Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

The selloff in bonds has seen a ‘reversal of the reversal’.

Another volatile if ultimate quite featureless day Tuesday in terms of net price movements across bonds, FX, and equities. The latter have just closed in New York with the S&P500 and NASDAQ both up around 1%. Netflix has jumped 10% post-close on an earnings beat and stronger than expected subscriber growth. The selloff in bonds, globally not just in New Zealand following the shocking upside surprise in its CPI report (both headline and underling measures) that was subsequently reversed in part on an FT report saying the Bank of England would likely not proceed with QT bond sales at month-end, has seen a ‘reversal of the reversal’. This after the Bank issued a statement that QT would proceed from November 1 – and that the shortfall in its bond sales target (£80bn over 12 months) would be made up by additional sales. UK and Canadian CPI are the data highlight in the coming 24 hours, both important ahead of upcoming BoC and BoE policy meetings.

Incoming economic data, whether real economy or inflation related, is moving markets, and where the highlights of the last 24 hours have been yesterday morning’s shocking high New Zealand Q3 CPI report, and then overnight the pick of the bunch has been stronger than expected US September industrial production. The latter posted a 0.4% rise against the 0.1% market consensus, plus 0.3% worth of upward revisions to prior months, with manufacturing production 0.4% against 0.% expected with 0.2% of upward revisions. Industrial output looks set to make a positive contribution to Q3 GDP (and with a strong base for Q4) and is this so far defying the (recession-type) signal coming from the ISM manufacturing survey (last at 50.9 and in a steep downtrend since late last year).

In contrast the NAHB US Homebuilders index has crunched still lower (38 from 46 against an expectation for no change) and which, ex-ing out the peak pandemic era crunch, is the weakest in over 10 years. A sharp fall in New Home sales in coming month is baked in the cake, and tonight’s housing starts and building permits should offer a further indication of the parlous state of the housing market. A key question for markets and policy makers is how quickly this might start feeding through to (lower) rents and owner-equivalent rents in inflation readings. Not right away is the current indication.

Other offshore data to note was the German ZEW survey, where the expectations readings was better than feared at -59.2 up from -61.9 (-66.6 expected) but current conditions were even worse than expected (-72.2 from -60.5% and -68.5 expected).

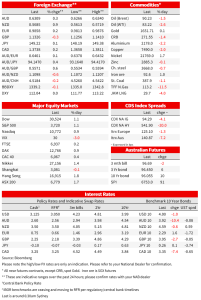

Across markets, bond market volatility continues unabated if down a bit on recent days , albeit the bellwether 10-year US Treasury yield is ending the New York day hardly changed on Monday, very close to 4.0%. This is within a 10bps range (3.96% to 4.06%), and which has (once again) been comfortably exceeded by 10-year gilts, the latter tracing out a 20-point (3.89% to 4.09%) range before ending in London at 3.94%. The rally in bonds during our time zone (including Australian and US guvvies) which following an FT report than the BoE is likely to delay the planned sale of billions of pounds of government bonds in a bid to foster greater stability in gilt markets following the UK’s failed “mini” Budget, has been undone by confirmation from the Bank QT will start on Nov 1 (just one day later than the originally planned Oct31 start date)

The Bank’s statement reads: “ On 28 September 2022, the Bank of England’s (Bank’s) Executive postponed the start of sales of UK government bonds (gilts) held in the Asset Purchase Facility (APF) in light of market conditions at that time. The first gilt sales operation was scheduled to take place on 31 October 2022 and proceed thereafter. In light of the Government’s fiscal announcement now scheduled for 31 October 2022, the first gilt sale operation will now take place on 1 November 2022. The Bank currently expects to conduct APF gilt sales operations in Q4 2022 at a similar size and frequency as had been previously announced, with any shortfall as a result of the earlier postponement relative to its previous sales plan incorporated into sales in subsequent quarters”.

So, sales of £80 bn over 12 months (£40bn from balance sheet run-off and same again from active sales) will on current plans now proceed, with the intention to also sell the same amount as it bought during its emergency operations earlier in late September and earlier this month (totalling more than £8bn). As for BoE Bank Rate pricing, ahead of tonight’s September CPI report (17:00 AEDT) the market prices almost exactly 100bps of tightening on 3 November. Canadian money markets price 56bps for the BoC for next Wednesday’s meeting, in front of its CPI tonight.

To lesser impact on the local bond market yesterday than either the reaction to the NZ CPI report or the FT BoE report, RBA’s Deputy Governor Michelle Bullock gave a hawkish interpretation of the October RBA meeting, despite the downshift to the 25bp increment. She notes “there was no doubt that a further increase in rates was warranted”, there was an “active discussion” about the appropriate size of the increase. Both the Minutes and Bullock’s comments infer that 25bps rather than 50bps was a (very) finely balanced decision. We don’t rule out the RBA reverting to a 50bps rise at its November (or December) meetings, depending on what the intervening Q3 CPI report reveals next Wednesday and the subsequent Q3 WPI data.

In FX not a whole lot of change in the AUD in the last 24 hours, from just under 0.63 at the start of Tuesday’s change to a little above now (0.6310). NZD has been far away the best performing G10 currency since the NZ CPI report, spending some time above 0.57 (just below now). The USD is overall very slightly stronger in late NY trade (DXY +0.03%) with GBP the worst performer (-0.4%) so giving back a little more of its post government fiscal policy ‘U-turn’ gains. USD/JPY has made another new high, ¥149.38, and which doubtless invites fresh jawboning from MoF official today but not, we suspect, intervention this side of ¥150.

Finally, US stocks, after a choppy session, finished in New York with the S&P500 and NASDAQ up +/-1%. A 2.3% rise for Industrials led the gains and which follow the upside industrial production surprises. Netflix has reported after the close, the market liking the Q3 earnings beat and stronger than expected new subscriber number (2.41mn against 1mn expected) even though Q4 revenue guidance of $7.78bn is a bit below the street consensus.

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.