Coming in for landing in a heavy cross wind

Insight

No surprises from the FOMC in its formal policy pronouncement, the Fed announcing a November start to the QE tapering process at the as-expected pace of $15bn per month.

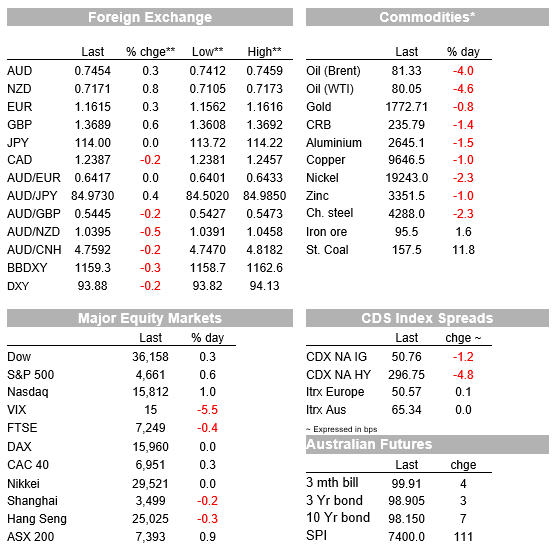

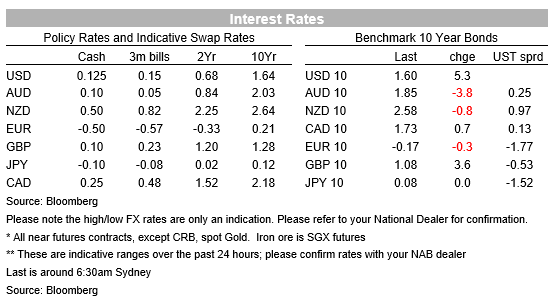

No surprises from the FOMC in its formal policy pronouncement now a couple of hours old, the Fed announcing a November start to the QE tapering process at the as-expected pace of $15bn per month (split $10bn for Treasuries and $5bn for Agencies) and to proceed at this clip – the next one in December – to end mid-2022, but with the Fed giving itself the option of altering the future pace of tapering contingent on the prevailing economic outlook. Following the Statement and now the Fed press conference, US stocks added more than 0.5% to pre-Fed levels with the S&P closing at another record high (+0.65% on the day). This is even though the US yield curve has bear-steepened, with 2s up 1.2bp and 10s a bigger 5bps to 1.60%. the USD is slightly softer, the DXY index now at 93.90 from just above 94.0 pre-Fed, helping AUD/USD lift back to ~0.7450 from an overnight low of 0.7413.

One key change to the FOMC statement was a rephrasing of the inflation picture, now saying that elevated inflation reflects factors that are “expected to be” transitory. The previous statement was more definite that elevated inflation was “largely reflecting transitory factors” This was a signal of less confidence in the inflation outlook, conceding that high inflation might be prolonged. Indeed, the ensuing press conference, Chair Powell admitted that the Fed took a ‘step back’ from transitory, noting only that we should see inflation move down by ‘Q2 or Q3’. As for the maximum employment half of the Fed’s mandate, Powell says this could be achieved by mid-2022, in doing so doing absolutely nothing to push back against market pricing which currently sees Fed lift-off’ commencing as early as July 2022 and with another rate rise priced by year-end.

Overall, despite the shift in tone, Powell proves he is no different to other central banker in talking about both sides of his mouth/giving something to everyone, saying the Fed “We’ll be patient, but we won’t hesitate” (to raise rates as needed).

Pre-Fed, US data prints overnight were stronger than expected. The ISM services index unexpectedly surged to a fresh record high of 66.7, with business activity and new orders up to record highs. With daily covid case levels falling quite sharply of late, US consumers seem ready to go out and dispose of the savings accumulated while the economy was in the grip of the pandemic and the government was raining down cash on households. Order backlogs, supplier delivery times and prices paid remained a feature of the survey, reaching new highs. ADP private payrolls rose by 571k in October, which might lead to some upward revisions to non-farm payrolls estimates for Friday relative to the pre-ADP consensus of 450k.

In other central bank news, the Central Bank of Poland, following the playbook written by Chile’s central bank, shocked the market again, delivering a 75bps hike in its policy rate to 1.25%, the largest hike in its history and Governor Glapinski saying “we will do whatever it takes to bring inflation back to target in the medium term”. This continues the theme of some central banks – mainly the smaller developed ones and in emerging markets – getting a move-on to reduce unnecessary policy stimulus. In sharp contrast, other notable central bank speak overnight came from ECB President Lagarde has been out saying that ‘2020 is “off the chart” in respect of interest rate rises. It seems she has just got the memo that described her push back against 2022 tightening in last week’s press conference as ‘half-hearted’.

Elsewhere and while everyone was busy been listening to Powell, oil prices have been falling quickly. Another sizeable weekly rise in US crude inventories is part of the explanation (EIA data shows a build of 3.29mn against 2.25mn expected), but now augmented by news that nuclear talks with Iran are set to resume on November 29, including the EU, China, France, Germany, Russia and the U.K. WTI crude is currently down about $4 and Brent $3.50 (both down more than $1 on the Iran news).

The US Treasury announced the first reduction in quarterly auctions of longer-term debt in more than five years, reflecting reduced borrowing needs as pandemic-related stimulus diminishes. This comes at an opportune time, as the Fed tapers its bond purchases, reducing the impact of this policy action on the market. Treasury will auction $120b of long-term securities next week, a reduction of $6b from the recent record levels.

Finally, the spread of COVID19 across China is worsening, with more than 600 community cases now tallied in over half of the 31 Provinces in the latest outbreak. We see the government’s elimination strategy as significantly reducing domestic demand as lockdowns become more widespread and this a key risk factor to watch for the global economy.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.