We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Jump in US jobless claims provides hope US labour market may be cooling while Challenger layoff data suggests there is more weakness ahead Softer US data triggers rally in UST and weakens the USD. AUD struggles to perform as US equities tumble with bank stocks leading the decline.

NZ: Card spending (m/m%), Feb: -1.7 vs. 3.3 prev.

CH: CPI (y/y%), Feb: 1.0 vs. 1.9 exp.

CH: PPI (y/y%), Feb: -1.4 vs. -1.3 exp.

US: Initial jobless claims (k), 4-Mar: 211 vs. 195 exp.

It might be too early to call a change in the US labour market’s fortunes, but price action overnight highlights the degree of sensitivity on current US economic conditions. US Jobless claims surprised overnight jumping by more than expected, bad weather was the likely main contributor, but Challenger layoff data also released overnight suggests there is more weakness ahead. The data triggered a rally in US Treasuries with the move lower in yields led by the front end of the curve. The USD is weaker across the board with JPY, ahead of the BoJ meeting today, leading the gains against the greenback. AUD and NZD have recorded modest gains limited by the increase in risk aversion. US equities accelerate their decline into the close.

US weekly claims finally jumped after 7-weeks below 200k to 211k in the week to 25 Feb from 190k and a 195k forecasts. This represents the biggest jump since November, that said it is too early to suggest we are now seeing a change in the trend, with the 4 week moving average in claims (i.e., claims through Feb) coming at 193k, same as in January, versus 221k in 22Q4.

Continuing claims, which include people who have received unemployment benefits for a week or more (a measure of how hard it is for workers to find work after losing their job), rose by the most since November 2021 . The market has been looking for an increase in claims as a harbinger the US labour market is finally starting to cool. On an adjusted basis, California and New York accounted for three quarters of the increase in claims with severe weather across the Midwest and California the likely driver behind the gains. If so the rise in claims may prove temporary, although US economists that we follow note that the number of technology employee layoffs and a pick-up in financial sector cuts should set the groundwork for a rise in claims down the road, once the usual severance pay period has worked its way through.

The Challenger and Gray series on job cut announcements for February was also released today, this series has a good leading relationship with claims and it revealed a relatively high 78k jump in layoff with the combined January/February reading at its highest level since 2009 of 181k, suggesting the level of weekly claims should rise over coming weeks/months.

The surprise jump in claims has set the stage for the February US labour market data release due out tonight (non-farm payrolls seen at 215k, unemployed unchanged at 3.4%, see more below). The market is uber sensitive to any news on the US labour market, a strong set of numbers tonight would vindicate the recent jump in Fed rate hike expectations, conversely a soft set of numbers is likely to trigger a meaningful unwind in current pricing. The market presently sees ~70% chance of a 50bps Fed hike in March with a terminal rate around 5.60%.

Reaction to the softer US labour market data overnight triggered a rally in US Treasuries with the move lower in yields led by the front end of the curve. As I type the 2-year Treasury yield is down 16bps to 4.915%, while the 10-year rate is down 7bps to 3.91%.

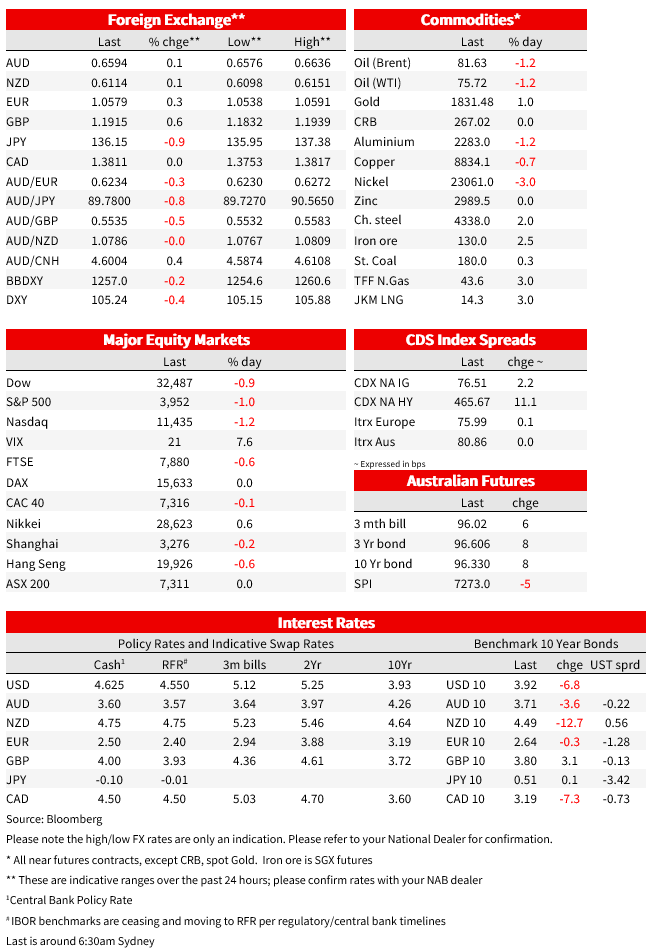

The USD was losing altitude during our trading hours yesterday, but the jump in claims and challenger data accelerated the greenback’s decline. Ahead of the BoJ meeting today, the move lower in UST yields contributed to JPY’s outperformance, up close to 1% with USD/JPY now trading at ¥136.14. GBP is also close to the top of leader board, up 0.63% to 1.194, the euro is up 0.35% to 1.0579. Speaking overnight ECB and Banque de France Governor Villeroy told France Info tv that “the peak is close, but inflation remains too high in France and in Europe.” “We will bring inflation toward 2% by the end of 2024 or beginning 2025 – that’s a commitment, not just a forecast.” He said strong food prices could last a few more months. Villeroy thinks inflation in France will start to decline from mid-2023. Last week he said it seems desirable to reach a terminal rate by summer and say be September at the latest.

AUD and NZD have only enjoyed modest gains vs the USD. AUD is up 0.1% to 0.6587, failing to sustain a move above 66c overnight (overnight high of 0.6636) while NZD is up 0.19% to 0.611, the kiwi recorded an overnight high of 0.6150. We think the turn in risk sentiment evident in the declines in US equities limited the ability of both Antipodean currencies to perform against the USD.

Somewhat uncharacteristically to what we have seen in recent weeks, where bad economic news has been deemed as good news by equity investors, reaction to the claims and Challenger data releases overnight weighed on US equities with the decline in main US equity indices accelerating into the close. The S&P 500 now trades 1.18% down on the day while the tech heavy NASDAQ is -1.59%. U S banks have been the notable underperformers with Bloomberg noting the KBW Bank Index down close 7.7%, its biggest one-day drop since June 2020. SVB Financial Group fell by a record 60% after the Silicon Valley-based lender took steps to shore up its capital position following losses in its securities portfolio. Other big bank stocks have also underperformed, with Bank of America Corp., Wells Fargo & Co. and JPMorgan Chase & Co. all sliding at least 5%. Earlier in the session the Euro Stooxx 50 close -0.005% while the FTSE 200 was -0.63%.

In other news, the Biden administration released a budget outline for fiscal year 2024 calling for increases in funding for defense, immigration, healthcare and clean energy programs . The proposal also includes an increase in tax for the wealthy that should help cut the deficit by $3trn over the next decade. Bloomberg notes the deficit in 2024 would increase from $1.6trn to $1.8trn , and the gross federal debt would swell to $51trn after a decade. The proposal sets the stage for a big battle with the Republican led House. GOP leaders have been calling for a reduction in spending, aiming for at least $150bn in cuts with no tax increases.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.