Total spending grew 0.9% in June.

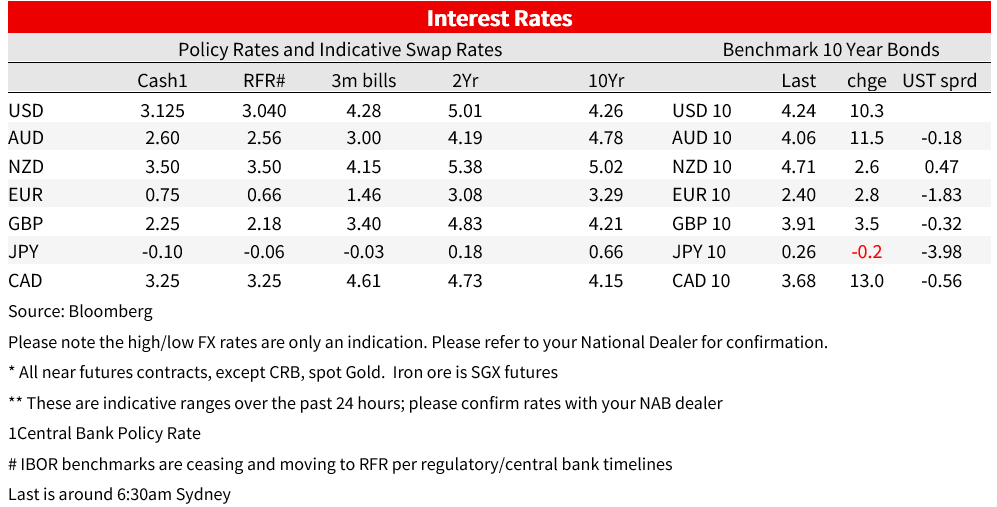

Terminal Fed Funds pricing have lifted to 5.00% by March 2023 from 4.92% last week and continue to price a 75bp hike at the upcoming November FOMC meeting and a 75% chance of a follow up 75bp at the December meeting.

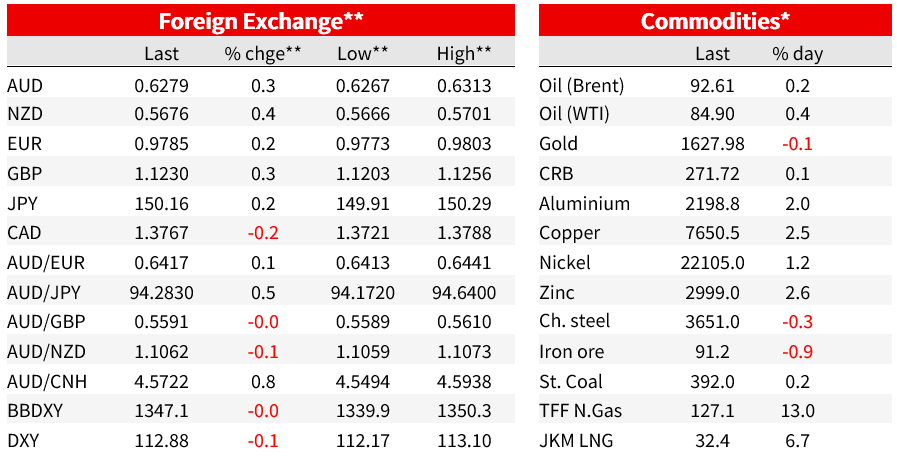

The bond sell-off continued overnight with yields continuing to rise with the US 10yr up 10.3bps to 4.24%, its highest level since 2008. Terminal Fed Funds pricing has also lifted to 5.00% by March 2023 from 4.92% last week and continue to price a 75bp hike at the upcoming November FOMC meeting and a 75% chance of a follow up 75bp at the December meeting. With the 10yr typically peaking around where markets think terminal is, that suggests the trend may have further to go. Hawkish Fed rhetoric continues to drive with Harker the latest. The continued rise in yields is pressuring the Yen with USD/JPY touching 150 (currently 150.20) for the first time since 1990. Japanese CPI up later to day will be closely watched for any implications for the 10yr YCC policy, as will be the Ministry of Finance for any potential intervention – 150 having been seen by analysts as a key line in the sand. In political news UK PM Truss has resigned after 45 days in power, surprising no-one and met with little market reaction given the prior wholesale abandonment of her policies by the Chancellor. A party leadership ballot is expected on Monday 24 October with a new leader likely by Friday 28 October, before the 31 October Budget and 3 November BoE MPC meeting. Betting markets favouring Sunak and Mordaunt, with Wallace and former PM Johnson as outsiders.

