A private sector improvement to support growth

Insight

Tech stocks lead gains in US equities. NASDAQ up just under 2%.

EA: Consumer confidence, Jan: -20.9 vs. -22.0 prev.

“Technology is a useful servant but a dangerous master” – Christian Lous Lange, Historian

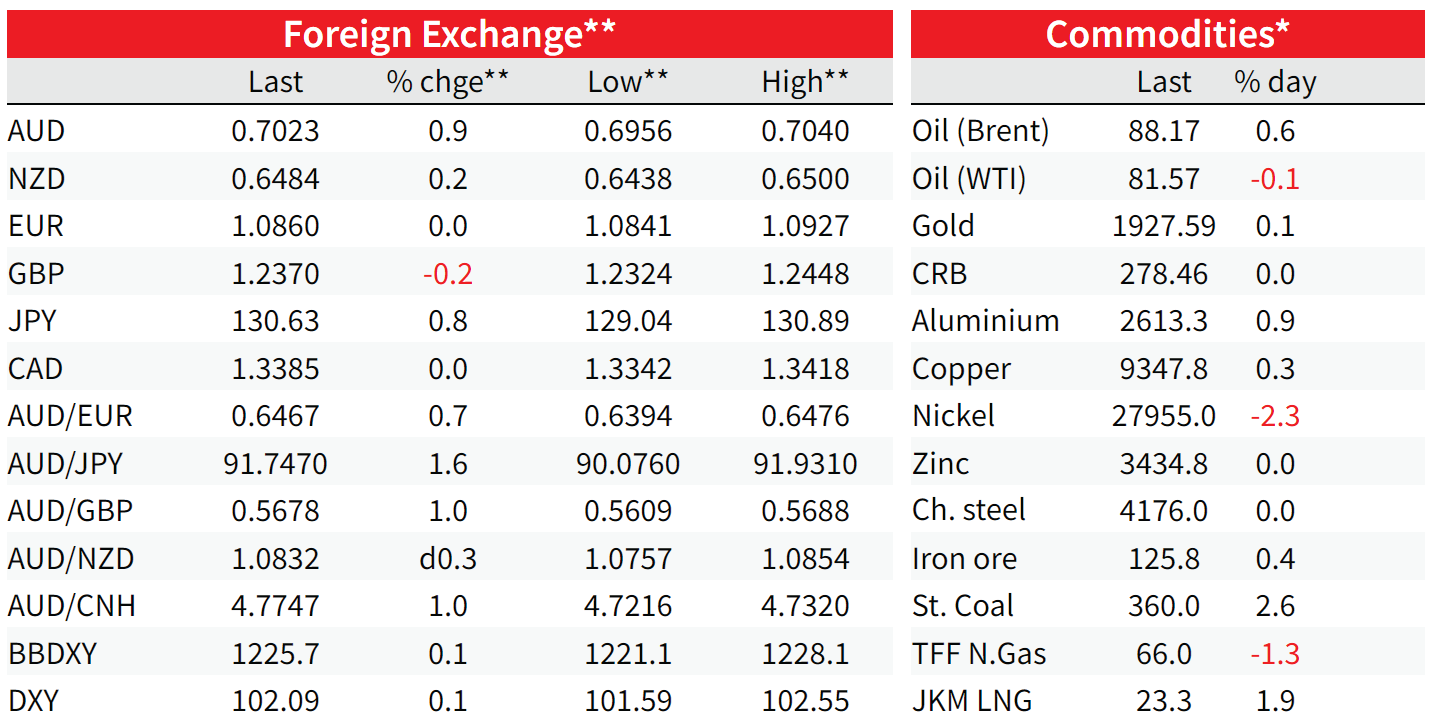

The NASDAQ is leading overnight gains within US equities as the market gears up for the tech sector to begin reporting their Q4 earnings, Microsoft is the first cab off rank after Tuesday’s closing bell. Core global bond yields are also higher with the UST curve showing a bear flattening bias as front-end bonds lead the move up in yields. The USD is little changed in index terms with the AUD (back above 70c) leading the gains within small G10 pairs, offset by JPY losses. Yesterday the BoJ loans for bonds programme was met with strong demand.

