We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

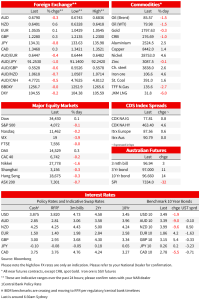

The dollar was softer and US yields lower over the past week as markets both pared terminal rate pricing and priced in more cuts from mid 2023.

EC PPI, Oct: -2.9% (30.8% YoY) vs fcst -2.0% (31.7%), previous 1.6% (41.9%)

US non-farm payroll, Nov: +263k vs fcst +200k; previous +261k

US Unemployment rate, Nov: 3.7% vs fcst 3.7%, previous 3.7%

US avg hrly earnings, Nov: 0.6% (5.1% YoY) vs fcst 0.3% (4.6%) previous 0.4% (4.7%)

US participation rate, Nov: 62.1% vs fcst 62.3%, previous 62.2%

CAD, Net change in employment, 10.1k vs fcst 10k; previous 108.3k

CAD unemployment rate, Nov: 5.1% vs fcst 5.3%; previous 5.2%

CAD hrly earnings, Nov: 5.4% vs fcst 5.4%; previous 5.5%

CFTC: 2y -528.2k from -566.9k; 5y -529.3k from -523.6k; 10y -296.8k from -321.3k

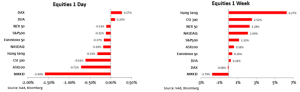

The initial reaction to Friday’s stronger-than-expected payrolls report was standard good news is bad news. Equities opened lower, the dollar was stronger, and the yields jumped higher. That didn’t last, and a positive risk backdrop saw those initial moves grind back through the US session The S&P500 was 0.1% lower on Friday, after opening down 1.2%. The US yield curve inverted further on firmer near-term hiking expectations, with the 2s10s spread at -79bps and back below its levels before Powell spoke last week.

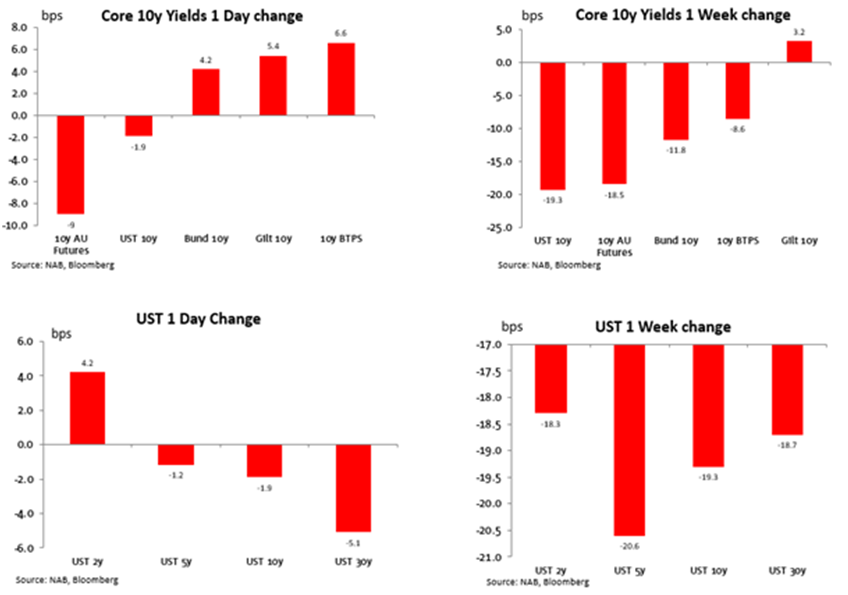

The dollar was softer and US yields lower over the past week as markets both pared terminal rate pricing and priced in more cuts from mid 2023. On the week 2yr yields were 18bp lower to 4.27%, now some 45bp lower than their recent peak of 4.72 in early December. Curves inverted further with the 10yr 19bp lower and the 5yr losing 21bp. The move lower came in real yields. The US 10yr real yield was 30bp lower over the week to 1.05%. The key driver over the week was Powell’s remarks on Wednesday. He didn’t say much new and stuck to the key messages: time to slow the pace of hikes could be as soon as December, but rates will likely go higher than the September projections and remain in restrictive territory for some time. Despite that, markets ran with the nod towards slower hikes in the near term and faded the more data dependent signal on the path for rates through 2023 and beyond. Helping the less-hawkish-than-feared interpretation was acknowledgement by Powell that goods would be imparting downward pressure on inflation looking forward and new rents suggested shelter would be cooling in time.

Fed pricing moved from pricing a peak fed fund rate of 5% in May at the beginning of the week to a low of just 4.83 at one point. The positive assessment that some of the key sectoral drivers of the inflation uplift could turn buoyed assessments the Fed may be knocked off its near-term march deeper into restrictive territory. Cue Friday’s payrolls report that underscored the still tight labour market and an income growth backdrop that makes a fall back to the 2% target challenging. May pricing jumped 14bp on the print, back toward 5%, but settled back to around 4.92%. Higher wages growth in the payrolls report acts as a reminder that the risk on how far the Fed needs to go remains 2-sided. There was an initial move higher in yields across the curve, led by the front end. A more deeply inverted curve was retained even as bonds rallied through the rest of the day, the 2yr ending the day 4bp higher, the 10yr down 1, and the 30yr down 5bp.

