Confidence and Conditions Lift

Insight

A few hours on from Nancy Pelosi leaving Taiwan and markets have almost forgotten she ever came. Equity market have recovered their poise, a tech sector rally seeing the NASDAQ close at its highest level since 4 May.

https://soundcloud.com/user-291029717/the-quick-path-to-credible-disinflation-and-other-stories?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

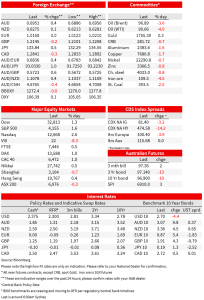

A few hours on from Nancy Pelosi leaving Taiwan and markets have almost forgotten she ever came. Equity market have recovered their poise, a tech. sector rally seeing the NASDAQ close at its highest level since 4 May (+2.6%) and the S&P 500 +1.6% . An upside surprise in the US Services ISM is partly responsible (good news is now good news it seems, and risk market have been unfazed by incoming Fed speak decrying the likelihood of Fed rate cuts next year). US bond yields are higher at the front end but – just in the last hour or so – lower further out (so deeper curve inversion). The USD had been caught between higher yields and improved risk sentiment, a combination which was unequivocally supportive for USD/JPY, up over 0.5% and one of the biggest o/n FX movers. AUD has done better given the ‘risk on’ tone to be 0.4% higher in the last 24 hours, to 0.6950.

The response from China to House of Representative speaker Nancy Pelosi – an avowed China hawk – to the unwelcome visit to Taiwan has been fairly restrained – limited so far to a ban on the export of natural sand to Taiwan (the key source ingredient for silicon chips, but hardly a ‘rare earth’) and the ban on the imports of some fruit and fish from Taiwan. Taiwan market shrugged off the news yesterday, shares in TSMC up nearly 2% yesterday and the broader market finishing just in the green.

The bigger influence on markets since Australia went home yesterday has been the US Services ISM, rising to 56.7 from 55.3 against a dip to 53.5 expected , in doing so thumbing its nose at last week’s unexpectedly large fall in the S&P Global Services PMI – a contrast that will have markets even more dismissive of the latter in coming months, after it had significant market impact at the time. Within the ISM, Business Activity and Orders led the increase, Activity up to 59.9 from 56.1 and New Orders strong at 59.9 from 55.6. Employment rose but is still sub-50 (49.9) while Prices Paid slipped (to 72.3 from 80.1 and Supplier Deliveries shortened to 57.8 from 61.9. The latter two reads offer some evidence that supply chain bottlenecks are easing up at bit, but the absolute level of prices paid is still very strong – so some signs of ‘disinflation’ not ‘deflation’ here.

On the subject of disinflation, St. Louis Fed President Jams Bullard gave a thought-provoking talk on ‘Credible Disinflation’ during our morning yesterday in which he claimed that because of Fed credibility and providing they don’t adopt a ‘gradualist’ approach ot monetary policy, it is possible to bring inflation down to target without no loss of output or employment. You could sense the scepticism of the audience (mostly Wall Street economists) but you ignore Bullard at your peril; he has been the most prescient of all FOMC officials since inflation shot up during the pandemic.

Other incoming Fed speak continues to undermine last week’s post FOMC bond market rally. After San Francisco Fed President Mary Daly 24 hours earlier said that the Fed was not nearly done raising rates, overnight she has said that while she favours a 50-point rate hike in September, her view of neutral is a ‘little over 3%’ (the median FOMC ‘long run dot in the June SEP is only 2.40% with 3% the top of the range). Even more pertinent she says markets are ahead of themselves on the Fed cutting rates, a sentiment echoed by Minneapolis Fed President Neal Kashkari, who says that 2023 rate cut(s) seem very unlikely. Richmond Fed President Thomas Barkin meanwhile says that the Fed can control inflation but recession could happen.

The Fed speak and Services ISM combination saw US bond yields extend Tuesday’s gains, but as of the New York close only now at the front end, with 2s currently just over 1bps up on 24 hours ago (having been +7bps earlier) at 3.06% but 10s now -4bps to 2.705%

In FX, its been a very mixed performance by G10 currencies. JPY has been the standout loser on the rally in US stocks and, earlier at least, higher US bond yields across the curve. USD/JPY has given back some of its gains coming into the NY close alongside slippage in 10-year Treasuries but is still 0.5% up on the day at Y133.90. CHF also lost ground on the risk-positive vibe, while NOK, AUD, SEK and CAD have all benefited, AUD/USD up 0.4% to around 0.6950 having spent much of yesterday’s session sub-0.69. NOK was the strongest G10 currency Wednesday, curious given oil is off 4% on higher EIA inventory data (OPEC agreed to a 100,000 barrels a day output increase but this was less than some had hoped). It has though started the APAC day losing ground.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.