he is increasingly confident inflation is on a downward path. Richmond Fed President Barkin argued for keeping the option open to raise rates again, “if inflation is going to flare back up, I think you want to have the option of doing more on rates.”

On the back of Waller’s comments the previous night, it was the dovish commentary that captured the market’s imagination. Market pricing now shows the first full easing by the Fed is now locked in for May next year and 117bp of cuts are priced over 2024.

Yields were lower globally as the bond market rally continued. The US 2yr yields were 8bp lower to 4.65%, while the 10yr lost 5bp to 4.27%. In Europe, German 10yr yields were 7bp lower at 2.43%, while 10yr Gilts were 8bp lower.

In other central bank speak, BoJ board member Adachi urged patience on monetary policy, saying “we’re not at a phase to discuss an exit strategy, given the current economy and inflation”. He said that the Bank will only be able to confirm next year’s wage trend after the new fiscal year starts in April. His view backs Governor Ueda’s recent comments, which have argued for waiting for wage data to give confidence that higher inflation can be sustained and adopting a very slow approach to policy normalisation. 10yr JGB yields slid to 0.67%, well within the BoJ’s expanded tolerance.

Net currency moves over the past 24 hours have been modest even as the USD has been broadly a little stronger. The dollar is up 0.1% on the DXY. The AUD has been the weakest of the majors over the past 24 hours, following weaker-than-expected monthly CPI data. The AUD found some support just over 0.66 and currently sits at 0.6620. In contrast, the NZD rose from 0.6150 to a high of 0.6208 in the aftermath of the RBNZ’s hawkish-hold, but overnight it has retreated back down to 0.6150, up 0.3% over the day.

The RBNZ produced a set of forecasts in the MPS that raised the chance that further tightening could be required. The Bank seems to have put a lot of weight on recent strength in migration adding to demand pressures on the economy, with the Bank now seeing asymmetric risks to the inflation outlook. The rate track showed a slightly higher peak in the OCR of 5.7% and a roughly six-month delayed start to any easing cycle, with a full rate cut now not projected until mid-2025. Not surprisingly, the market views the need for restrictive policy for such a long time with a great deal of scepticism and that was reflected in the market reaction to the Statement. The 2-year swap rate ended the day up only 6bps to 5.23%, or up 10bps from the pre-MPS level, after global forces supported lower rates earlier in the session.

As for the Australian CPI data the October Indicator came in at 4.9% from 5.6%, below consensus for 5.2%. The excluding Fuel, Fruit & Veg, and Travel number was 5.1% from 5.5% and the annual trimmed mean slowed less, at 5.3% y/y from 5.4%. The essential caveat here is that this is not the full CPI. October is the first month of the quarter which has reasonable coverage of goods prices, but few updates on the services components that are important for gauging domestic price pressures and where the RBA’s worries lie. What detail we did get suggest goods continue to support disinflation and the measured effect rent assistance sets up a temporary reprieve in Q4 from what are still strong underlying rents increases. At the margin those may skew the risks slightly to the downside of the RBA’s November SoMP forecast for Q4 Trimmed Mean of 4.5% y/y, but the November Monthly CPI on 10 January will be more informative. Regardless of the caveats, RBA pricing was pared, there is nothing priced for next week, just 8bp for February, and a cut now mostly priced by the end of 2024.

Coming Up

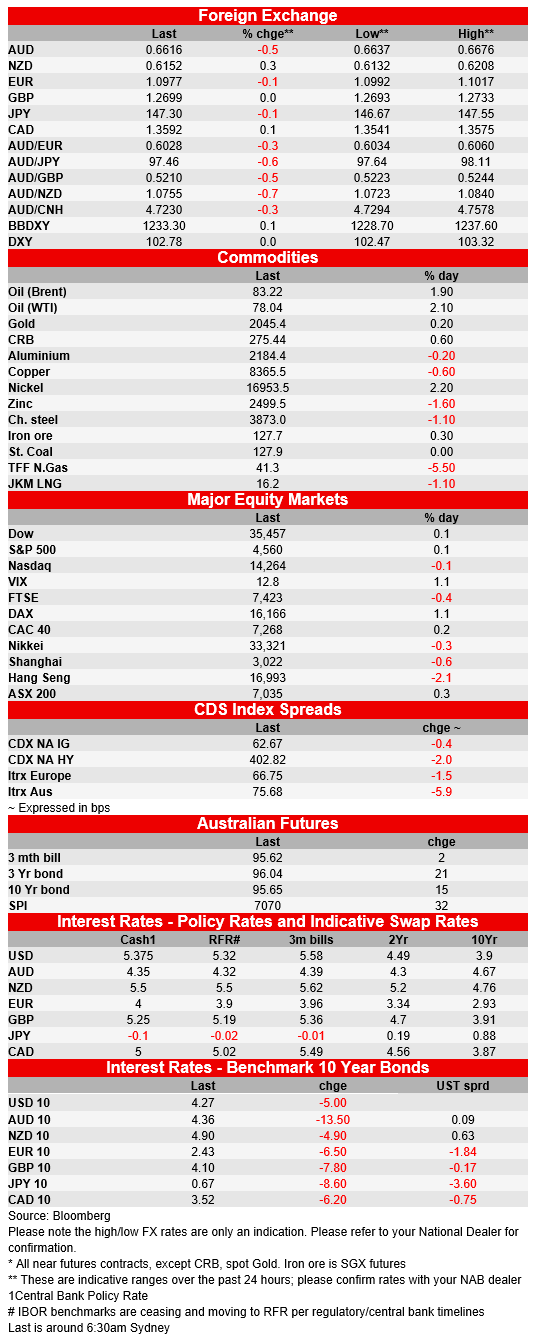

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.