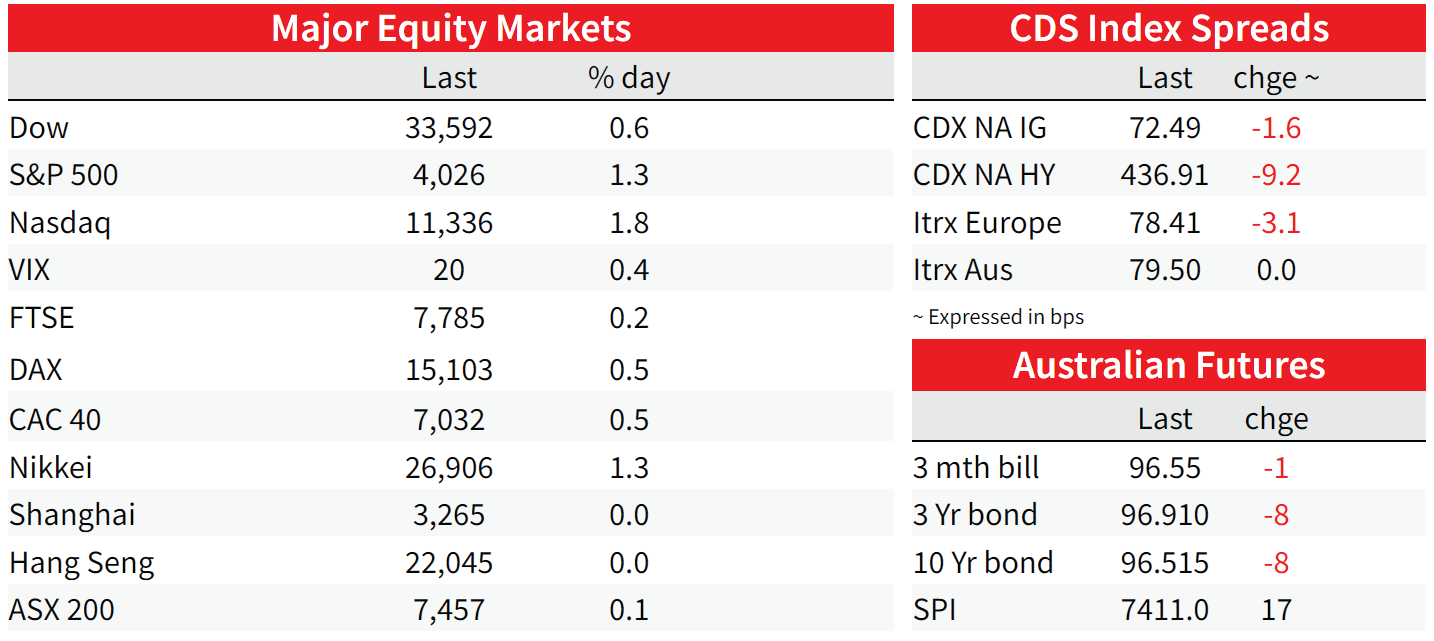

Global equities are enjoying a positive start to the new week with equities indices green across the board. After a positive lead from Asia (Nikkei +1.33, Hang Seng 1.82%) main European indices closed in the green with the Euro Stoxx 600 index 0.52% higher. Gains in technology stocks has been the main theme in the overnight price action with chip stocks from ASML to Ams-OSRAM recording some of the largest moves within Europe (Stoxx Tech Index was +2%) while in the US the NASDAQ is spearheading the gains, now trading 1.75% higher on the day.

Microsoft will be reporting its earnings after the closing bell on Tuesday, but after last week’s announcement to lay off 10k employees (~5% of its workforce), a theme seen across major tech companies, investors are now seemingly less pessimistic on US tech companies. Indeed, Spotify is the latest tech company to announce job cuts given a renewed focus on lowering cost amid diminished advertising revenue and a souring economic outlook. Spotify shares are up over 2% with Salesforce another notable gainer (up over 3%) following news that Hedge fund Elliott Investment Management had taken a substantial activist stake in the company.

The positive tech vibes have also extended to the broader market, the S&P 500 is up 1.65% as I type with all its 11 sub-indices trading in the green. The Dow is also having a good day up ~0.93%.

