Robust growth for online retail sales observed in June

Insight

Positive risk sentiment ahead of US CPI tonight.

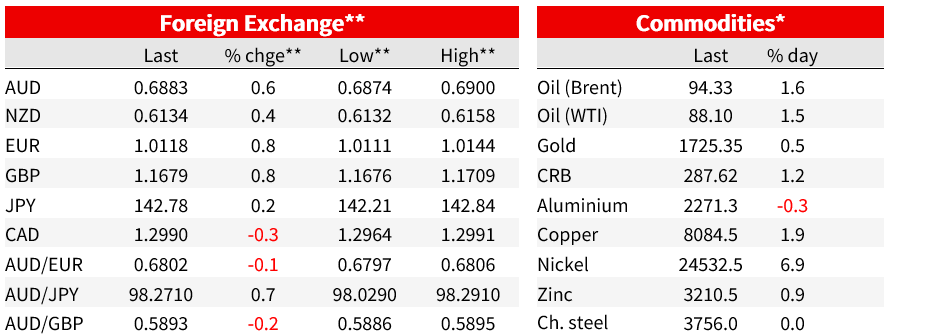

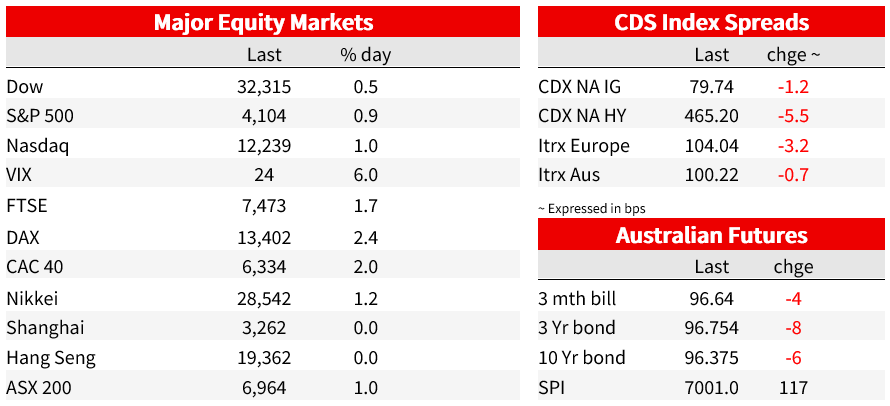

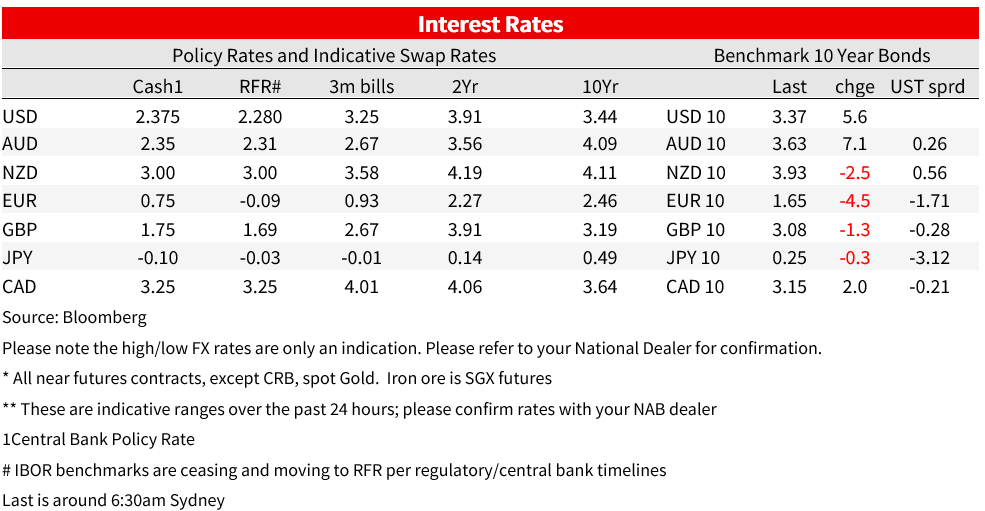

An absence of any real news has been enough to extend the recovery in risk sentiment ahead of US CPI tonight. There have been more headlines of Ukrainian forces continuing their push into Russian-occupied territory (now re-gaining more than one-tenth of areas lost to Russia according to the WSJ), while there appears to be a growing consensus that inflation has peaked in the US. A fall in the NY Fed’s inflation expectations survey likely added to that view overnight. The S&P500 rose 0.9% with equities having rallied 5.2% since their recent post-Jackson Hole trough. The USD is on the backfoot with DXY -0.6% as EUR and GBP sees some recovery, both up 0.8% to 1.0118 and 1.1679 respectively. Hawkish ECB speak by Nagel and Guindos has also helped. Yields rose in the US with bond supply weighing ahead of US CPI tomorrow; weak 3yr and 10yr Treasury auctions saw the 10yr yield up 5.6bps to 3.37%.

