Online retail sales growth slowed in May following a fairly strong April

Insight

The news was largely positive overnight.

https://soundcloud.com/user-291029717/topsy-turvey-response-to-a-good-news-day?in=user-291029717/sets/the-morning-call

This wheel’s on fire, Rolling down the road, Best notify my next of kin, This wheel shall explode! – Bob Dylan/The Band

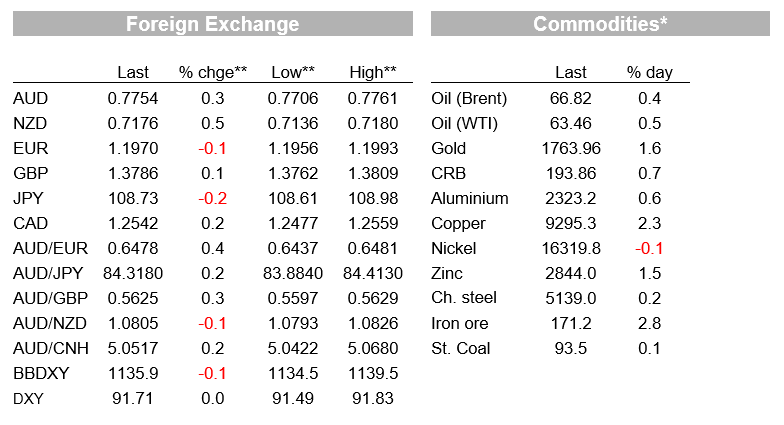

This time last week there was a bit of head scratching going on to understand why US government bond yields were softer after very strong incoming US economic data. Overnight, the tea tree oil has come out searching for nits, after 10-year Treasury yields lost some 10bps in the aftermath of some eye popping strength in Thursday’s US economic data calendar. This is turn has provided some strong support for US equities, where the main board indices have closed with gains of +/-1%, and driven a wedge between the strong data and the USD. AUD and NZD both slightly higher than where we left them yesterday evening (AUD/USD currently near 0.7750).

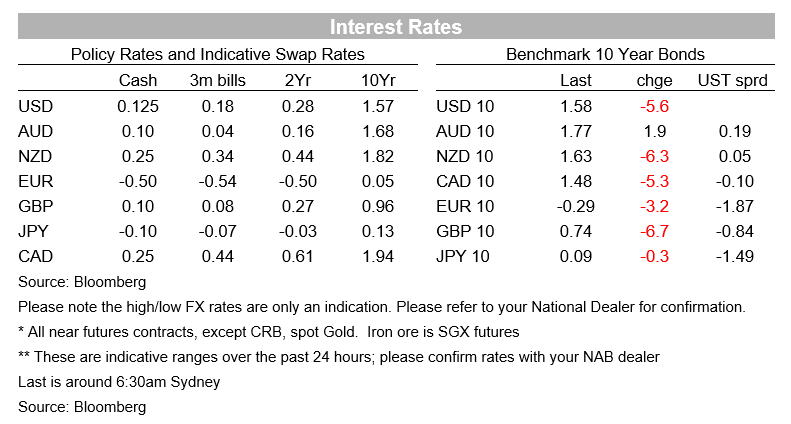

Possible explanations on offer for the sharp extension of the recent pull back in US Treasury yields – that now sees 10s down 5.6bps on the day to 1.575% after having been as low as 1.53% – are various. They include a squeeze on short positions built up in recent weeks, particularly among the Asset Management community, possible hedging activity related to an upcoming spate of bond issuance post the Q1 US earnings season (e.g. JP Morgan announced a $13bn bond sale a short while ago); and/or further evidence of consolidation after the sharp Q1 run up, something our bond strategists have been flagging for a while now, while seeing it as merely a prelude to a fresh move higher in yields later in the year.

Following on from much better than generally expected Australian labour market data yesterday (and which should ensure some substantial upward revisions to the RBA’s economic projections in next month’s Statement on Monetary Policy) almost all of the overnight US economic news punched the lights out, both in absolute terms and relative to expectations:

NZ: REINZ house sales (y/y%), Mar: 31.2 vs. 14.6 prev.