As for the details of the payrolls number, the headline non-farm payrolls gained 263k against 200k expected and suggesting a still strong pace of net hiring in November. The 221k private sector gain was the smallest since April 2021, while leisure and hospitality jobs recorded an 88k gain, continuing to catch up after lagging the broader employment recovery. Of more note was average hourly earnings at 0.6% m/m vs 0.3% expected. The number was 0.55% unrounded and helped by softer hours paid in the month but combined with an upward revision to October makes an assessment that the pace of wage gains is cooling already much more difficult. 3m annualised wages growth is now running at 5.8%. Prior to revisions, in October that number was just 3.9%. Continuing to muddy the waters, the household survey, from which the unemployment and participation estimates are calculated, showed weaker employment growth. The unemployment rate remained at 3.7% and the participation rate ticked down to 62.1% from 62.2.

In Canada, employment growth on Friday matched expectations with 10k job growth but the unemployment rate fell to 5.1% (against expectations for a rise to 5.3%), near its lowest levels since the 1970s. Analysts are split between 25 and 50bp from the BoC Wednesday, with market pricing at 32bp.

In Europe, core yields were also lower, the German 10yr was down 12bp to 1.86, though were 4bp higher on Friday. Yields rose globally after the payrolls data, with European markets closing before the recovery in US yields. Market pricing for the ECB was pared over the week. The peak rate is now prices at 2.82 in mid 2023, down from 2.92, while 55bp are priced for next week’s meeting, down from 61. Bank of Frances’ Villeroy and the Bundesbank’s Nagel spoke in a joint interview on Sunday. Villeroy said “we’ll bring inflation back to 2% by the end of 2024 or 2025… this isn’t just a forecast, a projection. It’s a commitment.”

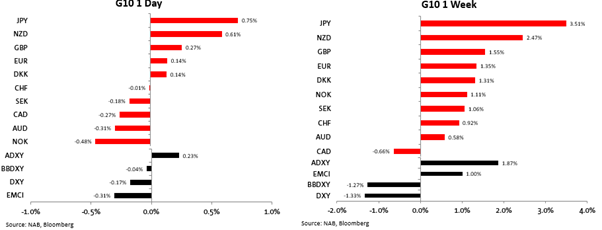

In FX, the dollar was down 1.3% over the week on the DXY . On Friday, the dollar was 0.2% lower on the DXY at 104.506, falling back after being up around 0.8% following the payroll’s print. The DXY is at its lowest level since June and down over 10% since its recent peak on 28 September. The yen was the best performer of the week, up 3.5% against the dollar, helped by the fall in US yields. The yen currently sits at 134.31, levels not seen since mid August. The AUD was 0.6% higher over the week to 0.6795. Also getting some attention was new BoJ board member Naoki Tamura, who told Bloomberg that it would be appropriate for the central bank to conduct a review of policy at the right time, which could be sooner or a little later depending on what happens to prices, wages and the economy. The AUD touched a high of 0.6845 on Thursday, but struggled to extend far beyond 68c in the back half of the week even against the backdrop of broad USD weakness. EUR recovered from its initial post-payrolls dip to close the week at 1.0535, its highest level since early July.

Equity markets pared losses on Friday to be relatively little changed. The S&P500 was down just 0.1% after opening 1.2% lower following the payrolls report. The NASDAQ was 0.2% lower. Equities began the week lower and were down as much as 2.2% prior to the rally on Powell’s remarks on Wednesday, The S&P 500 is up 1.1% on the week and is 15% below the peak on 1 April.

In Asia, the Hang Seng was 0.3% lower on Friday, but was up more than 6% over the week as optimism about a transition away from Covid-zero extended on some easing of restrictions including expanding home quarantine and removal of less target restrictions in some cities. On Sunday, Shanghai joined other cities including Beijing, Shenzhen and Guangzhou in relaxing restrictions. Shanghai will scrap PCR testing in outdoor public venues and public transport. A number of other cities also announced they would relax some curbs over the weekend. While the easing of some restrictions does not equate to a wholesale shift away from the dynamic covid zero strategy just yet, it is further evidence of a shifting approach and financial markets look to be firmly focussed on the longer term outlook over the near-term hit to activity as virus cases look set to continue.

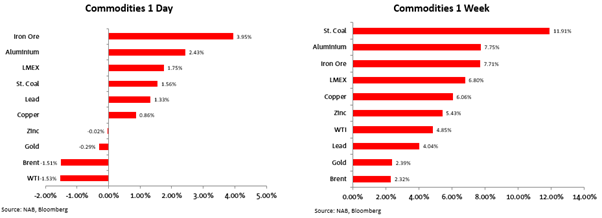

Commodities were generally higher over the week, boosted by optimism over China reopening even as the spread of the virus weighs on activity in the near term. Brent oil was 2.3% higher to US$85.42 over the week, but lost 1.5% on Friday. The EU finalised the price cap on Russian oil at of US$60/bbl. That’s above the $50 the Russian Urals crude already trades and so is at a level that could keep Russian oil on the market. Moscow said it would rather cut production than sell to countries that adopt the cap. On Sunday, OPEC+ left output unchanged as expected but said the group was ready to “meet at any time” and could “take immediate additional measures”. That comes after the large 2 million barrel-a-day reduction agreed at its last gathering.

NAB Markets Research Disclaimer

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.