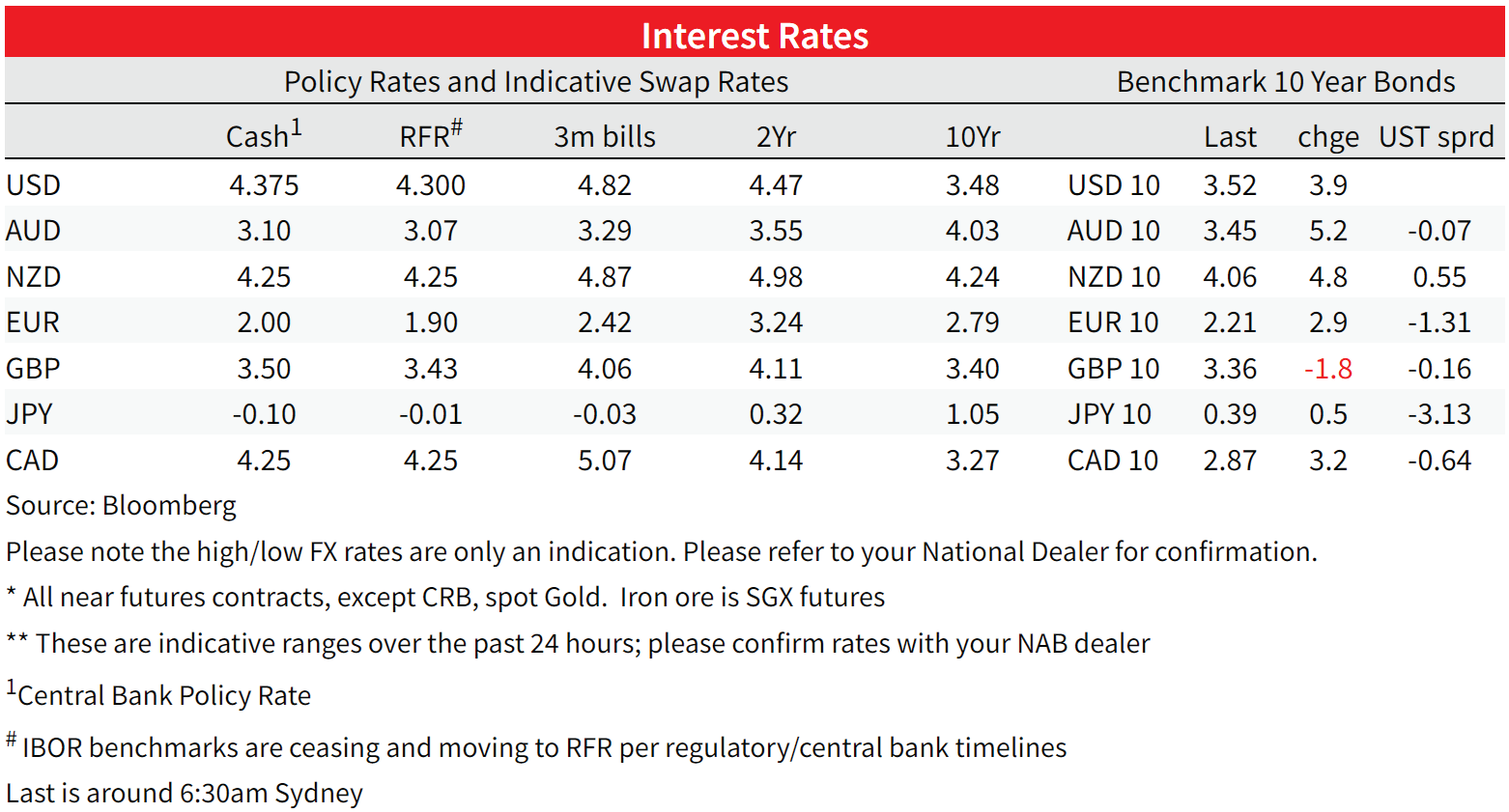

A move up in core global bond yields is another theme from the overnight price action . In Europe, Bunds closed with a mild bear-steepening bias with investors digesting another round of ECB speakers pushing back at the notion, suggested by news reports last week, that moderating inflation will soon warrant smaller interest-rate increases. Governing Council member Boris Vujcic said the institution’s guidance last month on another half-point increase in interest rates is still “reasonable” with ECB Kazimir also joining the hawkish chorus. Notbably, however, ECB Visco sounded more cautious saying the ECB has no need to err on the side of tightening and should take a measured approach to raising interest rates.

For now, it seems that another 50bps hikes on February 2 should be treated as the base case (49bps currently priced by overnight index swaps), but thereafter a more robust debate looks set to ensue with a shift down towards 25bps hikes an increasingly more probable outcome for the March 16 meeting.

Meanwhile front-end yields have led the move up in the UST curve with the 2y tenor up 6bps to 4.25%. The 10y Note is up 4.5bps and now trades at 3.52%, about 20bps higher than last week’s low driven by short-covering post the BoJ’s lack of policy action. Traders are focused on the increased supply this week, with some $120b of new 2s, 5s and 7s being issued and $20-25b of new investment grade corporate bond issuance on the cards this week.

Moving onto FX land, the USD is little changed in index terms, but we have seen some decent moves within G 10 pairs. The AUD is the top performer over the past 24, up just over 1% and now comfortably above 70c. The aussie traded to an overnight high of 0.7040 and now starts the new day at 0.7023, true to form the positive equity vibes have favoured the pro-growth /risk sensitive AUD.

The Kiwi has also made some gains against the USD (+0.3%) with some evident resistance around 0.65 and currently marginally higher from last week’s close at 0.6475. SEK (0.51%) and NOK (0.69%) were the other notable gainers.

JPY weakness was the offsetting USD force with USD/JPY climbing 0.75% to ¥130.678 . Move up in core global bond yields has been one factor weighing on the yen with short covering after last week’s BoJ’s lack of policy action an additional contributing factor. Of note too, yesterday the BoJ regained some control of the yield curve through its extraordinary loan operations, which saw demand of just over 3 trillion yen for the 1 trillion yen of 5-year loans on offer. The loans are effectively an offer for commercial banks to borrow cheap money to buy JGBs.

Looking at commodities, oil prices are up just over 1% with Lunar New Year festivities in China seen as boosting demand while Russian exports come under pressure given insurance difficulties from sanctions. Copper is the other notable performer, not gaining too much on the day (0.20%) but staying close to a 7 month high.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.