Coming in for landing in a heavy cross wind

Insight

A better-than-expected US JOLT report provided rattled markets. US Treasuries led a rise in core global bond yields, equities traded lower and the USD was stronger. USD/JPY gapped lower ( official intervention?) and AUD was the notable underperformer.

Events Round-Up

NZ: QSBO domestic trading activity, Q3: -17 vs. -15 prev.

AU: Home loans value (m/m%), Aug: 2.2 vs. 0.2 exp.

AU: Building approvals (m/m%), Aug: 7.0 vs. 2.5 exp.

AU: RBA cash rate target (%), Oct: 4.1 vs. 4.1 exp.

US: JOLTS job openings (m), Aug: 9.6 vs. 8.8 exp.

I feel love in the shock of the lightning – Oasis

Markets have been rattled by yet another positive US data surprise vindicating the Fed’s mantra of “higher for longer”. A better-than-expected JOLTS report added fuel to the recent move up in core global bond yields, triggering a bear steeping of the UST curve, also lifting the USD to a fresh year to date high. USD/JPY gapped lower after climbing above 150 (official intervention?) while the AUD was a notable underperformer, not helped by an increase in risk aversion (VIX up to 20, equities down across the board) and an RBA on hold.

The JOLTS report was the data release to watch overnight, and it provided a shock to the system with markets rocked across the board . Total job openings increased to 9.61m in August from 8.92m in July, against expectations for a small decline to 8.8m declines (having fallen for six of the previous seven months). Professional and business services (+509k) were the main contributors for the increase in openings with finance and insurance (+96k), and state and local government education (+76k) playing a complementary role. The jump in job openings suggests the US labour market is easing less rapidly than implied by recent data releases, vindicating the Fed’s recent message that rates will remain higher for longer. That said, not all details in the report pointed to a strong labour market , for one the ratio of vacancies to unemployed workers moderated marginally to 1.51, from 1.53 in July. And two, the quits rate was unchanged at 2.3%, matching the lowest level since 2020, consistent with workers remaining less confident in their ability to find another job in the current market, and suggesting some evidence of skill mismatch.

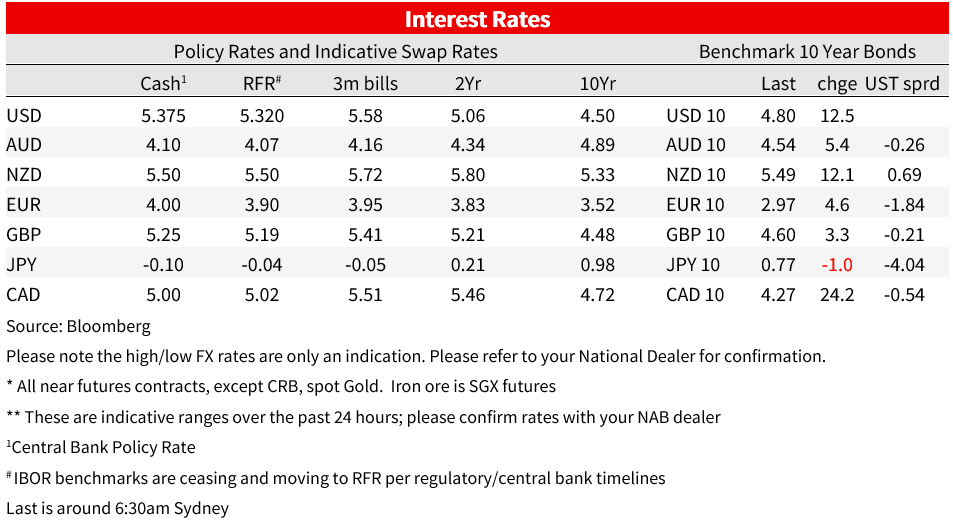

The unexpected jump in job opening added more fuel to the recent move up in core global bond yields triggering a bear steepening of the UST curve . The 10Y UST traded above 4.80% ( now at 4.78%) 12bp higher than the Sydney close and the 2Y/10Y UST curve has (again) surged steeper, breaking above -35bp for the first time in nearly a year. My colleague Ken Crompton also noted that All of the 10Y UST move was in real yields – TIPS breakevens were slightly narrower on the day. Near term Fed pricing, however, was barely touched: about 0.5bp was added to the implied rate for the end of 2023 and less than 3bp for the end of 2024.

The move up in yields was not limited to US bond yields, European yields also ticked higher, albeit in smaller magnitudes. 10y Bunds gained 4.6bps to 2.968% while 10y UK Gilts climbed 3.3bps to 4.597%. Meanwhile 10y ACGB Future climbed to 4.65%, 11bps higher relative to yesterday’s Sydney closing levels.

