NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

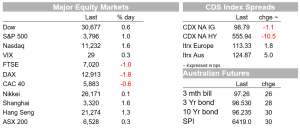

Despite softer PMIs and still-hawkish messaging from the Fed, US equities managed to turn around intraday.

https://soundcloud.com/user-291029717/unconditional-commitment-come-what-may?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Another day and another opportunity to weigh recession risk. This time against the backdrop of hawkish noises from the Fed’s Powell and Bowman and June flash PMI’s which, for the euro area at least, were decidedly soft. ECB speakers for their part continued to emphasise the need to normalise policy amid elevated inflation and risks of expectations de-anchoring. Government bonds rallied, led by Europe.

Despite softer PMIs and still-hawkish messaging from the Fed, US equities managed to turn around intraday, the S&P500 up 1.0% on the day and 1.4% off its earlier lows. Outcomes were mixed across industries, with gains in utilities, healthcare and real estate offsetting falls in energy. The Dow was up 0.6%, while the Nasdaq posted a 1.6% gain. Earlier, European bourses had fared less well, the EuroStoxx 50 down 0.8%.

Powell in his second day of congressional testimony, this time in front of the House financial services committee largely reiterated familiar lines. “We can’t fail on this. We really have to get inflation down.” Pressed on how the Fed would weigh its competing priorities in a situation where the labour market and growth were flashing clear signs of slowdown ahead of compelling evidence of cooling inflation, Powell’s instinct was that “In that hypothetical situation, that would be a setting in which inflation could be expected to come down ” but quickly reiterated the inflation focus, adding that “we’re gonna want to see evidence of it really coming down before we declare any victory, so I think we’d be reluctant to cut.” Elsewhere though, he called the commitment to curbing inflation ‘unconditional’ and summarised that “We have a labor market that is sort of unsustainably hot and we’re very far from our inflation target.” Separately Fed Governor Michelle Bowman said she backed raising rates by 75bp next month, followed by more hikes of at least 50bp until price pressures cooled.

S&P Global flash PMIs were the key data overnight. All in all they were doing nothing to assuage fears of a slowdown. Of most note was numbers out of the euro area. The Eurozone composite measure fell to 51.9 from 54.8, sharply softer than the 54.0 expected, with S&P summarising the detail “Eurozone growth slows sharply to 16-month low in June as demand stalls and price surge continues.” The US read was also on the soft side of expectations , the composite measure at 51.2 from 53.6 and 53.0 expected. The detail reveals the first contraction in new orders since July 2020 and new export orders contracting at the steepest pace since June 2020, and while input cost pressures remain, the pace of input cost inflation slowed to its lowest in 5 months. US jobless claims for the week ending 18 June came in at 229K after 231K. Still above recent lows, but not signalling a material slowing in the labour market at these levels.

ECB speakers for their part continued to underscore the need to normalise interest rates. Governing Council member Nagel said “Central banks must not respond with too little, too late. ” He added that what the ECB is doing is not dependent on the actions of other central banks and pointed to the ‘worrying’ development that German household and firm’s inflation expectations were “somewhat less anchored than, say, a year ago.” Villeroy at the same event also noted the need to push ahead with normalisation. “Our action will be orderly. We sometimes use the word gradual, which doesn’t mean slow.”

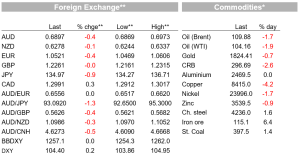

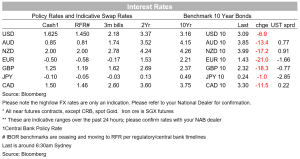

Yields were lower. The US 10yr yield was down 7bp to 3.09% while the 2yr was 5bp lower. The softening outlook in Europe helped German 10yr rates 21bp lower to 1.43% and the German 2yr yield a sharp 25bp lower to 0.80% in its biggest drop since March 17, 2008, the day after JPMorgan Chase & Co. announced it would buy Bear Stearns. ECB hiking expectations were pared, markets discounting the effective rate will end 2022 at 0.98%, compared to 1.15% a day earlier.

In currency markets, the US dollar was a little higher on the DXY, managing a 0.2% gain. The yen strengthened, with the US dollar down 0.9% against the currency, back to 134.97. Indicative of the risk-off tone, the Swiss franc was the only other G10 currency to manage a gain against the dollar. The AUD was 0.4% lower at 0.6897, paring losses from an intraday low of 0.6875 alongside a recovery in US equities.

In other news, Germany triggered its second highest ‘alarm’ stage gas emergency level. Economy Minister Robert Habeck warned of potential contagion if losses piled up from suppliers being forced to cover volumes at high prices, citing the potential for “a Lehman effect in the energy system. ” There has been a reduction in flows from Russia since June 14 and the gas crisis is expected to impact industrial production and become “huge burden” for many consumers. Meanwhile, the EU agreed to grant Ukraine and Moldova candidate status for EU membership. Candidate status is just one step in a potentially decades long process. Kyiv warned there must be “no illusions” about joining the EU anytime soon.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.