Confidence and Conditions Lift

Insight

Last week’s post FOMC sell-off was overdone, says NAB’s Tapas Strickland on today’s Morning Call podcast, evidenced by a big reversal overnight. Although markets remain jittery.

https://soundcloud.com/user-291029717/swift-turnaround-as-markets-rethink-fomc-response?in=user-291029717/sets/the-morning-call

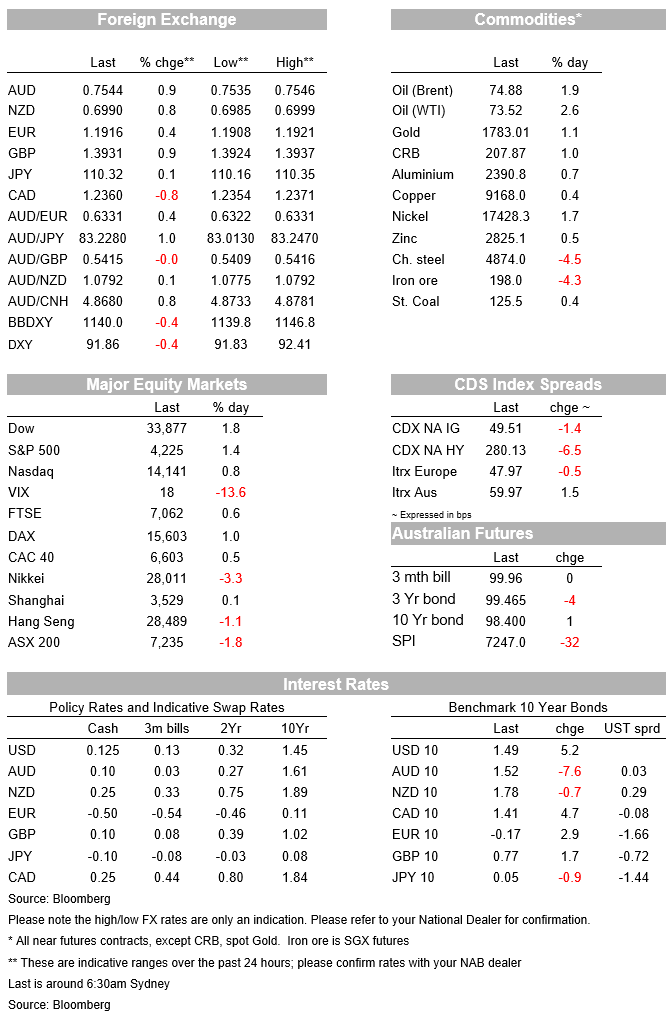

What a week in markets since Wednesday’s FOMC Meeting. The US 10yr yield has gone from 1.49% just prior to the FOMC meeting to a high of 1.59% just after, then to an intra-day low of 1.3526% in Asia yesterday and now trades back to 1.49%! Those moves suggest a significant positioning upheaval with markets not being ready for the Fed to begin talking about policy normalisation with some fearing the Fed was reverting back to its pre-pandemic policy framework and away from its recently adopting Average Inflation Targeting framework. Markets have now had time to reassess Fed rhetoric, encouraged by more toned-down rhetoric from even the most hawkish Fed officials such as Kaplan and Bullard. Across the pond the ECB’s rhetoric also suggests it wont become hawkish anytime soon with a strategy review to be unveiled by September’s ECB Forum

Global equities have rebounded sharply, first starting with European markets with the EuroStoxx50 +0.7% and then to the US with the S&P500 closing up +1.4% with all sectors strongly in the green. The rally back in equities has been fierce with the S&P500 now just 1% off its all-time record high set on June 14th . There has been a clear rotation back into the reflation trade with Financials (+2.4%) and Energy (+4.3%) outperforming, while the small cap Russell 2000 also bounced strongly by 2.2%. The rebound in equities is also mirrored in commodities with Brent Oil +1.9% to $74.99 and Copper +0.4% to 9,168. Global FX moves have also been sharp with the USD (DXY) falling back -0.4% with broad-based gains, particularly amongst the G10 risk proxies of the AUD (+0.9%) and NZD (+0.8), while GBP (+0.8%) outperformed with PM Johnston confirming lockdown restrictions are likely to ease by July 19th.

As for Fed speak, that came after the turn around in markets, though the rhetoric was on net more toned-down from the hawks. The Fed’s Kaplan noted he had been a fan of taking “our foot gently off the accelerator sooner rather than later so that we can manage these risks” around the recovery process, in a bid to “avoid having to press the brakes down the road ”. The Fed’s Bullard also noted tapering discussions would occur at meetings (plural), so an imminent decision is not likely. Both Kaplan and Bullard are non-voters of course and the Fed’s Williams who is a permanent voter on the FOMC and whose views are seen at being more of the centre of the FOMC notes “the data and conditions have not progressed enough for the [Fed] to shift its monetary policy stance of strong support for the economic recovery”. Chair Powell is due to give Congressional Testimony tonight and he is likely to repeat the more measured language of Williams. Powell’s opening statement was published just as your scribe is about to it send, with nothing suggesting of any hawkish leaning with Powell continuing the line of “ As these transitory supply effects abate, inflation is expected to drop back toward our longer-run goal” (See Powell’s testimony statement for details).

Possibly adding to a re-assessment of the Fed’s hawkishness was headlines from the ECB following their latest strategy review. President Lagarde said the ECB was making “good progress” on the strategy review. Results are expected before the September ECB Forum with an expectation of the ECB allowing an inflation overshoot. President Lagarde also noted a brightening in the outlook for the economy as the pandemic situation improves, but also highlighted the differences between the US and Eurozone, saying “they’re in a different situation in terms of the cycle, they’re in a different situation in terms of inflation, and they’re in a different situation in terms of inflation expectations ”. One does not get the feeling the ECB is set to get hawkish anytime soon.

The move in rates have largely seen an unwind of the post-FOMC moves in the longer end, with a corresponding significant steepening. Last week the US 30-year bond fell 17bps and fell another 9bps during Asian trading to as low as 1.925%, but has since sharply reversed course, up some 18bps from that low to 2.1097%. The 10-year rate traded down to as low as 1.35% during Asia yesterday, but now trades at 1.49%, while the 2-year rate has been flat at 0.25%. The Australian 10-year bond future is up some 7bps in yield since the NZ close, so that will set the tone for early trading domestically.

In currency markets, the USD is down 0.4% on the DXY and BBDX with most G10 pairs higher apart from USD/JPY which is flat 110.30. EUR has been the laggard, only up 0.4% to 1.1915 with Lagarde emphasising the ECB’s dovish tones. G10 risk proxies outperformed with the AUD +0.9% and NZD +0.8%. USD/CAD also outperformed. Finally in terms of crypto currencies, Bitcoin saw heavy falls on Monday after China’s central bank ordered the banks and payment processors to take a more active role in curbing cryptocurrency trading and related activities. Media note up to three-quarters of the world’s supply of bitcoin is mined in China. Bitcoin slipped to $32,626, down some 10% since Friday

A quiet day domestically with only Weekly Consumer Confidence and ABS Payrolls. It is also quiet internationally with most focus on Fed Chair Powell in his congressional testimony:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.