Confidence and Conditions Lift

Insight

Trio of strong data with US Retail, US Industrial Production, and UK Jobs all beating

https://soundcloud.com/user-291029717/tills-ring-in-the-usa-jobs-bounce-back-in-the-uk?in=user-291029717/sets/the-morning-call

Overview A Sky Full of Stars

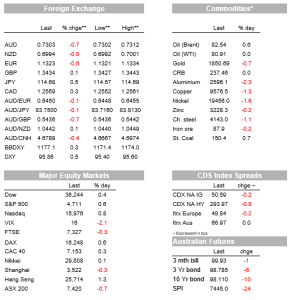

A trio of strong data overnight added to risk sentiment (S&P500 +0.6%) and to USD outperformance (DXY +0.5%). Notable within the beats was Retail Sales Core Control +1.6% m/m (consensus 0.9%), suggesting consumers are not as pessimistic as the University of Michigan report portrayed. Earnings by Walmart and Home Depot also added to the tone and suggests the strength seen in October continued into November. GBP (+0.5%) also came along for the ride with UK labour market data showing little impact from the end of the furlough scheme, firming up the prospects of a BoE December rate hike so long as the BoE doesn’t bottle it again. Despite the positivity, rates markets traded in a tight range (US 10yr +1.6bps to 1.63%). Finally, Fed speak was hawkish as Bullard (2022 voter) argued the fed should “take in a more hawkish direction ”, while eminent financial journalist Martin Wolf added his voice to the hawkish argument, “a faster shift towards monetary sobriety now could prevent having to go cold turkey later on”.

First to the US Retail Sales beat. Headline retail sales rose 1.7% m/m against 1.4% expected, alongside a modest revision to prior data. The core measure of retail was even stronger relative to consensus at 1.6% m/m against 0.9% expected. It is notable that amongst the core group there was broad strength amongst the retail categories indicating strength in discretionary spending in the lead up to Christmas. It’s fair to say doubts had crept into the US growth narrative in Q4 after the run of weak University of Michigan Consumer Sentiment reports, but today’s data suggests consumers are not as pessimistic as that report suggests. In an encouraging sign for the outlook, Home Depot noted it fiscal fourth-quarter sales were already tracking higher than last quarter, pointing to a strong finish to 2021.

Profit reports from Home Depot and Walmart also contained other important anecdotes. Inventory levels at Walmart had increased 11.5% in the quarter in preparation for the holiday season amid strained supply chains (which in turn would have added to strained supply chains!). The extent of the rise in inventories is notable, with the CFO stating “three years ago, if we would have said our inventory is up 11% I would not have been very happy”. Walmart also report workers had flowed back into employment with the company back to being fully staffed. Walmart attributed the flow back to “ when the stimulus dollars started to go away, the hiring situation changed….we saw people come back in a matter of weeks. We were back to being staffed”. In some signs that supply chain issues may be starting to abate (as indicated in shipping costs that appear to have peaked), sneaker firm On said all its production factories have been open since early November.

Other US data was also strong with US industrial production in October, up 1.6% m/m, with a strong 11% bounce-back in auto production despite the concerns about supply of global semi-conductors. Even excluding this sector, the increase in production was a healthy 0.6%, with manufacturers overcoming shortages of raw materials and labour constraints. It’s worth noting that a strong rebound was inevitable after Hurricane disruption and the level of manufacturing output is back above its pre-pandemic levels. Home Building Sentiment also surprised to the upside with the NAHB index at 83.0 against 80 expected.

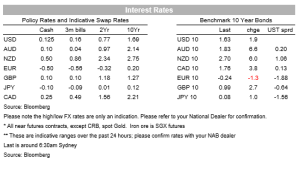

Across the pond UK labour data showed little impact from the end of the furlough scheme in September, which should reinforce the case for rate hikes from the BoE. Payroll employment actually rose 160k, with little sign that the 1.1m people on the scheme were added to the ranks of the unemployed. BoE Governor Bailey had earlier alluding to the uncertainty around the employment situation after the end of the furlough scheme as a key consideration in why the BoE didn’t hike. Markets fully price a December rate hike and 100bps of tightening is priced through to August 2022. Another labour market update is due a couple of days ahead of the December meeting, and inflation data will also be important.