The inflation has peaked narrative got some more legs overnight with the NY Fed’s consumer inflation expectations falling sharply for the second month in a row. The median 1yr ahead fell to 5.7% from 6.2%, and is well down from its peak of 6.8% in June 2022, but is still well away from the pre-pandemic level of 2.5%. The median 3yr ahead also fell to 2.8% from 3.2%, well down from its peak of 4.2% in October 2021, but again is still someway off the pre-pandemic level of 2.5%. The details of the report suggest a lot of the decline is being driven by gas prices with consumers expecting gas prices to be unchanged for the year ahead, while price expectations for other commodities are still elevated. Meanwhile the WSJ had a weekend piece noting price declines amongst a number of CPI items, including airfares, hotel room rates and used cars (see Inflation Showed Signs of Easing in Several Industries in August – WSJ for details). This comes ahead of US CPI tonight where consensus is for the moderation in core to continue at 0.3% m/m, after 0.3% last month, which was well down from the 0.6-0.7 monthly pace seen earlier in the year.

US yields meanwhile rose as bond supply weighed ahead of the US CPI tonight. About 10 issuers prepared new high-grade issuance, while Treasury 3yr and 10yr auctions were weak. The $32b 10yr auction re-sale was awarded at 3.330% vs secondary trading of 3.303%. Meanwhile across the pond European yields traded lower with German 10yr -4.5bps to 1.65% amid a very positive session for European equities with the DAX up 2.4%. Ukrainian forces making gains against Russia has likely added to sentiment in Europe with some even suggesting a new tail risk that Ukraine regains sufficient territory that the war ends on Ukraine’s terms. According to the WSJ, Ukrainian forces have re-captured more than 10% of territory formally held by Russia. The probability of that is still low, but if it occurred it would be a gamechanger for financial markets. Meanwhile ECB commentary remained hawkish with Nagel and Guindos that suggested another 75bp move is possible depending on the data.

In FX the USD (DXY) fell -0.6%, extending its pullback from its 20yr high to -2.2%. Strength overnight was driven by a stronger EUR amid the hawkish comments from ECB speakers with EUR up 0.8%. GBP (+0.8%) also lifted in the environment. With risk sentiment positive and oil also higher, commodity currencies also lifted with AUD +0.6%, NZD +0.4% and USD/CAD -0.3%. The Yen though continued to underperform with USD/JPY +0.2% to 1.42.78.

Other data out included UK Monthly GDP which was on the weak side of expectations at 0.2% m/m vs. consensus of 0.3%. On a rolling 3m sense, GDP is now 0.0%, and consistent with high recession risk amid the real income squeeze. The UK NIESR GDP tracker pegs Q3 GDP at -0.1% q/q, which if realised would meet the technical definition of recession after the UK economy contracted in Q2. The real income squeeze of course is likely to be less than initially feared if the government’s proposed price cap is approved, which would see headline inflation peaking at around 10-11%, instead of the 22% plus rate expected a few weeks ago. Paradoxically, a smaller but still sizeable real income hit may mean the BoE has to remain aggressive given elevated inflation pressures. Note tonight we get labour market data and CPI on Wednesday.

Finally, a draft report on the EU’s energy plan includes a mandatory cut to power demand during selected peak hours, an “exceptional and temporary” levy on companies in oil, gas, coal and refinery industries based on their extra profits, and capping excessive revenue of companies producing power from sources other than gas via a limit on the price of the electricity generated from the likes of nuclear and renewables. The proposals will need approval by member states and there will be plenty of debate around this. A firm plan might not be agreed until October. The market remains hopeful on developments and European gas prices continue to steadily fall, with the Dutch benchmark down another 8% on the day to EUR190/Mwh, its lowest level in over a month. Meanwhile across the pond, Germany’s Ifo institute offered a sobering outlook for the German economy. It ramped up its inflation forecast, seeing 9.3% inflation next year after 8.1% this year, and a recession that sees growth of minus 0.3% next year, a classic case of stagflation.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.