Total spending grew 0.9% in June.

Risk tone deteriorates in front of US CPI tonight, lack of positive new news on Omicron

Synonymous since the 1960s with the first day of the year that retailers supposedly start turning a profit, the original Black Friday as referenced in the Steely Dan classic was on Friday, September 24, 1869 when a bunch of wealthy investors tried to corner the gold market, buying as much as they could and driving up the price. But when the government got wind, it released $4 million worth of gold onto the market, driving down the price and clobbering the investors. This Friday brings the latest (November) US CPI print, just in front of next week’s FOMC meeting. A month ago, the October print clobbered a fair few bond market longs and US dollar bears, marking the start of the run up in 2-year Treasury yields from 40bps to 70bps and the rally in the DXY dollar index from 94 to 97. The latest (December) University of Michigan Consumer Sentiment reading will also be important, bearing in mind the November read was the weakest in over 10 years. Buckle up.

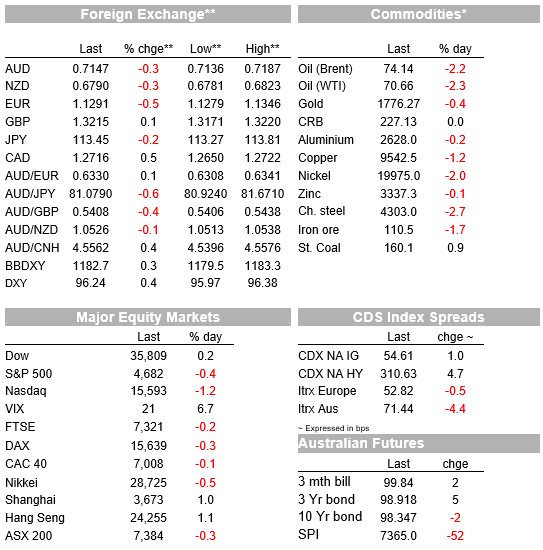

After three consecutive ‘up’ days for US equities, Thursday has seen a pull-back coming into the last hour of NYSE trade, the S&P 500 currently off a third of a percent and the NASDAQ -1.4%. Earlier European stocks finished with the Eurostoxx 50 down 0.6% and in the UK, the FTSE100 -0.2%. The initiation of Plan B in the UK, including orders for home working, restrictions on large gatherings, mask mandates, etc and whether other countries will be forced to do similar is a factor, while in Japan reports are than the Omicron Covid-19 variant is over four times more transmissible than Delta . It is also as yet unclear, according to some reports, whether existing vaccines can be easily tweaked to be as effective against Omicron (or other new variants) as prior strains.

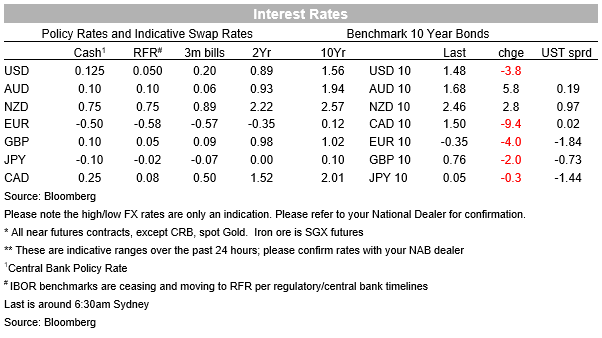

In truth the more cautious tone in risk market probably has as much or more to do with apprehension ahead of tonight’s US CPI report (see Coming Up below for expectations). In bond markets, Treasury yields are slightly lower across the board, seemingly just reflecting the poorer risk tone, with 10s -4bps to be back below 1.50% (1.48%) while 2 are little changed and the 30-year down 3bps to 1.865%, having earlier jumped from 1.85% to 1.89% in conjunction with a poor 30-year bond auction (so clearing 4-5bps above pre-auction expectations).

The US economic news overnight was in the form of a new post-1969 low for weekly initial jobless claims, down to 184k from a revised 227k last week. While the numbers suggest monthly payrolls growth should be running very much higher than November’s 210k, the main message is that firms are increasingly reluctant to let go of staff, fearful that won’t be able to find replacements when the time comes, and if so only by offering higher wages.

In Europe and ahead of the ECB meeting next week, Reuters reported that the central bank was considering boosting its existing Asset Purchase Programme (APP) when its (larger) pandemic bond buying programme rolls off in March. According to the report, options include setting a bond buying target for the APP to last until the end of 2022 or temporarily increasing the monthly APP bond buying amount from €20b, but with guidance that it will likely be tapered going forward if the economy performs as expected.

A lot going on in China in the last 24 hours, including the latest credit and money supply numbers for November. These showed New Yuan Loans up on October (Y1,270B from 826B) but largely for seasonal reasons and actually less than expected, though the broader Aggregate Financing measures that includes things like local government bond issuance, showed annual growth at 10.1% up from 10.0% in November, so signs of stabilisation here at least and for the second month running. M2 Money Supply meanwhile slowed to 8.5% from 8.7% y/y, so the pick up from 8.3% in September has not been extended.

Also of interest, yesterday the PBoC stepped in to curb ongoing CNY strengthening, which had hit a new low 3 ½ year low on Wednesday below 6.35. First the daily fixing rate was set a little higher than expected, then the PBoC lifted foreign currency reserve requirements on banks from 7% to 9%, which has the effect of taking about $20bn of FX off the banks’ hands (in essence, something that should curb their enthusiasm/raise the cost of selling FX for Yuan). In response, USD/CNY jumped by over 0.5% to 6.3776 at Thursday’s close.

In G10 FX, EUR/USD continues to labour, off another 0.5% and so largely responsible for the 0.4% rise in the DXY USD index (with bit parts played by CHF, CAD and SEK). USD strength and CNY slippage have both continued to AUD pulling back to just below 0.7150 from a high of 0.7187 around yesterday’s local close. This still leaves it more than 2% up on its early-week lows of 0.6993, and which has many of those of a technical persuasion losing conviction that AUD is about to embark on a new downtrend to well below 0.70. NOK is the weakest of the G10 pairs, with crude oil off more than 2%.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.