We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Global markets have seen a modest retracement of many of last Friday’s violent ‘risk-off’ moves, with equities higher in Europe, so too US government yields up, as too is oil, but in all cases to nowhere near Friday’s closing levels.

https://soundcloud.com/user-291029717/the-bounce-the-restrictions-the-uncertainty?in=user-291029717/sets/the-morning-call

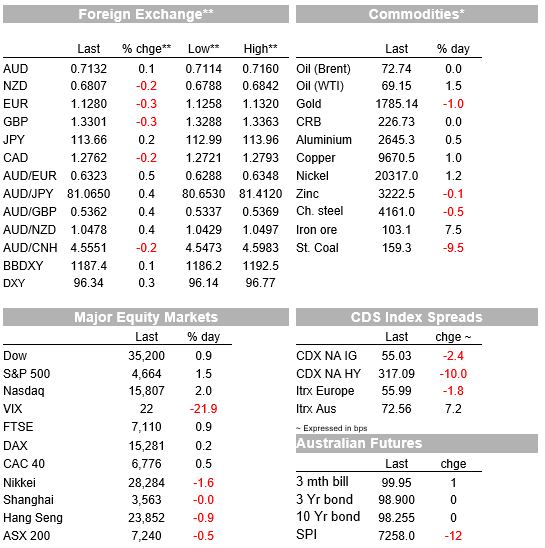

Global markets have seen a modest retracement of many of last Friday’s violent ‘risk-off’ moves, with equities higher in Europe, so too US government yields up, as too is oil, but in all cases to nowhere near Friday’s closing levels. AUD is less than 0.25% up on Friday’s lows. Cautious optimism that the Omicron ciovid-19 variant will prove not to be as seriously as delta is the driver of these moves, but cautious is the operative word here.

Late yesterday, we were fortunate enough to be able to converse with Dr. Rob Grenfell, the special adviser to Australia’s CSIRO and who told a NAB Webinar back in July when were in the mist of the delta outbreak that a new, more infectious, variant would emerge 6-9 months hence, most likely from Africa or India. Now he says that yes, the emerging variant appears like it may be very infectious and that while early reports are that it is not as serious as delta, this is yet to be proven and that he is keenly watching what is going in Europe. We will, he contends, need to wait a few more weeks to see how serious a disease this is, saying South Africa is not good comparator for us. It will also need a few more weeks to determine the effectiveness of current vaccines, though says there is no reason to suggest that they won’t work (that is, that the vaccines will provide some coverage).

US stocks are into the last hour of New York trade showing gains of 2% for the NASDAQ and 1.5% for the S&P 500 (VIX -6.5 to 22) with all eleven sub-sectors of the latter in the green, led by a 2.74% gain for the IT sector. Earlier the Eurostoxx ended 0.5% higher and the FTSE 100 by just under 1%. Yesterday, APAC stocks had a lot of catching up to do to Friday’s big offshore sell off so all ended in the red, led by a 1.6% decline in the Nikkei and where Japan slamming its borders shut because of Omicron was a contributing local factor.

In bond land, Friday’s 16bps drop in 10-year Treasuries has seen about a third of the move retraced, 10s currently +5.5bps to 1.53%, while the 2-year has retraced a lesser 2.4bps following its 14bps Friday fall. Fed chair Powell is testifying to the Senate tonight and front-end rates may prove particularly sensitive to what he has to say. In Europe, 10-year Bunds were up 2bps and UK gilts 4bps.

Currencies aren’t showing any massive moves. The USD is overall a little stronger (DXY +0..%) after Friday’s moves dominated by a rapid repricing of 2022 Fed policy expectations, and the EUR has given back 0.4% of Friday’s gains that came off the back of that. NOK (0.3%) and CAD (0.2%) are among the G10 gainers, albeit outflanked by a 0.8% rise in the SEK, thanks to a partial recovery in oil prices , though oil is falling away into the New York close with WTI crude currently up just over 2% and Brent a much lesser 0.4%. Remember WTI fell by 13% on Friday. AUD at 0.7130 is up from Friday’s low print of 0.7113.

Of some note is that Asia EM currencies have retraced very little of Friday’s falls amid the sounds of borders being slammed shut if only – for now – for a couple of weeks longer than previously planned. The ADXY index up less that 0.1% even though the CNH is 0.13% stronger. The Thai Baht for example, a recent strong EM FX outperformer driven in large part by optimism toward a re-start to the international tourism sector and which Friday’s biggest lower, is down another 0.2%.

The most significant piece of economic news overnight has been German November CPI jumping to 6%, up from 4.6% in October and well above the 5.5% expected. Belgium CPI also jumped, to 5.6% from 4.2% (Spain to 5.6% from 5.4%). Pan Eurozone numbers are tonight. ECB officials have been out en masse though warnings against premature removal of monetary accommodation and still expressing confidence inflation will be back to 2% next year. Governing Council member Villeroy said that while we must monitor latest covid developments and the Omicron strain, Omicron “shouldn’t presumably change the economic outlook too much.”

In the US and continuing the recent trend of US economic data beating expectations, pending home sales shot up 7.5% in October to a 10-month high, with the National Association of Realtor’s Chief Economist saying that existing home sales are on track to exceed 6 million this year, which would be the strongest in 15 years. The Dallas Fed November manufacturing Index fell to 11.8 from 14.6, weaker than the 15.0 expected.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.