Online retail sales growth slowed in May following a fairly strong April

Insight

It’s been a choppy session for US stocks, even though the news on the economy was largely positive and earnings results have been strong.

https://soundcloud.com/user-291029717/the-price-of-supply-chain-disruption?in=user-291029717/sets/the-morning-call

We’ve been broken down,To the lowest turn

Bein’ on the bottom line,Sure ain’t no fun….

The only way is up, baby.For you and me now – Yazz & the Plastic Population

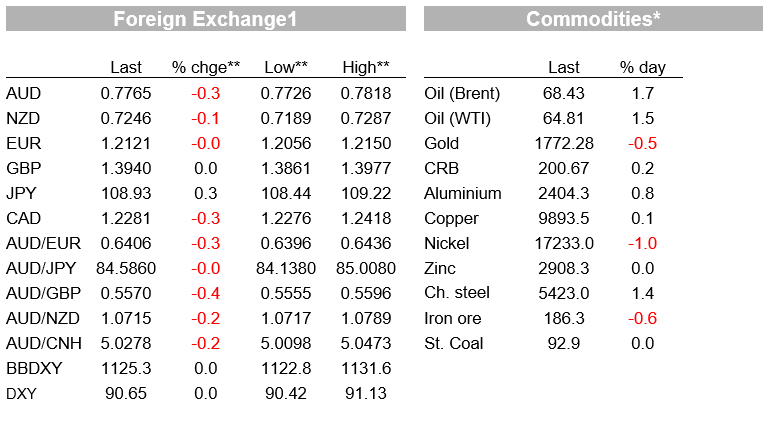

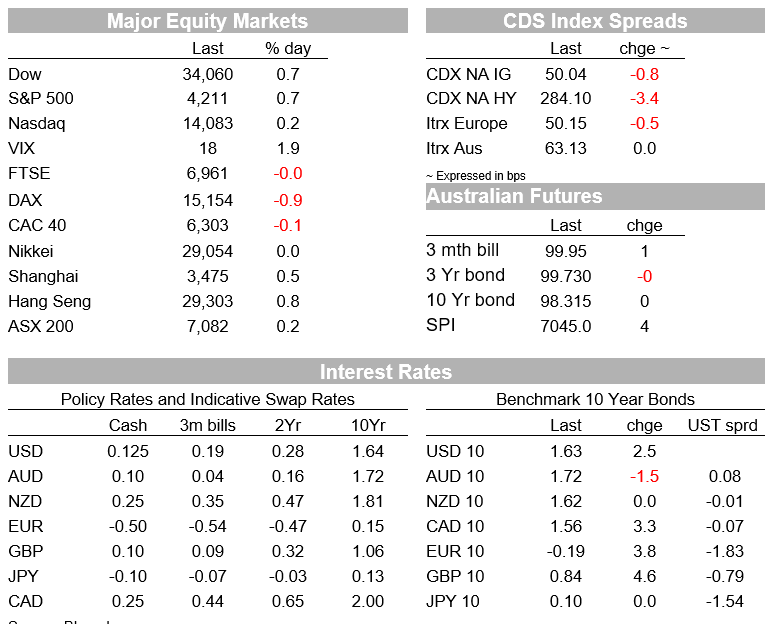

In an up, then down and up again session, US equities have closed in positive territory with the S&P 500 ending a two-day losing streak. In line with expectations, US GDP jumps in Q1 with the consumer leading the way. Longer dated UST yields edge a little bit higher while the USD has a mixed day. AUD and NZD are a tad softer, oil prices gain for a third day and copper climbs above 10000, before ending the day unchanged

Apple and Facebook reported after the bell yesterday. Both companies beat earnings expectations with their shares gaining in afterhours trading. This backdrop helped US equities open the overnight session with a positive tone, but a theme of supply shortage around the globe weighed on sentiment. Yesterday Apple and Samsung joined automakers alerting investors of production cuts and lost revenue due to chip supply constraints. Samsung, which is both a producer and user of chips, said revenue and profit at its mobile division will slide this quarter while Apple warned chip supply constraints are restraining sales of iPads and Macs.

After turning lower halfway through the session, the S&P 500 ended the day up 0.68%, the Dow closed +0.71% and the NASDAQ was +0.22. A solid Q1 US GDP print (more below) helped sentiment while most overnight earning reports beat expectations including Caterpillar, McDonald and Kraft Heinz. In Europe the 600 Index fell 0.3%, reversing early gains. Car makers (-2.6%) led the decline amid warnings over the negative impact chip shortages will have on productions. Twitter shares have fallen around 10% after the bell following disappointing sales forecast.

US Q1 GDP expanded at a 6.4% on an annualized basis following a 4.3% print in Q4-20. Personal consumption, the biggest component, surged at an annualised rate of 10.7%. Investment was also a major contributor with Non-residential investment up an annualised 9.9%, while residential investment increased at a 10.8% rate. Exports fell 1.1%, while (larger) imports rose 5.7%, resulting in 0.87% drag on GDP from net exports (adding to the US Twin Deficits dynamic). Inventories dragged 2.64% point off GDP suggesting a material payback could be in order over coming quarters though supply disruptions suggest this may not be a smooth process. Lastly government spending rose 6.3%, adding 1.12%pts to GDP and mostly at the federal level.

In what has become a common pattern in April, UST yields edged higher during our APAC (UST futures as Japan is on holidays) and then European sessions, but then eased back during the US session. The 10y rate climbed to an overnight high of 1.6860%, ending the US session at 1.6361%. The 10-year break even inflation rate stretched to almost 2.46%, a fresh eight-year high, before closing the session at 2.43%.

Copper stretched higher and broke up through the $10,000 per tonne mark before this drew out the sellers and the price fell back to $9,850. Oil prices are higher, with Brent Crude almost reaching the $69 mark again, before paring gains.

In currency markets the USD is a tad stronger in index terms (DXY and BBDX +0.05%) but mixed within G10. The move up in global yields sees USD/JPY up 0.30% with BoJ YCC policy anchoring JGBs, the pair briefly traded with a ¥109 handle and now exchanges hands at ¥108.91. Gains in oil have helped CAD (+0.28%), although NOK is unchanged while the AUD and NZD , the other two commodity linked currencies, are a tad softer. The antipodean currencies may be showing a higher degree of sensitivity to the volatility in equity markets while month-end flows are also likely kicking currencies around for no fundamental reason. For the third time in 10 days the AUD found the air thinning above the 78c mark, trading to an overnight high of 0.7818, before easing back, the pair now trades at 0.7769. Yesterday NZD rally up through 0.7285 proved to be temporary with the currency now trading down around 0.7245.

In other economic news, Euro area economic sentiment – a mix of business and consumer confidence – blasted up through expectations to reach its highest level since late 2018. While Q1 GDP figures for the region due tonight (more below) are likely to show an economic contraction, the sharp uplift in sentiment bodes well for the recovery setting in from Q2. German CPI inflation broke up through the 2% mark, but that is widely seen to be temporary, driven by one-off effects and core inflation is running much lower than that.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.