Online retail sales growth slowed in May following a fairly strong April

Insight

US yields are higher and the dollar stronger in a modest and reversal of some of last week’s post CPI moves as Fed speakers remain stubborn that rates will continue to go higher to get to a level that is sufficiently restrictive.

US yields are higher and the dollar stronger in a modest and reversal of some of last week’s post‑CPI moves as Fed speakers remain stubborn that rates will continue to go higher to get to a level that is sufficiently restrictive. Of most note among Fed speakers overnight, Bullard presented analysis showing 5-5.25% as the minimum level where rates might be ‘sufficiently restrictive.’ US yields were around 10bp higher. The UK Autumn Statement outlined tax increases and spending cuts, but most of the announced hit after the expected general election in 2024.

St Louis Fed’s Bullard presented analysis using various versions of a Taylor Rule showing the Fed funds rate would need to move to 5-7% to get inflation back down. Bullard said, “for now I’d be happy to get to the minimal level [of 5-5.25%] and that’s why I think the committee is going to have to do more.” But added that “it’s easy to make arguments that before this is all over you’d have to go to much higher levels of the policy rate. ” The lower end 5-5.25% of what might constitute ‘sufficiently restrictive’ policy is based on ‘generous assumptions that tend to favor a more dovish policy’ (a real neutral rate of -0.5%, trimmed mean PCE, and a slightly less reactiveness to deviations from target). A ‘less generous’ rule puts the ‘sufficiently restrictive’ levels around 7% (A +0.5% real neutral rate, core PCE inflation, and a more standard levels of policymaker reactiveness). (Bullard’s presentation is here: Getting into the Zone (stlouisfed.org)). Despite looking for higher policy rates, Bullard’s base case remains slower growth, but no recession and he told reporters he would look to Powell to set the direction on whether 50 or 75bp is appropriate in December. Speaking in the past couple of hours, Minneapolis Fed’s Kaskari said he’s not seeing much evidence of underlying demand cooling and is hesitant to predict when to stop raising rates.

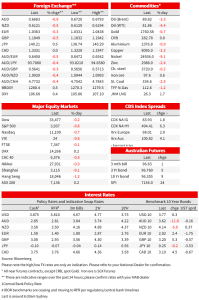

The continued stubbornly hawkish messaging made a bit of a dent overnight following the move lower in yields after the relief on one month of downside surprise in CPI data last week. The US 2yr yield was 10bp higher to 4.45% but still 14bp lower than it was prior to last week’s CPI data. Yields were higher across the US curve. The 10yr retracing its move lower yesterday, up 9bp to 3.78% meaning the 2s10s spread held onto yesterday’s dive further into inversion at 67.8bp.

Only second tier US data on the calendar, though initial jobless claims fell 4k to 222k last week, continuing to demonstrate a strong labour market. For the manufacturing sector, though, the Philly Fed business survey was weaker than expected, falling nearly 11 pts to minus 19.4 with the employment index falling 21pts to 7.1. Housing starts and permits continued to trend lower, down 4.2% m/m and 2.4% m/m respectively.

Equity markets were generally lower. The S&P500 is around 0.6% lower, after paring steeper losses earlier in the day. Declines were led by utilities and consumer discretionary. The Nasdaq is currently 0.7% lower. The Euro Stoxx 50 and FTSE 100 were little changed, down 0.1%. Oil prices were lower, with Brent down 3.3% and dipping below $90/bb to a six-week low of 89.82.

In currency markets the USD is broadly stronger, up 0.4% on the DXY to 106.86 from an intraday high above 107. Gains came across all G10 currencies, though the CAD was little changed. The AUD was 0.9% lower at 0.6683. The AUD got to an intraday low of 0.6634 before recovering a little alongside a broader pullback in the dollar and as equities pared losses across the US session. The euro was 0.3% lower.

The UK Autumn statement included plans £30bn of spending cuts and £25bn of tax rises . The FT highlights the contrast: while former chancellor Kwasi Kwarteng’s September ‘mini’ budget was the largest tax-cutting plan for 50 years, Thursday’s statement was the biggest tax-raising effort for 30 years other than during the pandemic. Much of the consolidation is not slated until 2024-25, when the economy is forecast to be back to growth. The net effect of policy announcements in the current and next fiscal years is a very small positive though freezing national insurance thresholds for businesses will take effect from April 2023 and raise £5.8bn by 2028 and an extended windfall tax on energy companies is set to raise £14bn next year. Chancellor Hunt said “w e need fiscal and monetary policy to work together. That means the government and the bank working in lockstep.” The OBR forecast growth at -1.4% next year before activity regained pre-pandemic levels in late 2024, inflation at 7.4% next year.

In terms of the market reaction, UK 10yr yields initially fell nearly 10bp to 3.12%, before moving as high as 3.26% as markets digested the package, but now sit at 3.20%, 5bp higher on the day and partially retracing some of yesterday’s fall. The German 10yr bond was 2bp higher to 2.02%.

In Australia, employment growth beat expectations at 32.2k in October (consensus 15.0k) and the unemployment rate fell one tenth to 3.4% from 3.5% (consensus 3.5%). The strong outcome bucks the trend slowing in employment growth over recent months, which had been difficult to square with still very elevated labour demand. In the context of the strong WPI print yesterday, the case for 25bp hikes in December, February and March, as is NAB’s call, looks even firmer. Despite updates this week showing the RBA considered 50bp in November when it raised 25bp, a strong labour market and more sharply accelerating wages growth, markets price around 20bp points for December, in line with where it was on Monday, and 52bp of hikes over the next three meetings.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.