Coming in for landing in a heavy cross wind

Insight

Limited market reactions to ‘as expected’ US CPI – 6.8% headline highest since June 1982

To say that US CPI on Friday was largely as expected and so markets didn’t react much, does the importance of the release a disservice (and detracts from the credit due to US economists for getting a pandemic-era big number right for once!). The fact markets reacted the way they did to the highest headline CPI number since 1982, with bond yields lower across the curve led by the front end, equities up (S&P500 +1.0% to a new record closing high) and the USD slightly softer, tells us that the latest inflation horror story – and likely Fed response to be revealed this week – had been very well anticipated in the lead up to Friday’s data. Indeed, markets were evidently braced for even worse news.

So headline US CPI rose to 6.8% from 6.2% (0.7% m/m) the highest headline read since 1982 (versus since 1990 for the October reading) with core (ex-food and energy) up to 4.9% from 4.6% last time, both bang in line with consensus. While use car prices (up 2.5%), lodging away from home (2.9%) and airline fares (4.7%) drove the headline increase, the most disconcerting element of the release was that shelter , comprising both rents and owner-equivalent rents (the latter largely a function of (rising) house prices) which together comprise 32.8% of core CPI – rose by 0.4%. This is the third straight increase above 0.4% and so running at a 5% annual rate. Clothing, new car prices and tobacco also contributed positively to the overall 0.5% monthly rise in core CPI.

The bottom line in that core CPI has not yet peaked, almost guaranteed to rise above 6% – and possibly as high as 7% come Q1 2021 according to our friends at Pantheon Economics.

Also of note on the US economic data front and linked to high and rising inflation, the University of Michigan’s preliminary December consumer sentiment index rose to 70.4 from 67.4, above the consensus, 68.0 but which is still the second weakest reading of the last ten years. The rise was led by a 4.3-point increase in the expectations component, while current conditions rose a meagre 1.0 point, with competing influences from falling covid case numbers, the emergence of Omicron and high gasoline prices. Inflation expectations at both the 1-year (4.9%) and 5-10-year (3.0%) levels, were unchanged on November.

The test for markets this week, alongside the various central banks meetings (see Coming Up below) is whether latest Omicron developments can derail risk sentiment alongside the strong gains witnessed for some commodities last week, the latter led by oil (+8%). South African has just reported 37,875 daily cases, surpassing the peaks of its prior wave, while in the UK news on Friday from the Health department is that Astra-Zeneca provides virtually no protection against Omicron for those who received their second jab several months ago and have not yet received a booster. The good news is that booster shots are seen restoring vaccine efficacy against Omicron to 70-75%. The Australian government’s response so far has been to bring forward the interval between second doses and booster jabs to five months from six. The glass half full interpretation of latest developments is that deaths from the Omicron variant are so far, mercifully, non-existent in most countries (e.g. none in Europe) and that health systems at least in developed countries do not so far appear to be overloaded.

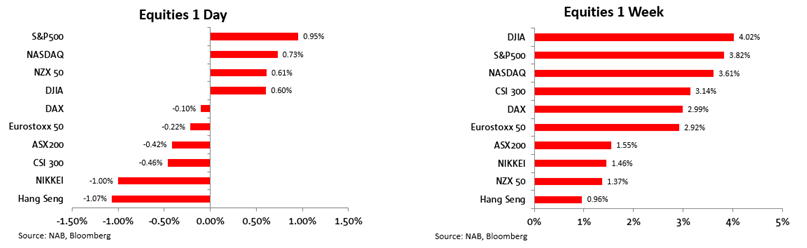

Risk asset market took Friday’s CPI report in their stride , the S&P500 ending the New York day up 1% to a new record closing high to be up 3.8% on the week, with the NASDAQ not far behind, up 0.7% on the day and 3.6% on the week. The US market was again out in front globally, with Europe and Asia stocks all down Friday, though all major indices closed the week higher (Hang Seng the underperformer, up a little under 1%).

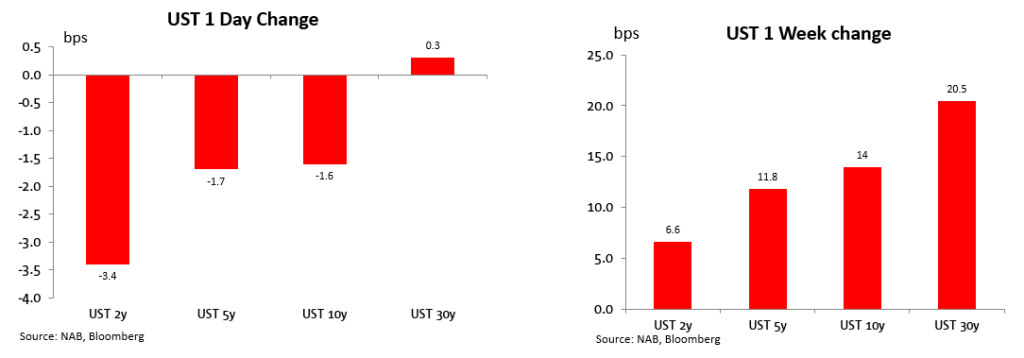

US bond market reaction was to see bullish steepening of the US yield curve, against consistent with a ‘sell the rumour, buy the fact’ mentality vis-à-vis CPI. 2-year Notes finished Friday 3.4bps lower and 10s -1.6bps, while the 30-year was virtually unchanged. The front end of the US curve nonetheless still has the best part of three quarter-point Fed rate rises priced in for 2022, the first no later than June. On the week, the US curve bear steepened, with 2s up 6.5bps and the long bond up 20bps. 10-year Aussie bond futures were 4bps lower in yield terms Friday but 2.5bps up on the week versus -1.6bps for US 10s.

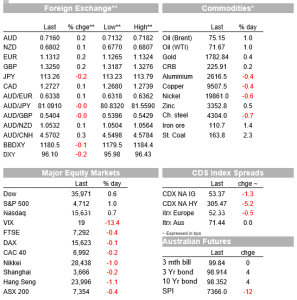

It turned out to be a pretty interesting week in the world of currencies , no more so than in the AUD which spent time – albeit very briefly – sub-0.70 either side of the previous weekend. So a Monday low of 0.6995 gave way to a high of 0.7187 last Thursday, not far from where it ended the week (0.7172, for a weekly gain of 2.4%). These gains came without – somewhat unusually – any assistance from Emerging Markets, Asia especially, where the ADXY was little changed on the week and Asia stocks clear underperformers, even though most indices eked out at least some strength on the week.

Developed Market risk sentiment and some heady gains for commodity prices (including iron ore) and, judging from latest IMM data, a very short speculative market at the start of the week, do a decent job of explaining last week’s AUD recovery, where the role of oil (WTI +8% on the week) shows up in the NOK just pipping AUD to top slot on the G10 scoreboard. The big dollar, as represented by the DXY, was marginally lower Friday, post CPI and ended the week virtually unchanged, so still about one percent off its late November high just shy of 97.0.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.