Coming in for landing in a heavy cross wind

Insight

The US economy has started 2023 from a stronger position that many of us had expected and when looking at the Fed’s new preferred inflation reading that tries to exclude much of the noise in the data, the story doesn’t change.

Events Round-Up

JN: CPI (y/y%), Jan: 4.3 vs. 4.3 exp.

JN: CPI x fr. food, energy (y/y%), Jan: 3.2 vs. 3.3 exp.

US: Personal income, Jan: 0.6 vs. 1.0 exp.

US: Real personal spending, Jan: 1.1 vs. 1.1 exp.

US: PCE core deflator (m/m%), Jan: 0.6 vs. 0.4 exp.

US: PCE core deflator (y/y%), Jan: 4.7 vs. 4.3 exp.

US: New home sales (k), Jan: 670 vs. 620 exp.

US: U. of Mich. con sent, Feb: 67.0 vs. 66.4 exp

Markets were yet again rattled by a round of solid US data releases with the Fed’s preferred measure of inflation shooting the lights out against a backdrop of a surge in consumer spending. The data depicted a US economy running too hot at the start of the year, increasing the urgency for the Fed to do more tightening over coming months. A repricing rate hike expectations was not limited to the Fed, ECB rate hike expectations also ratcheted up triggering a global bond sell off led by a rise in front end yields and flattening yield curves. European and US equity markets ended the week in a sea of red with the S&P 500 recording its worst week in two months. The USD was stronger across the board with JPY and AUD the big underperformers with NZD not too far behind. AUD starts the new week 0.6733, NDZ at 0.6165.

Following recent data revealing a stronger than expected US labour market and solid retail sales in January, the market was brazing for a round solid US data releases on Friday. But the degree of strength was bigger than anticipated, real personal spending rose 1.1% m/m, that was the strongest monthly gain since the pandemic government’s handout month of April 2021. Then, the accompanying inflation report also printed higher than expected, the core PCE deflator jumped 0.6%mom sa , it highest reading since July 2022. The annual increase was 4.7%, that was four-tenths ahead of market expectations as the data showed upward revisions.

While there are some caveats that should downplay somewhat the strength of the data, such as seasonality and warm weather alongside one off jump in wages at the start of the year, plus volatility on the financial services, professional services, and healthcare monthly readings. Overall, the reality is that the US economy has started 2023 from a stronger position that many of us had expected and when we look at the Fed’s new preferred inflation reading that tries to exclude much of the noise in the data, the story doesn’t change. The PCE services ex-energy, rose 0.58%, the biggest increase since November 2021, service inflation is sticky and there is no clear evidence of a nascent downtrend. Thus, the conclusion must be that the US economy is running hot and there is a need/urgency for the Fed to do more.

Just to add insult to injury, is worth noting too that other US data releases also beat expectations. New home sales jumped over 7% m/m in January to their highest level in nearly a year, one of the few housing market indicators showing any signs life and then the University of Michigan preliminary February reading for Consumer Sentiment came at 67 vs 66.4 expected while one year ahead inflation expectations jumped to 4.1% this month, from 3.9% in January but 4.4% in December.

Unsurprisingly, reaction to the US data triggered an uptick in Fed rate hikes expectations over coming months. Cumulatively the market now sees 82bps of hikes prices over coming months, suggesting three full 25bps hikes and a chance of a fourth, early in the second half. The Fed terminal rate is now seen at 5.40% with rate cut expectations by December 2023 reduced to 12bps to a funds rate of 5.28%, on Thursday that number was 5.17%.

Reinforcing this thinking, Fed speakers remained forthrightly hawkish. Speaking after the data releases, St Louis Fed President Bullard hawkish credentials remain undeterred, calling for 50bps clips and stressing the need to “move quickly now, re-establish credibility now”. Boston Fed President Collins anticipated “further rate increases to reach a sufficiently restrictive level, and then holding there for some, perhaps extended, time”. Cleveland Fed President Mester was asked whether she favoured stepping up to a 50bps hike at the next meeting said “where we’re going is more important than what we tactically do at any one meeting”.

Notably too, the strong Core US PCE print triggered a reassessment of ECB rate hike expectations. The market now sees a deposit rate peaking at 3.747% by the October meeting, that was a 10bps jump from pricing seen at the end of Thursday.

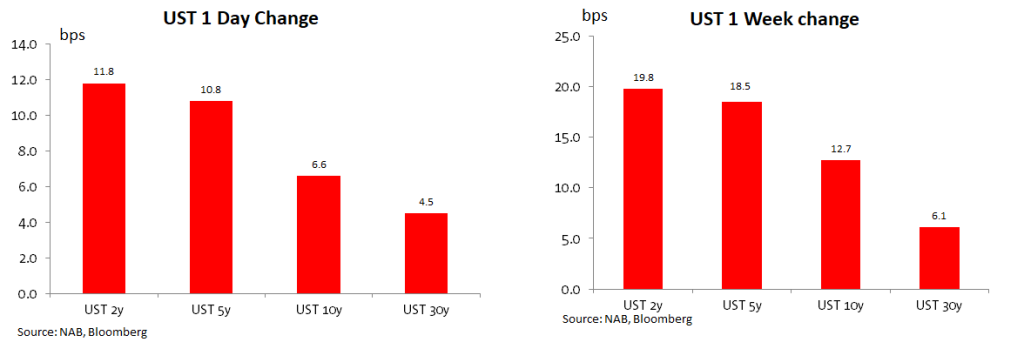

The repricing of Fed and ECB rate hike expectations triggered a sell-off in core global bonds with the move up in yields led by front end tenors, flattening yield curves . In the US, the 2y UST yield reached a high of 4.836%, highest level since 2007, the benchmark yield closed the week at 4.814%, up 12bps on the day. Meanwhile the 10y Note found support just below the 4% mark (double top at 3.978%), and ended the week at 3.94%, up 6.6bps on the day with the 2s10s curve, 5bps flatter at -87 bps. Meanwhile in Europe, Germany’s 2-year rate rose above 3% for the first time since 2008, closing up 12bps to 3.03% while the 10y rate gained 9.7bps to 2.532%.

