NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Despite lots of data for markets to chew over, they are looking for a directional lead from non-farm payrolls, says NAB’s Gavin Friend. Whether they’ll get it or not is the question.

https://soundcloud.com/user-291029717/the-last-day-of-treading-water?in=user-291029717/sets/the-morning-call

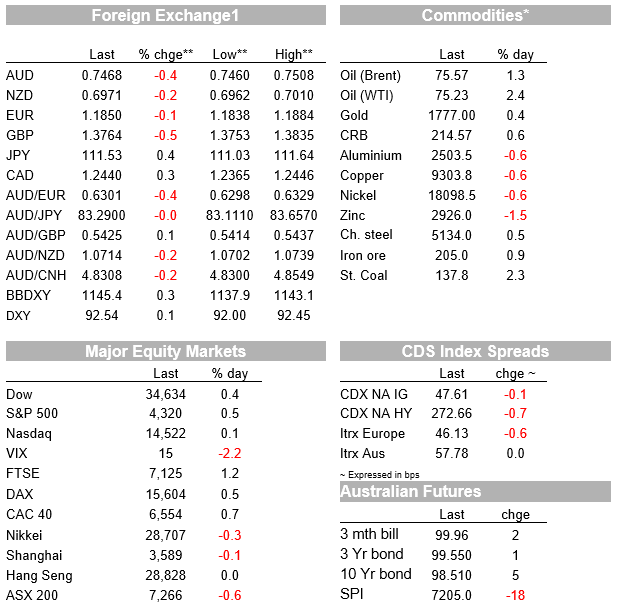

Any opportunity to quote the great Tom Petty is one that needs to be taken. So, as we wait for US non-farm payrolls tonight, it seems that it is all clear in the western front. US and EU equities closed up on the day with the S&P 500 recording its sixth day of gains. The US data flow has remained robust with the US ISM Manufacturing printing above 60 (trivially below expectations), UST yields continue to trade in tight ranges, showing little reaction to the data while the USD has remained on the ascendency, recording its fourth daily gain in a row. AUD is one big underperformer, technically wounded, while GBP is the other, after dovish comment from BoE Baily.

The US ISM Manufacturing was the big data release overnight and it essentially came in line with expectations , dipping slightly to 60.6 in June from 61.2 in May and a smidge below expectations for a print of 60.9. Overall US manufacturing activity has remained at a very robust level, encouragingly too the biggest driver of the dip in the headline was a 3.7 point drop in the supplier deliveries index, hinting at the idea that may be US has reached a peak in the supply bottle neck squeeze, although we are still a long way from normal. Another notable development was the employment index slipping one point below the 50 level, labour supply is the other major constraint with one survey respondent noting “”Lack of labor is killing us.”. Meanwhile, initial jobless claims fell to a new post-Covid low of 364k. In Japan, the Tankan survey of large manufacturers rose to its highest level since 2019, albeit by slightly less than expected.

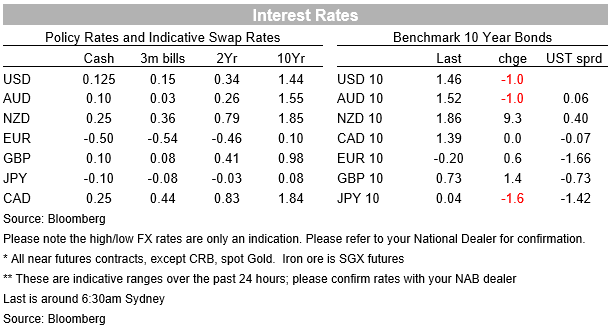

Reaction to the ISM report triggered a push up in UST yields and the USD, although with the move up in the former was reversed a couple of hours later while the USD retained its gains . 10y UST yields were drifting lower ahead of the data release, printing an overnight low of 1.4527% immediately after, then climbing to a high of 1.4832%, before ending the day close to the overnight low at 1.4578%. Overall 10y UST yields continue to trade in a very subdued manner and close to the bottom of the 1.40% to 1.74% range held since late February this year. The bond market seems to be in a very cautious mood ahead of non-farm payrolls tonight.

In contrast the USD story this week has been about onwards and upwards with the big dollar recording its fourth consecutive daily gain with the DXY index up 0.13% and BBDXY +0.27%. Unlike the cautious pattern in UST yields, it seems USD bulls are pricing a solid outcome from US labour market data tonight, buy the rumour sell the fact? Notably too, the market and USD showed little reaction to comments from Philadelphia Fed President Harker who argued the tapering process should start this year, with purchases potentially reduced by $10b a month over 12 months to get down to zero.

