US Fed hikes by 25bps as expected, keeps options open, tightening bias remains

Post Powell yields & USD are down (US 2yr -7bps to 4.83%; DXY -0.3%)

Fed staff no longer forecasting a recession, rate cut prospects a “full year from now”

Coming up: CH Industrial Profits, ECB (25bp hike), US Q2 GDP & Jobless Claims

“Well this could be the last time; This could be the last time; Maybe the last time – I don’t know – oh no, oh no; Well I’m sorry girl but I can’t stay”, The Last Time, John Farnham 2022 (note Farnham while announcing his decision to retire in 2002, came out of retirement in 2008 to tour across Australia).

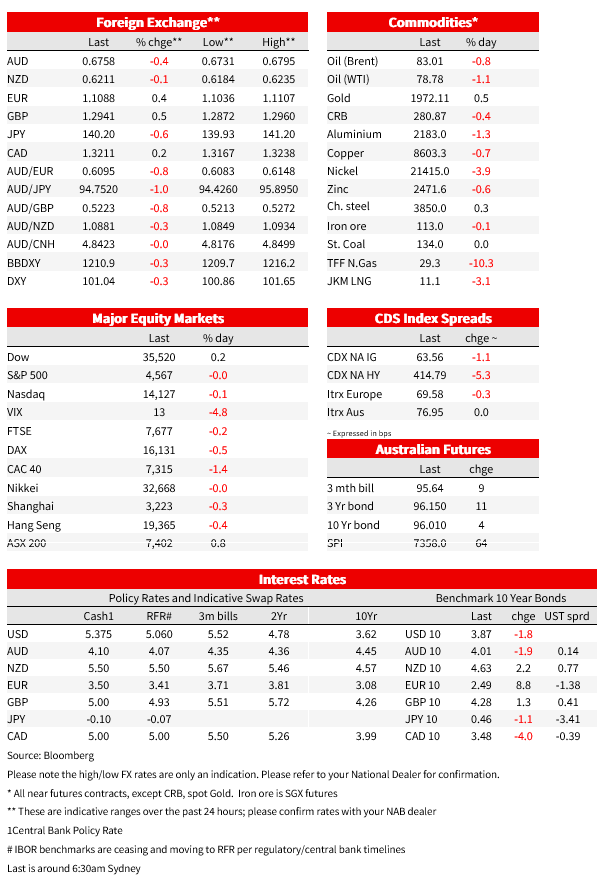

The US FOMC hiked rates by 25bps to 5.25-5.50% as universally expected , the post-meeting Statement was almost unchanged, while there was minimal forward guidance given in the press conference. Yields were mostly lower on net post Powell after having risen into the decision. 2yr yields were -7bps to 4.83% (-3bps past 24 hours) and 10yr yields -2.5bps to 3.86% (-1.6bps past 24 hours). Markets continue to price around a 40% chance of a follow up hike by November, though pricing of cuts extended with 136bps of cuts thereafter by end of 2024 (up from 130bps yesterday). The USD weakened alongside lower yields with DXY -0.3%. Equities meanwhile rose with the S&P500 +0.3%, though over the full session was -0.0% having traded weaker into the FOMC. Two interesting comments were that “the fed staff…are no longer forecasting a recession ” and for those looking for cuts “that’s just going to be a judgement that we have to make then – a full year from now”. Overall the Fed is data dependent with a mild tightening bias.

Other interesting snippets from Powell’s press conference. Although there wasn’t much forward guidance given, Powell did state: “we think we’re going to need to hold, certainly, policy at restrictive levels for some time, and we’d be prepared to raise further if we think that’s appropriate” and that “we can afford to be a little patient, as well as resolute, as we let this unfold”. Yields seemed to fall in relation to an answer about whether the Fed could hike in September, with Powell declining to give a hawkish answer and instead responded with data dependency: “I’m going to tell you again what we’re going to do in September,”…“ We’re going to look at two additional job reports, two additional CPI reports, lots of activity data. That’s what we’re going to look at, and we’re going to make that decision then. That decision could mean another hike in September or it could mean that we decide to maintain at that level.”