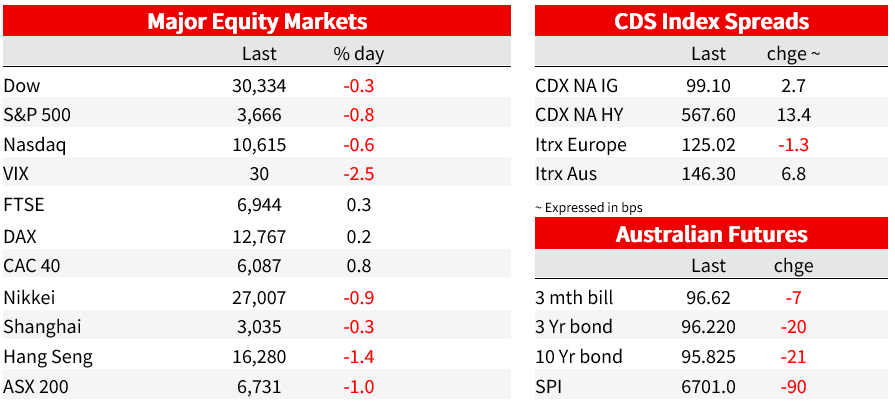

Fed speak continues to dictate direction. The Fed’s Harker noted: “we are going to keep raising rates for a while” and that “given our frankly disappointing lack of progress on curtailing inflation, I expect we will be well above 4% by the end of the year”. A pause at some point is likely in 2023, but Harker re-iterated “what we really need to see is a sustained decline in a number of inflation indicators before we let up on tightening monetary policy”. Interesting comments were also made in an MNI interview with a St Louis Fed research director: “We want to have not just a turning point but solid declines in inflation to start thinking about making adjustments to the policy, and Chair Powell has said that consistently….Right now we have not even changed the trend from increasing to flat or decreasing to assess which way things will decline in 2023″. Fed Governor Cook also pushed the Fed line of keeping rates higher for longer, pushing back on market pricing that while pushing up the terminal rate to 5.0% by March 2023, also prices 23bps of cuts in 2023. The hawkish Fed rhetoric underpinned yield moves with the 2yr yield +5.4bps to 4.6% and 10yr +10.3bps to 4.24%. The 2/10s curve steepened 4bps to -38.2bps, while moves in yields has been driven by both the nominal and the TIP with the 10yr TIP yield up 3.5bps to 1.73% and the implied inflation breakeven rose 6.4bps to 2.50%. Equities are under pressure from the rise in yields despite an ok earnings season so far. The S&P500 fell -0.8% after having been up 1.1% earlier in the day.

Data was not overly market moving. Initial Jobless Claims came in at 214 vs. 232k expected and 226k previously. Overall, the decline in jobless claims suggests the labour market remains tight, although some indicators are suggestive of tightness starting to ease. The Fed’s Beige Book which was released on Wednesday noted six out of twelve districts that make up the US Federal Reserve System reported flat or declining activity attributed to higher interest rates, inflation and supply disruptions. Several districts also reported a cooling in labour demand (citing hiring freezes) and an easing in wage growth (see Beige Book for details). The Philly Fed Manufacturing was also out overnight, coming in slightly weaker than expected at -8.7 vs. -5.0 consensus and -9.9 previously. The details were slightly more positive with employment up and current price indexes continue to suggest increases in prices on balance. The survey’s broad indicators for future activity in six months’ time though did deteriorate, and indicators for current activity and new orders were negative. Existing home sales, not usually market moving, was also out and fell for an eighth straight month.

In FX, moves have been relatively restrained relative to yields. The USD (DXY) is -0.1%, having recovered from its lows of the day as equity markets reversed course. The biggest news is around USD/JPY which rose 0.2% and breached 150 for the first time since the 1990; it currently trades at 150.2. It is unclear whether the Ministry of Finance will intervene with markets having seen 150 as possible intervention level. With the YCC policy dominating the currency, all eyes are on the Japanese inflation data later today to see whether it may imply any possible shifts in 10yr YCC. As for other pairs, GBP was +0.3%, EUR +0.2%, with similar being seen for the antipodes with AUD +0.2% and NZD +0.4%. The AUD did get above 0.6350 at one stage but is back below 0.63 as the USD recovered from its lows of the day. Also, one to watch out for and which created some FX volatility in Asia yesterday was Bloomberg reporting that China was considering reducing quarantine requirements for travellers to the country, potentially requiring 2 days hotel quarantine and 5 days self-isolation at home (from 7 days in a hotel and 3 days at home at present). The proposal hasn’t been signed off by the party leadership and previous relaxation of quarantine rules haven’t been a precursor to any loosening in China’s zero-Covid approach. President Xi reiterated his support for the zero-Covid policy in his speech earlier this week.

In the UK, there hasn’t been a lasting market reaction to PM Truss’ resignation. The GBP initially rallied on the news, trading up as high as almost 1.1340, but it has since given back those gains. UK gilt yields initially fell, boosted by comments by the BoE’s Broadbent who said risks to market hike pricing were more to the downside, but this reversed course with the 10-year yield ending 3bps higher at 3.90%. Pricing for the BoE terminal rate has been broadly steady at 5.15%, this having fallen substantially over recent days from a high of 6¼% after the mini-Budget as Chancellor Hunt reversed course on Truss’ policies. Perhaps more importantly for the gilt market, the Bank of England confirmed that it would start selling down its holdings from 1 November, with eight auctions totalling £6b scheduled by the end of the year. Another leadership contest will now be fought, although the Conservative party will restrict it to a maximum of three candidates, all of whom would need to gather the support of at least 100 MPs of the party. The new PM is expected to be decided by 28 October, after a vote of the party membership, so they will be in place before the medium-term fiscal plan announcement on 31 October.

Finally in Australia, yesterday’s labour market report was slightly weaker than expected, with employment increasing just 1k last month compared to market expectations for a 25k lift. The unemployment rate stayed at an ultra-low 3.5%, though did rise in unrounded terms to 3.54 from 3.48. While volatility in the jobs data has made interpretation difficult over recent months, but overall, the labour market remains tight given still strong labour demand indicators as seen in the NAB Business Survey and in the still elevated level of SEEK Job Ads. Instead. The NAB Quarterly Business Survey which was also released yesterday had the ‘availability of suitable labour’ as being a major constraint on output at a record high in the September quarter. All eyes now on next week’s Q3 CPI on Wednesday with another punchy quarterly reading for core inflation expected. Markets currently price a 14% chance of the RBA returning to a 50bp hike in November, with successive 25bp hikes in November and December fully priced. Terminal pricing is 4.27% by November 2023.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.