Looking at G10 pair, AUD ( 07467) and GBP (1.3768) are the big underperformers, down 0.47% and 0.54% respectively. Fundamentally is hard to argue for a softer AUD, the domestic AU data flow over the past 24 hours has been a solid one. AU Job Vacancies grew another 23% in the three months to May to be 57% above pre-pandemic levels, AU May Trade surplus increased $1.5bn to $9.7bn (consensus $10.5), but really the trade story is a solid one with both exports (+$2.4bn, +6%) and imports (+$0.9bn, 3%) rising in the Month. Lastly, AU dwelling Prices rose 1.9% m/m in June to be 13.5% y/y.

Of course, that is not all the AUD story, covid remains a concern and a headwind for the AUD. Plus the technical picture is also a negative one. The AUD now trades at 0.7467, the pair has broken below its rough 0.75 to 0.80 range held since the start of the year and is now testing a key support level. A break below 0.7470, means the AUD has a clear runway to extend it decline with not a lot of obstacles on its way. FX reaction to non-farm payrolls tonight will be important.

The EUR is down only slightly overnight (-0.1%) but has still managed to post a three-month low, around 1.1840. USD/JPY has continued to push higher, to around 111.60, its highest level since last March. Alongside the GBP (-0.6%), which has underperformed on some dovish comments from BoE Governor Bailey, the JPY (-0.5%) has been one of the laggards overnight.

In his annual Mansion House address, Bank of England Governor Bailey reiterated the message from the most recent monetary policy report, saying the Bank’s job was to ensure it didn’t undermine the recovery by tightening prematurely. The headlines caused an immediate dip in the GBP although there was little impact on UK interest rates. Bailey adheres to the conventional central banking view that current inflation pressures will prove temporary, citing base effects, the eventual easing of supply-related disruptions and a post-reopening switch to spending on services, a part of the economy with greater spare capacity. The message contrasts with that of departing Chief Economist Andy Haldane who, in his last speech for the Bank earlier this week (well worth reading), warned of a significant and persistent rise in inflation that could affect monetary policy credibility.

The grinding rally in US equities has continued overnight, with the S&P 500 adding 0.52%, its sixth consecutive daily increase, to a fresh record high . Under the surface, there has been some rotation back into the cyclical sectors, with energy stocks leading gains and tech stocks underperforming. Subdued market volatility has seen the VIX fall to a post-Covid low of 15.5. European equities also close higher with main regional indices up between 0.29% and 1.27%

Oil prices are up around 1% overnight, after reports that OPEC+ would increase supply by less than expected. An internal committee of the cartel proposed that supply be increased each month between August and December by 400,000 barrels/day, less than the previously reported 500,000 figure. The meeting was postponed to tomorrow after a late objection from the UAE, but oil prices have still retained most of their overnight gains, with Brent crude oil trading just over $76.

In other news, the OECD reports that 130 countries and jurisdictions have agreed to a new global taxation rule setting a minimum tax rate for corporations. The agreement sets the stage for the G20 finance ministers to sign off on an agreement in principle at their meeting next week. If so, there is a potential for the new rules to become effective as soon as 2023, limiting the ability of multinationals including the likes of Google and Facebook of avoiding tax payments, setting an effective rate of “at least 15%” with smaller countries benefiting from a bigger share of tax revenue from foreign firms.

Finally, speaking to Bloomberg former NY Fed President Dudley gave an interesting take on whether the Fed could consider raising the Funds rate before ending QE . Given the recovery for many economies has been evolving faster than originally expected, this question has been raised for many Central Banks, including the RBA and RBNZ. Dudley’s take is that it would be very unlikely, noting that: First, buying assets and raising short-term rates would be adding stimulus with one hand and taking it away with the other. This makes no policy sense. Second, if the economy is doing better than expected and the Fed wants to remove stimulus more quickly, it can simply increase the pace of the taper. This would lead markets to expect interest rates to start rising sooner, too. Third, the Fed wouldn’t want to weaken an important tool of monetary policy. Markets expect interest rates to start rising only after the taper is complete. This perception increases the power of asset purchases in the first place: Market participants know interest rates will stay at zero as long as the Fed is still buying.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.