In the FOMC’s view, while real rates were in “meaningfully positive territory”, policy has not been “restrictive enough for long enough” to do the job. And there’s still “a long way to go.” Emphasising the higher for longer theme, Powell also noted “many people wrote down rate cuts for next year. I think the median was several, for next year, and that’s going to be a judgment that we have to make then, a full year from now.” One positive was that “the fed staff…are no longer forecasting a recession” (instead they now have a noticeable slowdown in growth starting later this year). Powell also mused that the Fed could continue its balance sheet runoff while lowering policy rates under certain circumstances (see US Fed: Press Conference for details).

The only other event worth noting is yesterday, Australian Q2 CPI which was slightly softer than both market and RBA forecasts . Headline CPI was 0.8% q/q and 6.0% y/y (consensus 1.0%/6.2%; NAB 0.9%/6.1%; RBA SoMP 6.3%). The core Trimmed Mean was 0.9% q/q and 5.9% y/y (consensus and NAB 1.1%/6.0%; RBA SoMP forecast profile 6.0%). For both headline and trimmed mean, it was the lowest quarterly read since September 2021. The details revealed greater than expected goods disinflation is now occurring (the surprise was garments and motor vehicles), but services inflation – often seen as stickier – moved higher and our estimate of ‘market services excluding travel and telco’ printed at 1.9% q/q and 6.6% y/y. We still see Q3 CPI as printing high given likely pass through from the minimum/award wage increase, higher energy prices, as well as well-telegraphed price increases in other services components. The concern remains on services inflation, which could impede the aim of getting inflation back to 3% by mid-2025.

As for NAB’s RBA view, we now expect the RBA Board to leave rates unchanged in August on the back of this lower than expected CPI outcome, awaiting more information on the evolution of the economy and inflation, amid uncertainties over the lags in previous policy increases. High services inflation though means continued risks of higher rates over coming months. Markets pared back expectations for a possible RBA hike next week from a 60% chance down to about a 25% chance. Lower Australian rates drove the AUD down by -0.7% initially, but the fall in the AUD has now been partly retraced with the AUD now ‑0.4% to 0.6758 over the past 24 hours as the USD weakened post Powell. RBA whisperers in the press were mostly quite. There was one article by the Herald Sun’s Terry McCrann, which noted “There is no way that the RBA would hike in the wake of this sort of data – even after the very strong jobs numbers of last week” (see McCrann: Rates to stay on hold after surprise good inflation numbers).

FX moves mostly reflected USD weakness post-Powell with DXY -0.3%. Over the past 24 hours: EUR +0.4% to 1.1086, GBP +0.5% to 1.2938, and USD/JPY -0.6% to 140.20. The AUD as noted above was -0.4% to 0.6758 and NZD was unchanged at 0.6215 after having declined alongside the AUD post the Aussie CPI figures yesterday. There was no other data of note.

Coming up:

AU: Import/Export Prices: Unlikely to be market moving. Consensus sees export prices -6.7% q/q and import prices -0.8% q/q.

CH: Industrial Profits: Likely to remain weak, especially given the PPI is well in deflation. No consensus available; the prior month was -12.6% y/y.

EZ: ECB & Lagarde Presser: 25bp hike almost universally expected (markets price a 96% chance). Thereafter ECB guidance should be less definitive given the much softer than expected PMIs and greater evidence of policy taking effect as seen in the tightening of credit conditions across the Eurozone. Markets price an 88% chance of a follow up hike by December.

US: Q2 GDP/PCE & Jobless Claims: Q2 GDP is out with consensus at 1.8% quarter annualised, with upside risks given the Atlanta Fed GDP Now estimate sits at 2.4%. The GDP data will include the Core PCE deflator for Q2, while separately Jobless Claims are worth a look given the tick back lower after having trended higher recently – consensus sits at 235k.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.