Online retail sales growth slowed in May following a fairly strong April

Insight

It has been a nervous start to the new week with big moves seen in rates, oil and FX markets.

https://soundcloud.com/user-291029717/the-divided-story-of-rate-expectations?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

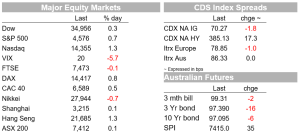

It has been a nervous start to the new week with big moves seen in rates, oil and FX markets. 2y UST extend their parabolic rise, flattening the 2y10y UST curve as the 10y Note ends a volatile day little changed. BoE Bailey softened guidance triggers a rally in Gilts while in FX land, USD/JPY continues its vertical rise, boosted by BoJ defence of its YCC policy. NZD, NOK and GBP are the other notable underperformers with AUD and EUR showing resilience versus a broadly stronger USD. In contrast, equity moves have been more subdued, EU equities closed little changed while US stocks edge higher in afternoon trading with the VIX extending its recent decline to 20.

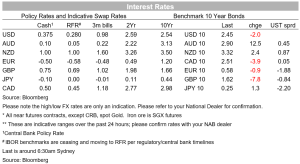

After the big rise in UST yields on Friday, on the back of a series of hawkish upgrades to the Fed funds rate outlook by some US banks, the US Treasury market opened the new week in Asia under pressure as investors in the region caught up with the weekend news . After a volatile session 10y UST yields traded in a 10bps range reaching an intraday high of 2.5530% around the time Sydney called it a day. A move lower in core global bond yields ensued during the European session, led by a rally in UK Gilts following comments from BoE Governor Bailey.

In his first public comment since the BoE rate decision early in the month, the Governor softened its cash rate guidance noting that the Bank’s guidance should reflect current uncertainties , including the spike in energy prices in the wake of Russia’s invasion of Ukraine. Bailey also said the UK is facing an historic hit to real incomes that will weigh on demand and growth and start to pull down domestically generated inflation, adding that “The bank doesn’t have a policy tool to make that hit go away”.

Money markets trimmed their BoE bets to 137bps of rate hikes by December, versus 148bps before Bailey’s comments and 141bps on Friday. 10-year gilt yields ended Monday 7bps lower to 1.62% while 10y Bund yields closed 1bps lower to 0.58%.

After trading down to on overnight low of 2.4126%, 10y UST yields recovered some ground to end the US session relative unchanged at 2.4586%. Notably as well, the relentless rise in 2y UST yields continued during our Monday night, up another 6bps to 2.3280%, that is a 100bps rise since March 1st and a big factor contributing to the ongoing flattening theme in the UST curve, the 2y10y curve now trades at 13bps, 7bps lower on the day, further enhancing the market perception that it is only a matter of time before we see an inversion, increasing concerns over an imminent US recession, given the curve’s historically reliable signal.

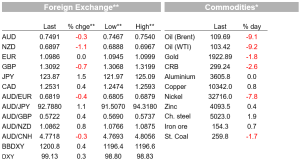

The Japanese yen the remains the main story in FX land with USD/JPY extending its vertical rise over the past 24 hours. The BoJ’s YCC policy which confines the 10y JGB rate within a +/-0.25% range has been one big factor of recent yen weakness amid a rise in core global bond yields. Recent JPY weakness is also explained by Japan’s energy dependency with the rise in oil and gas exposing its economy to a terms of trade shock. Against this backdrop and concerns over rising inflation, albeit from a low base, the market has been wondering if the BoJ’s commitment to its YCC policy was wavering. Well, yesterday the Bank sent a strong signal that YCC is here to stay for a while yet, offering to buy unlimited amount of 10-year JGBs at 0.25%, the first action to contain the sell-off of the Japanese bond market since mid-February. This attracted no bids, but another offer in the afternoon following the 10-year rate breach of 0.245%, saw 64.5 billion yen taken up. The affirmation of its YCC commitment, triggered an aggressive yen selling with USD/JPY rising to a high of ¥125.09, before easing down to ¥123.87 currently (JPY is down 1.13% over the past 24 hours).

NOK, ( -1.2%), GBP (-1.10%) and NZD (0.71%) are the other big FX underperformers with declines for the first two more easily explained than for the kiwi . NOK’s decline seems consistent with the 10% fall in crude oil prices as the market reassess the demand outlook following news of Shanghai’s lockdown. As my colleague Jason Wong noted, the city’s 2 staged lockdown that began yesterday means that nearly 5% of China, weighted by population is now forced to reduce their energy/petrol consumption. Brent crude trades this morning at about USD109 per barrel after trading close to USD120 at the Asian open.

GBP softness is a direct result of a decline in Gilts yields following BoE Baily’s comments, but the decline in NZD is less clear. That said the kiwi has had a good run of late, so a period of consolidation looks to be in order with the pair now trading at 0.6898. The AUD has shown a bit more resilience, only down 0.33% against a broadly stronger USD ( now at 0.7492, but similar to the kiwi, after a strong run up to 75c, the AUD is now taking a well deserved break and while we still expect higher levels over the course of 2022, recent price action is consistent with our view that the AUD is likely to do some work around the 75c area before heading higher over coming quarters.

Equity markets have been less volatile than other markets. European equities erased earlier gains and closed little changed as investors weighed the risks from rising bond yields against Ukraine war risks. Meanwhile US stocks staged a decent recover in the afternoon session with the S&P500 ending the day up by 0.71% while the Nasdaq closes 1.31% higher.

The data calendar has been light. The US goods trade deficit narrowed slightly to $106.6b in February from the record high in January, adding to the chance that net trade will be a drag on Q1 GDP growth. The inventory data released were slightly stronger than expected, an offsetting factor for Q1 GDP, but Pantheon Macroeconomics notes that the risk of a zero headline GDP print remains real.

Russia and Ukraine peace talks in Istanbul begin tonight. The chance of a deal still looks slim. Ukrainian President Zelensky talked over the weekend about the conditions under which Ukraine might accept neutral status but he also rejected two of Russia’s war aims, including that the Ukrainian government won’t step down nor accept demilitarisation of the country.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.