Total spending grew 0.9% in June.

Core global yields have been the big market movers overnight with European bonds leading the decline in yields.

https://soundcloud.com/user-291029717/understanding-how-little-we-understand?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Core global yields have been the big market movers overnight with European bonds leading the decline in yields. Speaking in Portugal, Fed Chair Powell reiterated commitment to raising rates “expeditiously” while also acknowledging path to achieving a soft landing is getting narrower. Equities struggle for direction, ending the day lower. The USD is stronger across the board with the euro leading declines amid mixed inflationary signals.

The ECB Sintra forum has been a focal point for markets overnight with a lot of heavy hitters expressing their views. Reiterating recent comments, Fed Chair Powell said he was more worried about inflation shifting into a higher regime than the possibility of raising interest rates too high and pushing the economy into a recession. Powell then expressed confidence the US economy can withstand a higher tighter monetary policy, retelling the Fed’s commitment to raising rates “expeditiously” and move “into restrictive territory fairly quickly,”. The Fed Chair effectively endorsed current market pricing signalling another 75bps hike will be on the table for discussion when FOMC meets again in late July.

In a similar line of thinking, BoE Governor Baily said the Bank will act more forcefully if inflation proves persistent, but like Powell he did not explicitly say what the Bank will do over coming meetings. Lagarde reiterated the ECB will consider the anti-fragmentation tool at its next meeting in July while the pace of tightening is data dependent. Singing from the same song book as Powell, Lagarde noted sadi “I don’t think we are going to go back to that environment of low inflation . . . there are forces that have been unleashed . . . that we’re facing now that are going to change the picture and the landscape within which we operate.”

European bonds led a decline in global yields with the tough talking from Central Bank heads playing into concerns over a policy induced global growth slowdown. For Europe, however, mixed signals coming from Spain and German inflation readings added another layer of uncertainty. Higher food and energy costs drove Spanish inflation to 10% last month while German inflation fell to 8.2%yoy against expectations for a 8.8% outcome. Cuts in fuel duty and discounted public-transport tickets helped slow the surge in German prices, but is worth noting these measures are only temporary, starting this month and running through July and August.

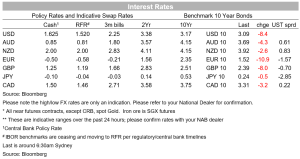

German Bund yields ended the day down between 10-13bps across the curve, while peripheral spreads narrowed with the likes of Greek 10-year yields falling 21bps while 10y Italian BTPS fell 16bps. The decline in UST yields was also in a parallel fashion, down between 6 and 8bps across the curve. 10y UST yields now trade at 3.0873% with breakevens again leading the decline, down around 15bps over the past two days and now trading at 2.39%, close to the lows printed back in January.

Earlier in the session, the Fed’s Mester noted that the Fed is ‘just at the beginning’ of raising interest rates and that ‘there are risks of recession’. She wants to see the Fed Funds rate reach 3% to 3.5% this year and ‘a little bit above 4% next year’.

Equities have struggled for direction amid the tough talking from central bank heads. European equities fell for the first day in four days with sentiment also hurt by China reaffirming its commitment to its Covid Zero policy. Late in our session yesterday, President Xi Jinping declared Covid Zero the most “economic and effective” policy for China adding that China would rather endure some temporary impact on economic development than let the virus hurt people’s safety and health. The CSI 300 ended the day down 1.5%, breaking a recent run higher. The Stoxx Europe 600 Index fell by 0.7% after posting its strongest three-day rally in six weeks. Meanwhile in the US, both the S&P 500 and NASDAQ traded in narrow ranges ending the day with modest decline, -0.7% and -0.3% respectively.

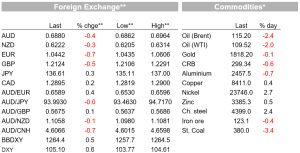

Moving onto FX, the USD has benefited from the uncertainty in the air with the euro leading the decline with G10 pairs, down 0,74% to 1.0442. The larger yield declines in European bonds overnight, not helping the union’s currency. In contrast, the decline in yields didn’t help the yen, with USD/JPY almost touching ¥137, before easing back to ¥136.56 where it currently trades.

Commodity currencies have also struggled against the USD with the AUD trading down to an overnight low of 0.6868, starting the new day 10 pips higher. NZD is a touch lower than this time yesterday, hovering above the 0.62 mark and eyeing month and year-to-date lows just under that figure. Month/Quarter end is a consideration today with large declines in equity markets over the past three months suggesting some large rebalancing/hedging flows could be in the offing.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.