AU: Employment change (k), Mar: 70.7 vs. 35 exp.

AU: Unemployment rate (%), Mar: 5.6 vs. 5.7 exp.

US: Initial jobless claims (k), Apr 10th: 576 vs. 700 exp.

US: Retail sales (m/m%), Mar: 9.8 vs. 5.8 exp.

US: Retail sales ex auto, gas (m/m%), Mar: 8.2 vs. 6.4 exp.

US: Retail sales Control group (m/m%) 6.9% vs 7.2% exp.

US: Empire manufacturing, Apr: 26.3 vs. 20 exp.

US: Philly Fed business outlook, Apr: 50.2 vs. 40.9 exp.

US: Industrial production (m/m%) 2.7% vs. 3.7% exp.

US: NAHB housing market index, Apr: 83 vs. 83 exp.

We have to remember here that, with respect to the retail sales report in particular, many households were in receipt of $1,400 stimulus cheques in mid-March. While history suggests only about a third of the cash would be spent rather than saved or used to pay down debt, this was always going to generate a huge boost in spending – as it clearly has. Note that the so-called ‘Control Group’ which excludes items like building materials and food services (the latter jumping as restaurants and bars re-opened) was actually a bit softer than expected at 6.9% on the month versus the headline 9.8% rise. The other slight outlier, versus expectations, was industrial production coming in at 2.7% against 3.7% expected and failing to fully reverse the February weather-related hit. Here, a sharp fall in utility output as the weather dramatically warmed up, and auto production impacted by supply shortages (e.g. chips) provides adequate explanation. Regardless, analysts are busily revising upwards their estimates of Q1 GDP growth, with a stronger than previously anticipated Q2 also looking on the cards.

Since the US numbers have been published, San Francisco Fed president Mary Daly has been talking, where she notes that the Fed “hasn’t approached the time” when it would consider paring bond purchases, that “we are not there yet” on making progress on the Fed’s goals, and that were unlikely to see an “unwanted” surge in inflation.

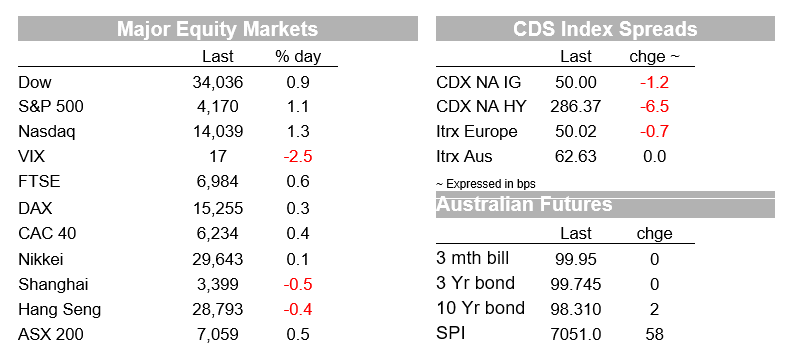

In equity markets, there was nothing not to like in the combination of super-strong data and lower bond yields, the NASDAQ just outscoring the Dow and S&P because of the latter, finishing +1.3% against +1.1% for the S&P500 and 0.9% for the DJIA. The VIX has ended the day little changed on Wednesday’s closed at 16.6. Equity gains have come despite both Citigroup and Bank of America losing a bit of ground post better than expected earnings reports, similar to JP Morgan earlier in the week and where concerns over future loan growth have somewhat overshadowed the exceptional strength noted in trading income and other investment banking revenue. Or simply another case of the market selling the fact after buying the rumour of great results.

In FX, lower US bond yields and positive risk sentiment has once again been a cocktail fuelling a softer USD, albeit not by much with the BBDXY index off just under 0.1% and the DXY virtually unchanged thanks to the EUR and CAD both failing to participate in the USD selling elsewhere. NZD and AUD top the G10 leader board with gain of 0.45% and 0.3% respectively versus Wednesday’s NY closing levels. Helpful to the cause of the AUD at least has been across-the board strength in commodity prices where all base metals are higher (led by a 2.3% rise for copper) as is oil (Brent crude +25 cents), doubtless helped at least in part by lower US bond yields and a generally softer USD.

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.