Online retail sales growth slowed in May following a fairly strong April

Insight

US CPI numbers came in on the high side and markets have reacted swiftly with equities falling sharply and the bond sell-off pushing Treasury yields up.

https://soundcloud.com/user-291029717/the-inflation-shock-we-were-warned-about?in=user-291029717/sets/the-morning-call

“You know we getting hotter and hotter; Sexy and hotter, let’s shut it down; Pound the alarm; Pound the alarm”, Nicki Minaj 2011

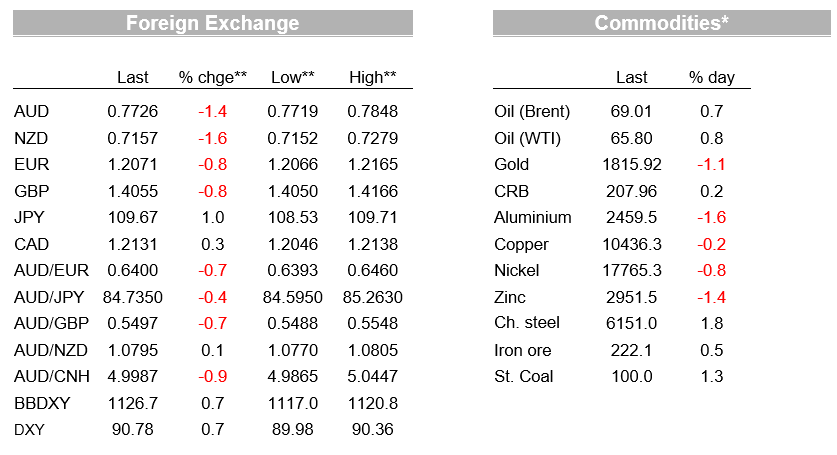

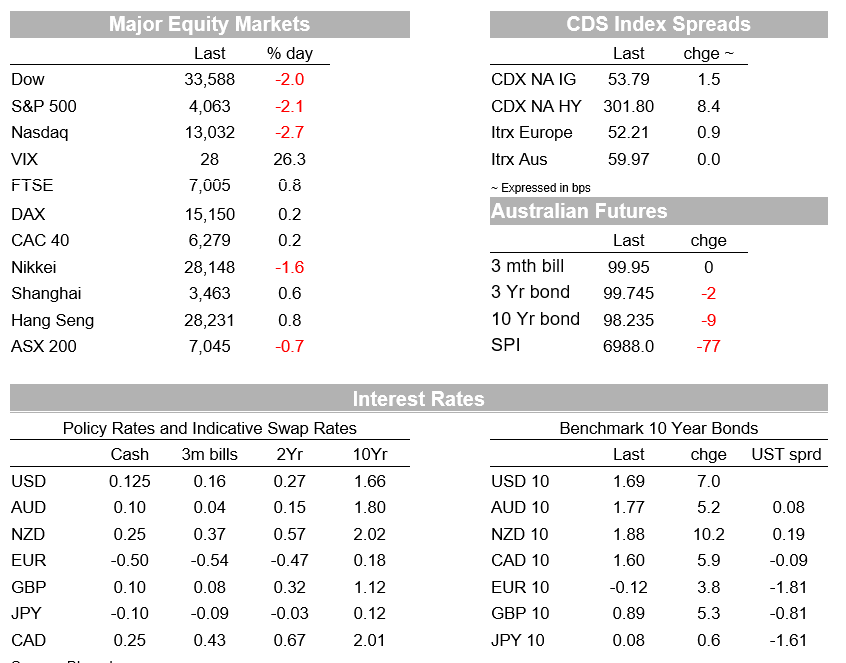

Inflation alarm bells sounded overnight with US Core CPI Inflation printing triple the market consensus at 0.9% m/m (consensus 0.3%). The market reaction was swift with equities tumbling on Fed normalisation fears, with losses extending into the close (S&P500 -2.1% and NASDAQ -2.7%). Eurodollar futures now price an 80% chance of the Fed hiking rates by the end of 2022, significantly earlier than the Fed dot plot which see the Fed hold in 2022 and in 2023. Fed speak post the CPI report repeated the familiar lines of its transitory, but some daylight within this rhetoric starting to emerge with Clarida repeating the obvious that if the Fed’s transitory view proved wrong, then the Fed would not hesitate to act. Unfortunately we will only really know if the lift in inflation proves to be transitory towards the end of the year and into next year as supply disruptions start to ease. Yields lifted on the rate outlook with the US 10yr +7bps to 1.69% and the 2/10s curve steepened by 5bps. Implied inflation breakevens rose 2.1bps to 2.56% for the 10yr with real yields lifting 5bps to -0.87%. Higher US yields supported the USD with BBDXY +0.7%, while the AUD (-1.4%) and NZD (-1.6%) underperformed in the risk-off environment.