Speaking overnight Atlanta Fed President Bostic said “I am not in a hurry to raise, but I am not in a hurry to reduce either…I want us to hold. I think that’s the appropriate thing to do, for a long time”. By indicating that he only sees one rate cut next year, towards the end of the year, he sits more hawkish than the median FOMC member who sees two cuts next year as appropriate.

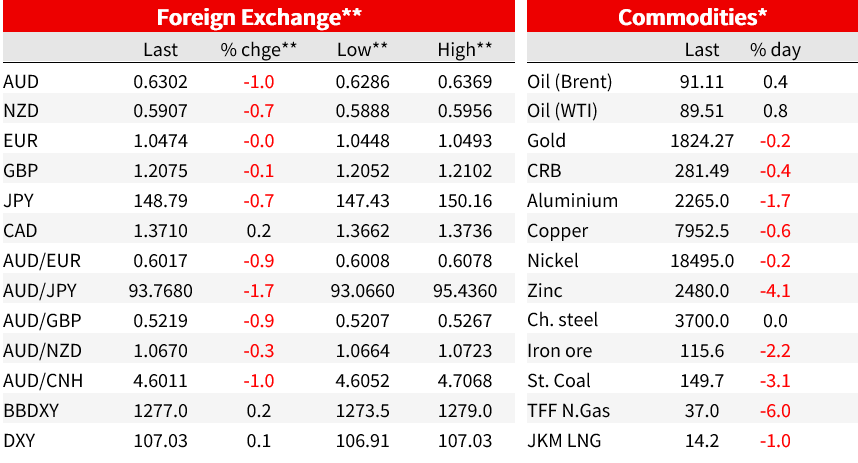

The move up in UST yields boosted the USD across the board with DXY printing a new YTD high (107.348) after the JOLTs report, before easing to 107.002, up to just 0.11% over the past 24 hours. One big factor preventing USD strength was JPY with modest lower moves seen in EUR and GBP. After the JOLTS report release, USD/JPY climbed above 150 with the move triggering a quick collapse down to 147.43, before settling just below 149. Japan’s MoF wouldn’t comment whether it intervened, but simply calling banks to check out prices might have been enough to trigger the market volatility.

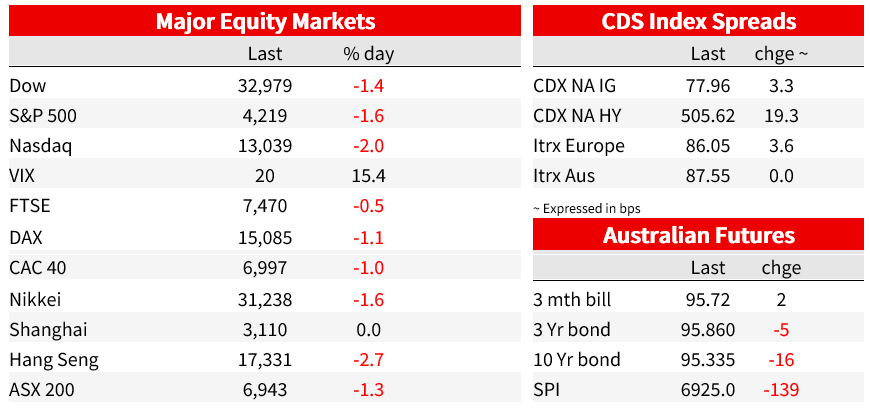

The AUD is one of the notable underperformers over the past 24 hours with a combination of risk aversion and RBA on hold not helping the pair . After the JOLTS report, the aussie traded to a new year to date low of 0.6286, before recovering into the NY close and now starts the new day at 0.6303. Equity markets have remained sensitive to the move up in core global bond yields with both European and US main indices down on the day. The EurStoxx 600 closed 1.1% lower while all EU regional indices also closed in the red. Meanwhile in the US, the S&P 500 fell 1.4% to a four-month low while the Nasdaq 100 index dropped 1.87% and the VIX index climbed above 20 for the first time since May.

The AUD was also note helped by yesterday’s RBA decision to stand pat . Although the RBA was widely expected to remain unchanged, the Bank had the ammunition to sound a bit more hawkish, given stronger than expected service inflation evident in the monthly August CPI and dire productivity reading in the national accounts for Q2, both which would have been new information over the past month. The Bank, instead, chose to deliver a message that that was little changed from the previous month. The AUD traded lower post the RBA announcement, with the front end of the ACGB curve adjusting a little lower while pricing for November fell from 13bp to 9bp of hikes and the peak rate in May-24 down from 4.38% to 4.33%.

The NZD is down 0.9% from this time yesterday to around 0.59, extending the fall seen during NZ trading hours, with sub 0.5890 levels tested a few times overnight. The RBNZ has its policy meeting today, but our BNZ colleagues see little chance of a hike ahead of the election ( see more below).

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.