Fed speak was hawkish, but had little market impact. The Fed’s Bullard (voter 2022) argued the Fed should “tack in a more hawkish direction” in the next couple of meetings “so we are managing the risk of inflation appropriately ”. As for what the FOMC could do, Bullard argued for a faster tapering profile to end by March, with markets likely watchful for weather his fellow FOMC colleagues agree in the lead up to the December FOMC meeting. Bullard also made the suggestion of actively selling down its balance sheet, while his views on rates are well known having pencilled in two hikes in 2022. The financial journalists also appear to be jumping on the ‘Fed should raise rates to avoid an inflation breakout’ bandwagon. Martin Wolf in today’s FT is one of those who nots the Fed should scrap its average inflation target and move towards normalisation. His fear is the risks around inflation are to the upside and it may turn out far worse than expected, with the Fed compelled to play catch-up, with the costs of that catch-up vastly exceeding the benefits of the current ultra-loose policy (worth a read: FT: Fed policy must adjust for inflation).

US Treasuries have taken the data and Fed commentary in their stride. The 10-year rate has traded a tight 4bps range for the day, after yesterday’s selloff, and is currently barely higher at 1.63%, with rates across the curve showing the same increase of about 1-2bp. Against a modest fall in key European 10-year rates, the 2bps lift in the UK 10 year and 4bps rise in its 2-year rate stand out, consistent with the market seeing the strong UK labour market data as supporting tighter monetary policy. The economic releases have driven the USD and GBP higher overnight. The key USD indices are up 0.3-0.5% for the day, keeping their upward trend since June intact and sending them to fresh highs for the year. For now, the US economy’s relative outperformance, given the supercharged policy backdrop, remains a force to be reckoned with, even if the longer term consequences of over stimulating the economy are foreboding.

Against a backdrop of a stronger USD, the NZD and AUD show notable overnight falls. The NZD is down 0.7% to just below the 0.70 mark, a similar level it found support last week, but ultimately unlikely to hold for too much longer, given strong USD momentum. The AUD is also down 0.7% to near 0.7300. GBP is the only major to hold up against the strong USD, relatively steady at 1.3430, EUR is down to a fresh 16-month low of 1.1325, while USD/JPY is up to 114.60, just shy of its October high.

Closer to home, the RBA Minutes and a speech by Governor Lowe yesterday again saw the Governor push back on market pricing for interest rate rises in 2022, with Governor Lowe explicitly stating “the latest data and forecasts do not warrant an increase in the cash rate in 2022”. The key to the Governor’s view is that wages growth in excess of 3% is needed to sustain inflation at the mid-point of the 2-3% target. The RBA continues to forecast only a gradual increase in wages and inflation in Australia in part related to “inertia in wage-setting practices”. It’s fair to say markets either do not believe the RBA’s central forecast scenarios and/or reaction function. Markets still fully price the first rate rise by July 2022, with a follow up hike by September. NAB’s view is that the RBA will raise rates from mid-2023 with a relatively aggressive series of hikes thereafter to bring the cash rate to 1.75-2.0% by the end of 2024.

Asked in Q&A where neutral was, Governor Lowe hoped that neutral had a real positive rate and included a 1% productivity assumption, implying neutral for him was somewhere between 3-4%. This looks too high for us, especially in the context of higher household debt with neutral likely closer to 2.0% in NAB’s view. It is also worth noting here the Governor’s observation that market pricing is only for a modest rise in policy interest rates globally which is “consistent with the view that the current increase in inflation is only transitory and that a period of contractionary monetary policy will not be required ”, which would indicate a low global neutral rate. NAB also expects QE to end in February 2022 with little use for the program given other central banks will have ended or tapered their programs by then and the rebound in activity and employment from the current lockdowns is likely to be clear by the February meeting.

A big day domestically with the Q3 Wages print dominating domestically. Offshore focus will be on the UK’s inflation figures and whether that affirms a December rate hike, then onto the US where there are no less than seven Fed speakers. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.