Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

As we start a new week, Omicron headlines were positive on Saturday which may add to some stabilisation in risk sentiment.

https://soundcloud.com/user-291029717/too-tight-too-quickly?in=user-291029717/sets/the-morning-call

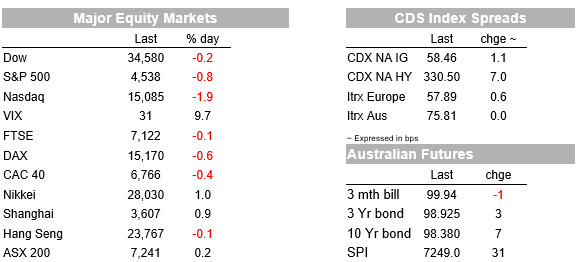

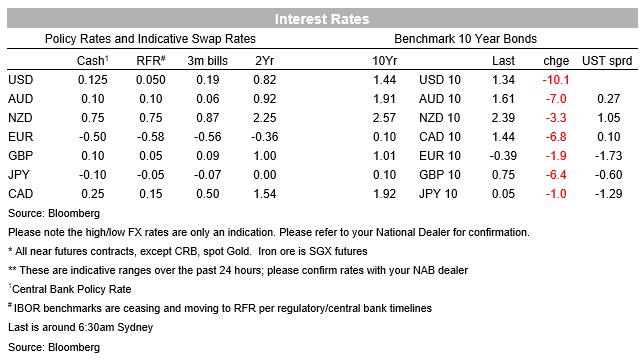

Risk assets and yields tumbled on Friday. Headline Payrolls disappointed (210k vs. 550k expected), but the four-tenth drop in the unemployment rate (5.2% vs. 5.5% expected) was seen strong enough for an accelerated taper to occur at the December meeting. There was little new news on Omicron on Friday, but it appeared markets were taking risk off the table ahead of the weekend, while equity declines (S&P500 -0.8%) were led by tech stocks (NASDAQ -1.9%) with the the hawkish tilt by the US Fed earlier in the week a factor. Yields initially rose 3-4bps in the wake of payrolls, but then fell as equities went into the red with the US 10yr yield fell -10.1bps to 1.34% to be the lowest since September 2021. The move in nominals was largely matched by TIPs with the 10yr real yield -7bps to -1.11%; the implied 10yr breakeven was -3bps to 2.44%.The 2/10s curve flattened further by -7.9bps to 75bps with 2yr yields down by just 2bps to 0.59%. Markets still price almost 3 rate hikes in 2022 with a May 2022 rate hike 89% priced.

As we start a new week it is worth highlighting that Omicron headlines were positive on Saturday, which may add to some stabilisation in risk sentiment outside of markets adjusting to a more hawkish Fed. The first study of hospital patients in South Africa was published on Saturday, pointing to the variant being ‘milder’ than prior variants and suggestive of vaccines being effective. STAT has a good summary, and the details can be found at the South African Medical Research Council: Tshwane District Omicron Variant Patient Profile – Early Features. The data shows analysis of 166 patients admitted to hospital and 42 patients on COVID ward in the Tshwane district. They conclude “that the majority of hospital admissions are for diagnoses unrelated to COVID-19. The SARS-CoV-2 positivity is an incidental finding in these patients and is largely driven by hospital policy requiring testing…” . Of the 38 adults on COVID wards, 19% did not require supplemental oxygen, most were unvaccinated or vaccination status could not be confirmed (84%).

Of course the usual caveats of these findings being too early to make a full assessment around severity or vaccine efficacy remain. We should get the first lab-based efficacy analysis by Sunday, while further data out of South Africa is expected this Tuesday. Medical experts continue to take a cautiously positive view with the US’ Fauci noting on the weekend: “though it’s too early to really make any definitive statements about it, thus far, it does not look like there’s a great degree of severity to it…Thus far, the signals are a bit encouraging. ”. For risk assets, if omicron is more mild, and vaccines still work, that could accelerate the transition to living with COVID-19. It would also put the focus back to the US Fed where the IMF on Friday played to the view of central banks needing to hike rates to ward off inflation pressures amidst the pandemic (see IMF: Addressing Inflation Pressures Amid an Enduring Pandemic).

