Online retail sales growth slowed in May following a fairly strong April

Insight

Fallout from UK mini-budget continues.

The UK and the reaction to the new government’s Growth Plan once again dominated attention to start the new week. The pound touched a record low of 1.035, only managing to regain some ground on a renewed surge in gilt yields and BoE hike expectations. Yields globally have also pushed higher and the dollar is up at least half a per cent against each G10 currency and 0.7% higher on the DXY. US equities are lower, with the S&P500 losing 1.0% to its lowest close since December 2020.

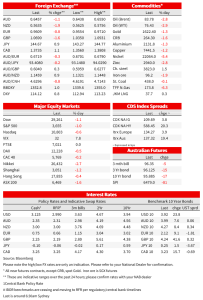

First to the UK, where after taking the weekend to digest the implications of the UK government’s tax-cuts-from-borrowing growth plan, markets remain unimpressed. The pound dropped to an all time low of 1.035 early in Asia. That ground back over the next several hours as rising gilt yields and expectations of BoE action supported the pound, the currency making it back a little above Friday’s close to at one point touch 1.093. A BoE statement poured cold water on the idea of an emergency hike saw the pound fall anew as near-term rates pricing was pared. The pound is currently around 1.069, 1.6% below Friday and 5.3% below where it was before the growth plan.

Helping to explain the volatility is just how cloudy the outlook is . With the questions of longer-term sustainability dependent on whether supply side reforms and tax cuts designed to stimulate growth are effective, the lack of detail is complicating what would already be a difficult assessment. We now have some more clarity on the timeline form here. Chancellor Kwarteng brought forward a plans for a medium-term fiscal strategy to November 23 and promised to bring down debt as a share of GDP. That update will be alongside a forecast from the independent Office for Budget Responsibility. The Bank of England statement followed soon after the Chancellor’s and welcomed the Treasury’s commitment “the role of the Office for Budget Responsibility.”

The BoE’s statement was brief and said that the MPC “will make a full assessment at its next scheduled meeting…and act accordingly.” “The MPC will not hesitate to change interest rates by as much as needed to return inflation to the 2% target sustainably in the medium term.” The statement dampened expectations for an emergency hike. As much as 80bp of rate rises had been discounted this week, but that fell back to 10bp following the statement and the pound weakened. Pricing for the BoE had pushed to 200bp of tightening up to and including the November meeting at one point, but now sits at around 150bp for November and a peak in Bank Rate of 6% by May next year. UK 2yr gilt yields were up another 56bp to 4.49%, a full ppt above Thursday’s level. The 10yr was 42bp higher to 4.24%. It was 3.49% on Thursday.

Yields globally were also higher. US yields continued their push higher, the 10yr up nearly 22bp to 3.9%, outpacing the selloff at the 2yr, where yields were 14bp higher to 4.34%. German 10yr bund yields rose 9bp to 2.12%. The Italian 10yr yield rose 22bp to 4.55%, with the spread to bunds its widest since May 2020 as counting confirming that the Meloni-led coalition won about 44 per cent of the vote in Italian elections, enough to give it a comfortable parliamentary majority.

The surge in US yields added support, if more were needed, to the dollar. The DXY was 0.8% higher at 114.09, with Bloomberg noting that the Fed’s trade-weighted US dollar index hit a record high. The Kiwi was again an underperformer, down 1.9% against the dollar to 0.5635. The AUD fell 1.1% to be below 65c for the first time since the initial COVID shock in 2020, and before that since March 2009. The euro was 0.8% lower against the dollar.

Equity markets struggled . APAC bourses were generally lower, the Nikkei losing 2.7% and the ASX 200 1.6% lower. European share were generally softer with the Euro Stoxx 50 losing 0.2%. US shares were also down. The S&P500 dropped 1% to a new 2022 low, while the Nasdaq was 0.6% lower. The Dow’s fifth daily decline in a row took the index it into bear market territory for the first time since early in the pandemic. Italy’s FTSE MIB was an outlier, rising 0.7% as investors so far don’t judge a large risk of policy clash with the European Union.

In economic news, the OECD’s interim forecast update showed sharply downgraded global growth, led by a b ig hit to the European outlook, The OECD warned of difficult winter and costs from the war in Ukraine, while also noting that inflation had broadened and there was a need for higher interest raises in most major economies. Global growth was downgraded to just 2.2% over 2023 from 2.8% at the June update. There was a stark 2.4ppt downgrade for Germany, now seen -0.7% over 2023, while the Euro area as a whole down 1.3pp to 0.3. Australia was not immune to deteriorating global outlook but fairs relatively well, the OECD seeing growth of 2.0% over 2023. In the data flow overnight, there was no disagreement from the German Ifo survey, which showed confidence dropped from 88.6 to 84.3 vs expectations for 87.0. The decline was led by a 5.3 point plunge in the expectations component and was seen across sectors.

Also of some note were comments from Lagarde at regular testimony to European Parliament. Lagarde played down the chances of quantitative tightening in the near term and emphasised policy rates are the preferred tool for now. “When we have completed our monetary policy normalization, using the most appropriate, efficient and effective tool, that are the interest rates, then we will ask ourselves: how, when, at which rhythm, at which pace, we use the other monetary tools that we have available, including quantitative tightening.” The comments are in some contrast to recent comments from the Bundesbank’s Nagel who is “clearly for a reduction of our balance sheet.” It’s worth remembering, though, that on current market pricing the ECB could be at neutral, Lagarde’s threshold for thinking about QT, this year. Some ECB estimates of neutral for sit around 2%, a level the ECB would reach in December if it matched current pricing.

Meanwhile in China the PBoC signalled more discomfort with yuan depreciation as the CNY got within 1% of a 14-year low against the dollar. On Monday, the PBoC imposed a risk reserve requirement of 20% on banks’ foreign-exchange forward sales to clients, making it more expensive to bet against the yuan with derivatives.

NAB Markets Research Disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.