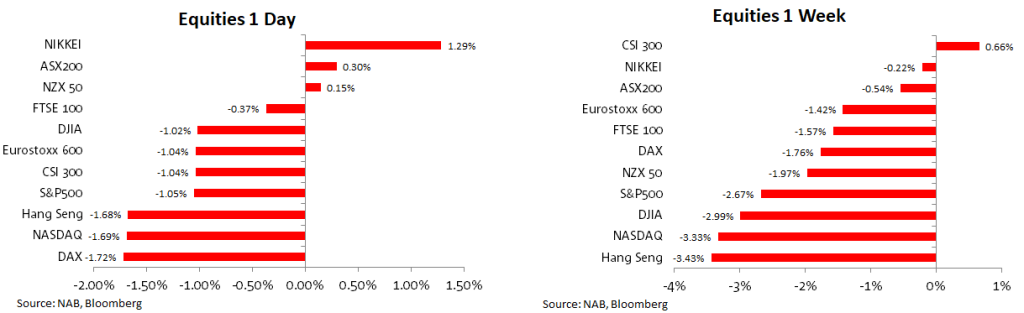

Prospect of higher cash rates dented equity sentiment with the US and European equity board a sea of red. In the US, the S&P 500 fell over 1% on Friday, extending the week decline to 2.7%, that was the worst weekly return in two months . The tech heavy NASDAQ fell 1.69% on Friday, losing 3.33% on the week. In Europe the Eurostoxx 600 fell 1.04% on Friday and 1.42% on the week. Of note, China’s CSI 300 was the only main equity market that managed to record a positive return for the week, up 0.66% over the past 5 working days.

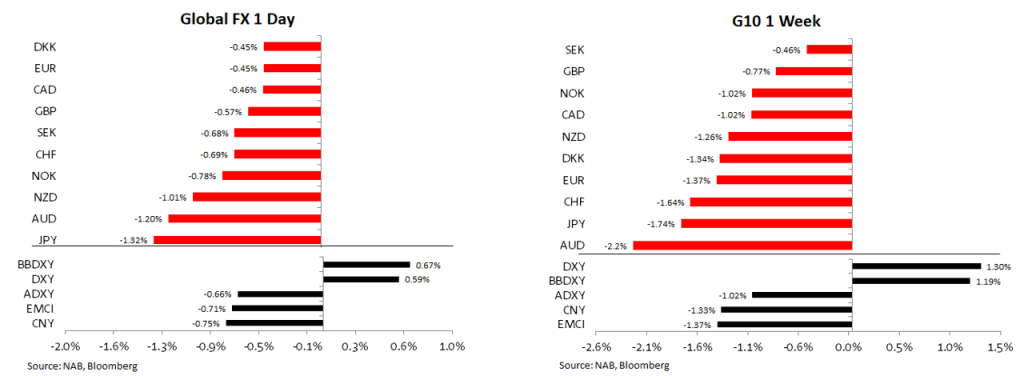

A combination of risk aversion and higher UST yields favoured the USD on Friday with the greenback stronger across the board. In index terms the USD gained around 0.6% in both DXY and BBDXY terms with the former starting the new week above 105, a level not seen since early January.

Looking at G10 pairs, EUR closed just under 1.0550, with traders eyeing support at 1.05. GBP closed just under 1.1950. The AUD was one of the big underperformers falling 1.2% on Friday and over 2.2% on the week. On Friday the AUD traded down to an overnight low of 0.6723 and now starts the new week 10bps higher. The technical picture leaves the AUD exposed to the downside with the next meaningful support area seen around 0.6660/80.

NZD was also another underperformer, down 1% on Friday. The key 0.62 support for the NZD was broken, as was the 200-day moving average of 0.6184, to close the week at 0.6165.

The higher global rates backdrop saw a weaker yen and resistance of ¥135 for USD/JPY broken, for a weekly close around ¥136.50 . My BNZ colleague, Jason Wong, notes sentiment for the yen wasn’t helped by BoJ Governor nominee Ueda’s comments as he faced questioning at Parliament. Disappointingly, he seemed to parrot the same soundbites as Governor Kuroda. Charitably, perhaps he just wanted to play a straight bat before he gets his feet under the desk. He noted that recent higher inflation was due to “cost-push” factors and not strong demand and he saw inflation falling from here, adding that current BoJ policy is appropriate. Earlier in the day, Japan CPI inflation continued to push up to fresh multi-decade highs, with the headline rate at 4.3% y/y and the core rate that excludes fresh food and energy at 3.2%.

In other economic news, German GDP for Q4 was revised two-tenths lower to minus 0.4% in Q4. Another contraction in Q1, as widely anticipated, would pass one definition of economic recession, although survey data showed improving momentum which would imply only a shallow recession

Over the weekend, media reports noted the Australian government is considering setting a maximum cap on the level of pension savings which receive concessional tax treatment, Treasurer Jim Chalmers confirmed. While Australian Prime Minister Anthony Albanese called on the country’s big banks to boost deposit rates for savers amid concerns rate hikes are only being passed on in full for borrowers.

Finally in China, the steel Hub city of Tangshan has started production restrictions to try to clear its skies ahead of some major political meetings in the country. According to Bloomberg, a so-called level-two emergency response begins Sunday, when Tangshan, 150km (93 miles) east of Beijing, expects medium or heavy air pollution, according to a statement on the local government website on Saturday.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.