Total spending grew 0.9% in June.

As widely expected, the BoE lifted the cash rate by 50bps and retained the option to act forcefully in the future, the Bank now officially sees a recession in the horizon.

https://soundcloud.com/user-291029717/uncertainty-reigns-except-in-britain-its-just-grim-there?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

GE: Factory orders (m/m%), Jun: -0.4 vs. -0.9 exp.

UK: Bank of England base rate (%), Aug: 1.75 vs. 1.75 exp.

US: Trade balance ($b), Jun: -79.6 vs. -80 exp.

US: Initial jobless claims (k), 30-Jul: 260 vs. 260 exp.

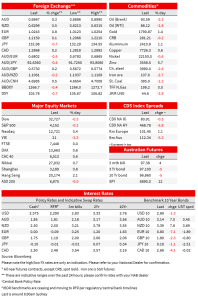

Ahead of US payroll tonight US and EU equity markets have traded in and out of positive territory, ending the day with modest gains/losses. There is a sense of daze and confusion with investors struggling for direction with geopolitics adding another layer of uncertainty. News that China may have fired missiles over Taiwan has not helped sentiment, but it hasn’t rattle markets either. As widely expected, the BoE lifted the cash rate by 50bps and retained the option to act forcefully in the future, the Bank now officially sees a recession in the horizon. Core yields have drifted lower with the belly leading the yield decline in the UST curve. The USD is broadly weaker with the euro back above 1.02, USD/JPY below ¥133, AUD a tad higher at 0.6975.

The S&P 500 has ended the day down by 0.08% while the NASDAQ is up by 0.41%. Investors are treading water ahead of non-farm payrolls tonight with mixed earnings reports contributing to the lack of direction. Amazon.com and Advanced Micro Devices reported better than expected numbers but Fortinet Eli Lilly disappointed, weighed on the S&P 500 Index. After a solid rebound in July, the index has been consolidating in the early part of August showing resilience against a backdrop of mixed economic data releases, heightened geopolitical tensions and expectations the Fed won’t hike as much as previously feared.

A similar theme is evident in Europe with the Euro Stoxx 600 ending the day marginally in the green (+0.18%), after posting its biggest monthly gain since November 2020 in July. The economic outlook remains a big uncertainty with the Bank of England lifting the cash rate by 50bps while at the same time it becomes the first DM Central Bank to forecast a recession for its economy. A reminder that Central Banks with price stability objectives are currently solely focus on bringing inflation down and as we have been saying in FX strategy weaker growth along with softer labour markets are not the problem – they are part of the solution.

So as expected by a decent majority (70% of economists, ~76% priced by markets), the Bank of England lifted its cash rate by 50bps to 1.75%, its biggest interest-rate hike since 1995.The decision was supported by eight of the of the bank’s nine policy makers with Silvana Tenreyro voting for a 25 bps increase. The Bank retained complete flexibility in terms of options for its next meeting in September, but also noted that the Committee will be particularly alert to indications of more persistent inflationary pressures, and will if necessary, act forcefully in response.

The Bank’s new forecast make it clear that the primary objective is to bring inflation down with headline inflation now projected to a peak of 13.3%yoy in Oct and quarterly peak of 13.1% in Q4 . In its central forecast, GDP is expected to fall from a Q3 2022 peak for 4 quarters before staging a very slow recovery over the subsequent 2 years, such that the level of real GDP in Q3 2025 is projected to be about 1% below its Q3 2022 peak. The projected downturn it’s the cost of bring inflation back under control. The BOE also laid out its plans for reducing the Gilt holdings it bought during the crisis; they’re likely to start after a confirmatory vote in September and it will be in the region of around £10b a quarter. My BNZ colleague, Nick Smyth notes that the BoE and the RBNZ are the only two central banks that are taking the step of selling their bonds, to reduce their holdings faster than simply waiting for the bonds to mature.

Moving onto the US economic data releases, jobless claims have continued the slow grind higher, printing 260k in the latest week (4wk ma up to 254k) . The rise was in line with expectations and suggests there are some early signs of a softening US labour market. These are early days, but the data is fuelling an emerging debate between some Fed officials and prominent economists. Can we have a decline in inflation with an ease in labour demand without a material rise in the unemployment? Some argue that in the current environment many companies are counting lower hiring plans as job cuts, so if you believe there is a significant number of companies doing this, then the answer is yes. A pullback in hiring plans has certainly been an evolving theme in the current earnings reporting season.

Oil prices have continued to fall, with WTI futures falling below $90/barrel for the first time since February, around 2.5% lower on the day. The recent fall in oil prices, which are now trading below the levels immediately before Russia’s invasion of Ukraine, has contributed to the market’s perception that inflation is likely to peak soon, taking pressure off the Fed to raise rates as aggressively. And while we are talking about commodities, iron ore has extended its decline overnight falling almost 3% to $107 and down 10.94% in the past five days . After initial hopes China will step in to support its property sector, the lack of details is now raising concern over the demand for steel amid the prospect of a more subdued economic recovery which also remains clouded Beijing zero-covid policy.

Core global yields have drifted lower overnight with UK Gilts little changed after the BoE, yield on the two-year note closed around 1bps higher at 1.85%; the 10-year closed 2bps lower at 1.89%. 10y Bunds were more lively, declining -7bps to 0.80% while in the US the belly of the curve led the decline in yields, down 6bps to 2.769% while the 10y Note decline 3.7 bps to 2.688%.

The market continues to price almost two rate cuts from the Fed next year despite continued hawkish rhetoric from officials . Overnight, Cleveland Fed President Mester said it was “not unreasonable” to raise the cash rate to “a little above 4” while suggesting she could favour a more frontloaded profile for hikes than what was set out in the Fed’s June projections.

Meanwhile, media reports have suggested China fired missiles over Taiwan during military drills on Thursday. Japan’s Ministry of Defense estimated that five ballistic missiles landed in Japan’s exclusive economic zone, and four of those probably flew over Taiwan. Officials in Taiwan and the US have not commented, but if confirmed this would be a sign of major escalation as it would be the first time China has flown missiles over Taiwan itself. The news of course are a concern and clearly has not helped sentiment, but it hasn’t rattle markets either.

The USD is broadly weaker with the DXY index down 0.76% to 105.76 while BBDXY is -0.45%. The euro is a notable out performer, up 0.8% to 1.0248, GBP in contrast was little changed at 1.216 showing little lasting effect from the BoE decision (up on the rate hike news, down on the recession news). The AUD has edged up a little over the past 24 hours, now trading at 0.6971 (+0.4%), of note yesterday Australia’s today’s Jun trade surplus hit another record high, $17.67bn up from a downwardly revised $15bn in May, well outpacing forecasts for a fall to $14bn but in line with our $18bn forecast. NZD has broken back above the 0.63 mark, 0.6% higher than this time yesterday.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.