First to the US CPI. Core CPI Inflation in April printed triple the consensus at 0.9% m/m (consensus 0.3%), while the annual rate at 3.0% y/y is the highest since 1996 (consensus 2.3%). Headline CPI Inflation was also hot at 0.8% m/m and 4.2% y/y. The key question for markets and for fears around inflation is how much of the rise in April is due to transitory one-offs, and how much reflects more permanent inflationary pressures. Three CPI components are clearly transitory and added almost 0.5 points to the monthly inflation print (airfares +10.2% m/m, used cars +10.0%, lodging costs 7.6%). Outside of that there appears to be some inflationary impulse with prices notably lifting for restaurant meals even with elevated unemployment (+0.3% m/m and 3.8% y/y). It will take a number of months for a clearer read on US inflation to emerge given extensive supply chain disruptions, as well as consumer spending having been concentrated in March and April due to the recent stimulus cheques. Given the uncertainty, markets are likely to continue to price in the chance of the lift in inflation being more durable and the risk the Fed may need to normalise policy earlier than previously indicated.

We did not have to wait long for a reaction from the Fed given four Fed officials were on the speaking circuit overnight. Vice-chair Clarida said he was “surprised” along with everyone else, but still held to his view that the lift in inflation was going to be transitory, calling it “one data point”. The Fed’s Bostic also made similar comments, noting that “we are going to see a lot of volatility in prices and pricing…” and that this does not warrant a policy response. Some daylight though is starting to emerge with Clarida again re-stating the obvious point that “ if, contrary to our baseline view, demand relative to supply was excessive and persistent and pushed up inflation and inflation expectations to levels that were not potentially consistent with our mandate…we would not hesitate to act and to use our tools to bring inflation back down to our 2% longer-run goal.”

As for the Fed’s tolerance, Clarida has previously noted that the Fed will only know if they are wrong on inflation towards the end of the year and into next year. Thus it will take a string of strong monthly CPI increases for the Fed to doubt its view. For now strong CPI prints adds to the argument of the Fed needing to taper its asset purchases and Jackson Hole in August is shaping up to be one possible date when this is announced. As for rate normalisation and inflation tolerance, the Fed’s Harker noted 3% is probably the “maximum” inflation he would like to see, though he would be more comfortable with inflation at around 2.5%. Much will also depend on the Fed’s employment goal with payrolls still 8.2m below pre-pandemic levels. Either way normalisation when it comes could potentially be steep given the economy would be running at full capacity and in danger of overheating which is a point that has been made previously by Summers and former NY Fed President Dudley.

Market reaction to the CPI numbers was swift. The S&P500 closed down -2.1% and is now down 4.0% since Friday’s record high. All sectors closed in the red apart from Energy (+0.1%), with IT (-2.9%) and Consumer Discretionary (-3.3%) leading the falls. Reflective of the underperformance of growth stocks, the tech-heavy NASDAQ is down a sharper -2.7%. The fear for the equity market is the Fed lifting rates aggressively if there is some notion of the Fed being behind the curve as some like Summers have argued. Moderate inflation and a slow moving Fed has been supportive to date, but inflation and a reactive Fed is negative for valuations. Either way yields and equities are likely to be in a dance as much better than expected economic data continues to challenge central banks rates guidance not only in the US, but also in many advanced economies. Meanwhile for commodities, prices overall remain well supported, as one would expect in an inflationary environment, with Bloomberg’s commodity price index showing gains despite the stronger USD backdrop.

Bonds also sold off with US 10yr yields up 7bps to 1.69%. Interestingly the 2yr yield was little moved with the 2/10s curve steepening by 5bps. Higher US-global rate spreads and weaker risk appetite have lent some support for the USD, which is higher against all the majors bar the CAD. The AUD (-1.4%) and NZD (-1.6%) have been whacked the hardest with the AUD currently trading at 0.7726. GBP, EUR and JPY also show notable falls from this time yesterday, down in the order of 0.6-0.8%.

The inflation shocker raises the question on whether this changes our negative outlook for the USD. Our initial reaction is no. The combination of higher inflation, a massive fiscal deficit and strongly rising trade deficit are all USD-negative. If US inflation is, say, 1% higher than expected then the equilibrium fair value of the USD is 1% lower. Changing interest rate expectation and gyrations in risk appetite can obviously have a positive short-term impact on the USD, but these shouldn’t affect the medium- term trajectory. The biggest risk to our positive AUD/USD view is if inflation does get out of hand, requiring a decent interest rate response by the Fed and risk assets come tumbling down from their lofty levels.

In other economic news, the UK economy contracted by 1.5% q/q in Q1, but the monthly track showed a decent pick-in in growth in March, confirming that a strong rebound is underway as lockdown restrictions ease. On the weak side, euro area industrial production rose just 0.1% in March, well below expectations, while China credit growth slowed in April after a record first quarter, encouraged by the PBoC’s intention to slow down credit expansion. Aggregate Financing was 1850 v. 2290 expected.

A quiet day in Australia and offshore. Fed speakers and the US PPI are worth watching after last night’s hot CPI print. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.