Fears of the Fed overdoing the eventual hike cycle can be seen in Eurodollars which have a slight inversion beyond March 2024 (adjusted rate on EDH4 is at 1.57%) and on OIS FWD Swaps beyond 2Y1Y (2Y1Y is 1.34% compared to 3Y1Y at 1.26%). Fed speak seemed to confirm the markets view that the payrolls report was strong enough with the Fed’s Bullard noting: “except for the headline number, that [jobs] report seemed quite strong across the board…It certainly seems consistent….that this is a very tight labor market, ”. Bullard also sounded his usual hawkish tones, noting that “the inflation numbers are high enough that I think (ending the taper by March) would really help us to create the optionality to do more if we had to, if inflation doesn’t dissipate as expected in the next couple of month”. Bullard has pencilled in two hikes, while former Treasury Secretary Summers said the Fed should signal it could possibly raise rates four times in 2022 given inflation.

While headline payrolls did disappoint, the four-tenth drop in the unemployment rate is enough for an accelerated taper. Payrolls were +210k against 550k expected (note there were also upward revisions worth an extra 82k), disappointing for sure on the establishment survey, but the alternative household survey showed incredible strength with 1.136m jobs being added. It is unclear why the two measures are so different, though unfavourable seasonals on the establishment survey may be part of the explanation. The strong employment figures from the household survey saw the unemployment rate fall to 4.2.% against 4.5% and 4.6% previously, despite a 0.2 point rise in the participation rate. Unemployment at 4.2% places it well below the 4.8% expected by the FOMC at the September meeting for the end of 2022 and closer to their end 2022 forecast of 3.8%. Bullard noted he expected unemployment to be below 4% by Q1 2022.

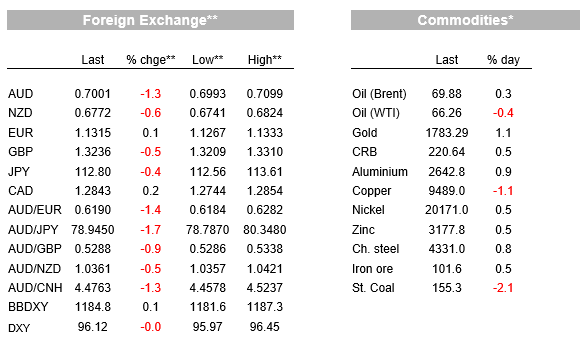

In FX, the AUD and NZD both printed fresh year-to-date lows on Friday amidst the weakness in equity markets. The AUD slumped 1.3% to 0.70 while the NZD was off 0.9% to around 0.6750, its lowest level since November last year. Safe havens outperformed, with the JPY and Swiss franc both appreciating 0.3% and the EUR gaining 0.1%. The CAD (-0.3%) fared much better than the other commodity currencies after a stellar Canadian labour market report, which showed a 153k increase in jobs and a 0.6% fall in the unemployment rate, to 6%. The market ramped up its expectations for Bank of Canada rate hikes, with a January rate hike now priced at around 66% and five hikes in total priced in for 2022. In contrast in the UK GBP closed at its lowest level in 12 months, around 1.3235 with BoE MPC member Michael Saunders hinting that the BoE might hold off raising rates this month due to the uncertainty around Omicron.

Other data out also confirmed ongoing strength in the US economy with the Services ISM printing at 69.1 against 65.0 expected. The surge in the index sends a positive signal about the economy in Q4. The not so good news remained around price pressures with supplier delivery times, prices paid, and the order backlog all hitting new highs, and plays to the view of ongoing inflationary pressure in the US. Finally, China’s Evergrande Group’s long-awaited debt restructuring may finally be at hand with Evergrande saying it could not guarantee it could meet a $260m obligation, which could likely to trigger cross default on its $19b in USD bonds. Meanwhile the Guangdong local government has sent a team to oversee risk management. Evergrande’s USD bonds are trading just over 20 cents in the dollar, so markets have effectively already priced in a restructuring/default scenario, and investors generally seem sanguine that the Chinese authorities can avoid the default turning into a systemic risk event.

It is very quiet domestically with no top-tier data of note scheduled, though in your scribe’s opinion the monthly inflation gauge from the Melbourne Institute is worth a look. Offshore there is nothing of note apart from a speech by the BOE’s Deputy Governor Broadbent. See details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.